Reliable 1042 filing solution, built for everyone

Whether you file a handful of forms or manage high-volume 1042 submissions, our software scales with your reporting needs.

Simplified Form 1042 Filing for Businesses of All Sizes

Stay compliant with annual withholding tax reporting requirements without increasing administrative complexity.

Fast Preparation & IRS E-Filing

Prepare and transmit Form 1042 quickly using reconciled totals from your withholding payments and related 1042-S data, supported by structured workflows and bulk upload options.

Guided Signing & Submission

Complete electronic authorization using Form 8453-WH or Form 8879-WH and e-file directly with the IRS through an

authorized platform.

Built-In IRS Validations

Automatically identify missing fields, inconsistent totals, and reporting errors before transmitting your Form 1042 to reduce the risk of rejection.

Expert Guidance at Every Step

Access AI-powered assistance and live support to confidently navigate complex withholding calculations and

reporting requirements.

Multi-Client Form 1042 Filing, Structured for Tax Firms

Manage annual withholding tax return filings across multiple clients with complete visibility, delegation control, and secure collaboration.

Bulk Filing

Upload multiple Form 1042 filings using your existing CSV file or our standard template. Prepare and validate returns efficiently before IRS transmission.

Centralized Dashboard

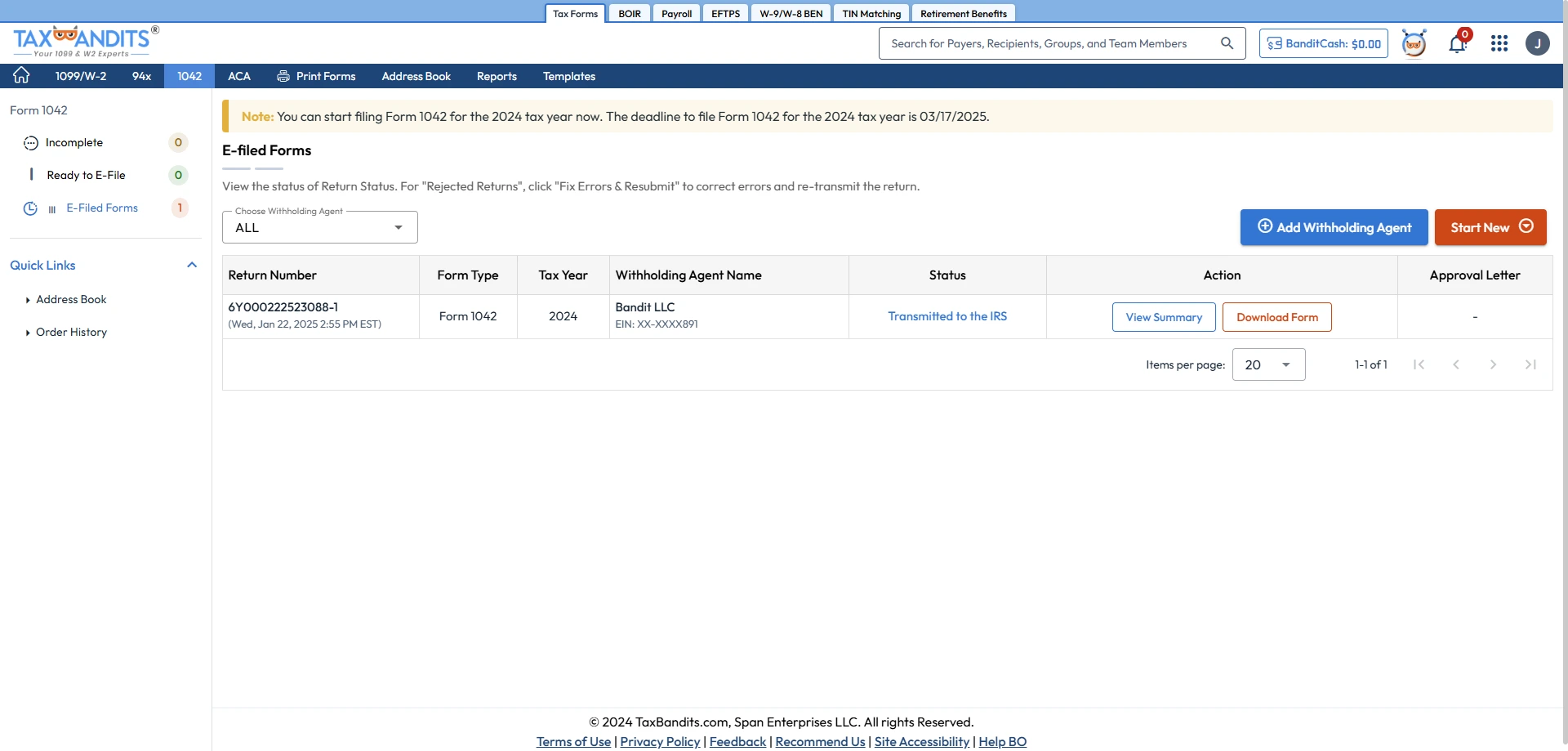

Track filing status, IRS acknowledgments, corrections, and upcoming deadlines for all clients in one consolidated view.

Branded Client Portal

Provide clients with secure access to review returns, exchange documents, and collaborate through your firm-branded portal.

Role-Based Team Access

Assign preparer, reviewer, and transmitter roles to staff members with controlled permissions while maintaining firm-wide oversight and compliance control.

Enterprise-Scale Form 1042 Reporting Infrastructure

Standardize annual withholding tax compliance across departments, entities, and high-volume filing operations.

High-Volume Processing at Scale

Manage large volumes of Form 1042 filings using structured data imports, API integrations, and optimized enterprise-grade workflows.

Seamless Data Ingestion

Import withholding and payment data through bulk uploads, custom templates, ERP integrations, or direct API connectivity to align with existing systems.

Personalized Branding

Customize internal portals and email communications to align with corporate branding and stakeholder expectations.

Streamlined Workflow

Invite teams, assign precise roles, and delegate filings with clear ownership and approval workflows.

The Bandit Commitment

Ensuring the right outcome for

every 1042 you file.

With TaxBandits, 1042 filing goes beyond just submission. Our focus is accuracy, acceptance, and accountability, from data ingestion through IRS acceptance and beyond.

The Bandit Commitment defines how we approach compliance: prevent errors before filing, guide you during filing, support corrections when required, and stand behind every transmission.

Getting the Right Data in

Compliance begins with clean, validated withholding data, aligned with your Form 1042-S filings—well before transmission.

Guided, end-to-end compliance

End-to-end guidance for accurate filing. Federal submission, and ongoing compliance—all handled together.

No Cost Corrections & Retransmissions

Corrections and retransmissions for your 1042 are included with your filing fee.

Money-Back Guarantee

If a 1042 is not accepted or is identified as a duplicate, the filing fee may be refunded.

How to file 1042 online with TaxBandits

It’s simple. TaxBandits provides a structured workflow to prepare, reconcile, and file your annual withholding tax return accurately and on time.

Prepare and reconcile Form 1042

TaxBandits gives you the tools to accurately prepare Form 1042 based on your annual withholding activity.

-

Withholding Reconciliation

