Running a business involves making various types of payments throughout the tax year. While you might have extensive experience in paying and reporting non-employee compensation to independent contractors on Form 1099, there are many other payment types that can become more intricate.

One such complex payment type is attorney fees. Navigating the reporting process for payments made to an attorney throughout the year can be challenging and may vary depending on specific scenarios.

Here is an overview of the essential information needed to maintain accurate records for your business and report this information to the IRS successfully at the end of the year. It is also important to note that it is best practice to contact a tax preparer or CPA with specific questions pertaining to your business.

In this article, we cover the following topics:

- Understanding Attorney Fees

- IRS Guidelines for Reporting 1099 for Legal Fees & Settlements

- Navigating 1099-MISC vs. 1099-NEC for Attorney payments

- 1099 for attorney fees paid by credit card

- When to Issue 1099s for Attorney Fees?

- Report Attorney Fees on the Appropriate 1099 Forms

- Common Mistakes to Avoid

1. Understanding Attorney Fees

There are different types of payments that are made to an attorney. When you hire a lawyer, they will request payment or fees for their services. For example, if you open a business and hire a lawyer to assist you in drawing up documents and incorporating, they will charge legal fees for their service.

There are also some circumstances where you may pay someone else’s lawyer, this is likely in the case of a settlement. The Legal Information Institute defines a settlement as an agreement between two parties that ends a dispute and results in the voluntary dismissal of any related litigation.

2. IRS Guidelines for Reporting 1099 for Legal Fees & Settlements

The IRS requires different reporting procedures for when you are reporting legal fees vs. when you are making a settlement payment to someone else’s lawyer. The IRS requires that you report payments to your attorney for legal fees on Form 1099-NEC if the payment(s) total $600 or more.

When you pay someone else’s lawyer in regard to a settlement, this payment should be reported on 1099-MISC if it totals $600 or more. When it comes to hiring an attorney for personal matters, this is not typically reported on 1099, as it happens apart from the business operations.

3. Navigating 1099-MISC vs. 1099-NEC for Attorney payments

With that said, it is not always that cut and dried. See the table below for some examples of when you should choose

Form 1099-NEC vs. 1099-MISC for attorney payments.

| Scenario | Who should file? (Payer) | Who is the recipient? (Payee) | Which 1099 is used? (NEC or MISC) | What is the deadline? |

|---|---|---|---|---|

| A business hires an attorney or law firm and pays them $600+ in legal fees. | The business should file to report the payments. | The attorney is the recipient and should receive a copy. | Form 1099-NEC for non-employee compensation should be filed. E-File Now | The deadline to file and furnish copies of 1099-NEC is January 31st. |

| A law firm pays another attorney a fee for co-counseling a case. | The law firm should file to report the payments. | The attorney who is the co-council should receive a copy. | Form 1099-NEC for non-employee compensation should be filed. E-File Now | The deadline to file and furnish copies of 1099-NEC is January 31st. |

| A law firm receives settlement proceeds on behalf of a client. | The taxpayer who is making the payment to the law firm’s client should file. | The law firm should receive a copy. | Form 1099-MISC for miscellaneous payments should be filed. E-File Now | The deadline to furnish a copy of Form 1099-MISC is January 31st. The deadline to e-file is March 31st. |

| A business hires a law firm to represent them in a legal dispute. The lawyers of both parties come to a settlement. The business is in turn required to pay the other parties’ legal fees in addition to their own. | The business should file a 1099-NEC to report the payments made to their attorney. They should file a 1099-MISC to report payments made to the opposing counsel for their client’s legal fees. | The business’s attorney should receive a copy and the opposing counsel (law firm or attorney) should receive a copy. | Form 1099-NEC for non-employee compensation should be filed. Form 1099-MISC for miscellaneous payments should be filed. E-File Now | The deadline to file and furnish copies of 1099-NEC is January 31st. The deadline to furnish a copy of Form 1099-MISC is January 31st. The deadline to e-file is March 31st. |

Do You Want to File 1099 Forms?

Get Started Today with TaxBandits and File Form 1099 in 3 simple steps. Deliver Recipient Copies via Postal mail or Secure Online Portal at the Lowest Price in the Industry. E-file Now

4. 1099 for attorney fees paid by credit card

Businesses should report direct payments made to attorneys by using Form 1099-NEC or Form 1099-MISC if the payment was made by check or cash. However, if the attorney fees were paid via credit card, rest assured, the payment settlement entity (PSE) is the one responsible for reporting these transactions to the IRS using Form 1099-K. Form 1099-K is used to report payments processed through payment cards (e.g., credit and debit cards) and third-party network transactions (e.g., PayPal) to the IRS.

5. When to Issue 1099s for Attorney Fees?

The amount of the payment made to the attorney will indicate whether or not a 1099 should be issued. Issuing a 1099 for attorney payments is only required if the business paid a lawyer $600 or more. Again, if the attorney was hired for personal matters and the legal fees paid were in regard to personal matters such as divorce proceedings and personal estate dealings fall under non-taxable income, they do not need to be reported to the IRS.

When the attorney payment is directly related to your business, you will likely File 1099-NEC. While payments made to corporations do not typically require a 1099, attorney payments are unique. Any payment of $600 or more made to a single attorney or law firm is required, whether they are classified as a sole proprietorship, partnership, LLC, or corporation.

If you've paid $600 or more legal fees to an attorney who is not directly serving your business, you should likely use Form 1099-MISC instead. For example, settlement payments made to an opposing party’s attorney or law firm.

6. Report Attorney Fees on the Appropriate 1099 Forms

The first step to preparing accurate 1099s for attorney payments is to properly document them. Throughout the course of the year, all payments made to an attorney or law firm whether they were directly or indirectly your business’s law firm or attorney should be recorded. This way, at the end of the year you will be able to clearly see the total amount of the payment(s) and the purpose behind them. This will help you to know whether a 1099 needs to be issued, and which 1099 form to use.

-

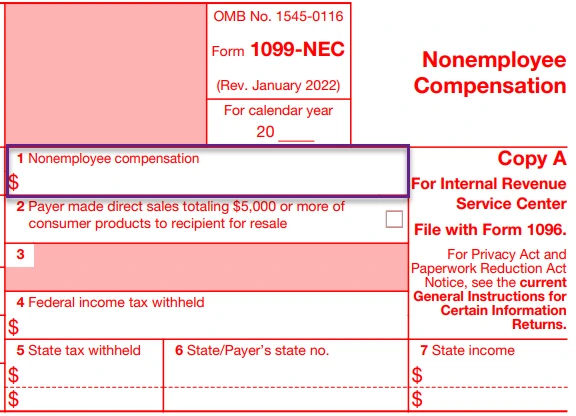

When preparing Form 1099-NEC to report a payment to your attorney, you can enter this amount in Box 1: Nonemployee compensation.

-

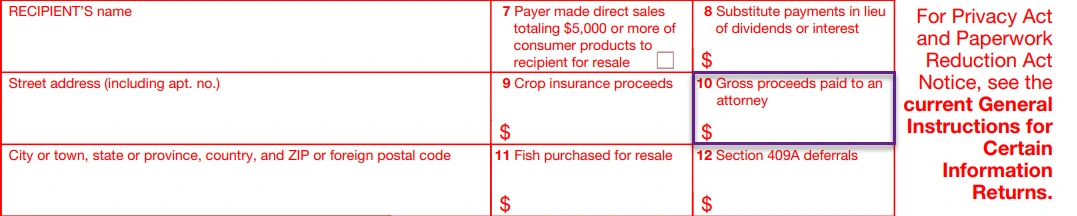

When preparing Form 1099-MISC to report a payment to an attorney that you are not directly a client of, this should most likely be reported in Box 10: Gross proceeds paid to an attorney.

-

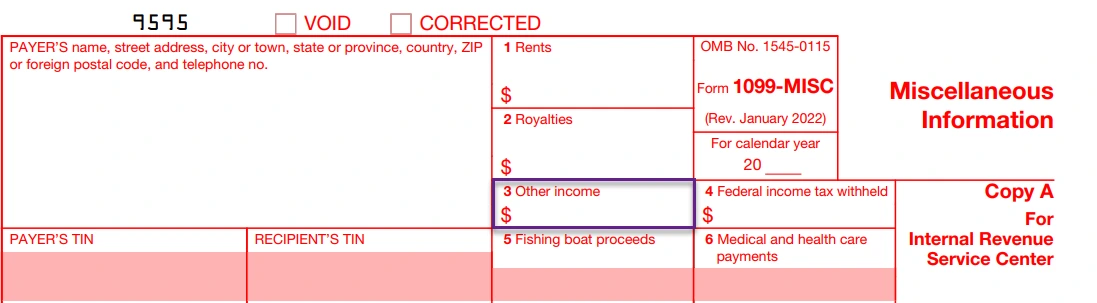

When paying legal damages to a claimant (not their attorney), this is generally reported in Box 3: Other Income.

7. Common Mistakes to Avoid

When filing 1099 forms for attorneys, making mistakes can easily lead to penalties or delays. To help ensure smooth filing, here are some common errors to avoid.

- Not having correct TIN Information: You must have the correct taxpayer identification number associated with the attorney or law firm you’ve paid for. If your business doesn’t have this information available when filing, it is impossible to file an accurate 1099 Form. The solution for this is to request a Form W-9 from all contractors, vendors, and attorneys that you do business with well before the year-end filing deadlines. TaxBandits offers both a complete W-9 Manager and a fillable W-9 option to help payers and their payees avoid this complication.

- Filing the Wrong 1099 Form: Remember, as a general rule, if a payment of $600 or more is made to your attorney, Form 1099-NEC is likely the required form. On the other hand, when you're making payments for damages from a settlement or compensating a lawyer representing the opposing party in a legal proceeding, you typically need to file 1099-MISC online.

- Missing the 1099 Filing Deadline: It's important to note that although both 1099-NEC and 1099-MISC are part of the same IRS series of forms, they have different deadlines. The 1099-NEC due is earlier, on January 31st, allowing taxpayers ample time to receive their copy and accurately report the nonemployee compensation they received on their personal income tax returns. It is also important to complete and distribute 1099-MISC and 1099-NEC in time for the recipient copy deadline on January 31st, regardless of the filing deadlines. Not filing within the required deadline will result in potential penalties. To learn more about the 1099 penalties, click here.

Securely E-file Form 1099 with TaxBandits in Minutes!

E-filing Form 1099 is seamless with TaxBandits, an IRS-authorized e-file provider designed to streamline the filing process while ensuring accuracy and efficiency. Here's how TaxBandits makes filing easier:

- TaxBandits take care of both federal and state filings in one place.

- We print and mail recipient copies, ensuring your recipients receive their forms on time.

- TaxBandits supports distributing recipient copies through online access.

- With standard CSV templates, importing your data makes it easy to file multiple forms.

- Ensure accurate filing with internal audit checks and TIN matching.

- Get instant support via phone, e-mail, or live chat.

Share this article

Related Topics

Related Topics

IRS Form 941

- Form 941

- Form 941 Instructions

- Form 941 Due Dates

- Form 941 Mailing Address

- Form 941 Schedule B

- Form 941 Penalty

- Form 941 ERC

- Form 940 vs 941

- Form 941 vs 944

Revised Form 941 for 2023

Form 941 Worksheets

- Form 941 Worksheet 4 for Q3 & Q4 2021

- Form 941 Worksheet 2 for Q2 2021

- Form 941 Worksheet 1

- Form 941 Worksheets

IRS Form 941-X

Revised Form 941 for 2022

Revised Form 941 for 2021

- IRS Form 941 for Q4 2021

- Revised Form 941 for 2nd Quarter, 2021

- Form 941 Quarter 2 vs Quarter 1, 2021

- Revised Form 941 Schedule R for Q2 2021

- Revised Form 941 for 1st Quarter, 2021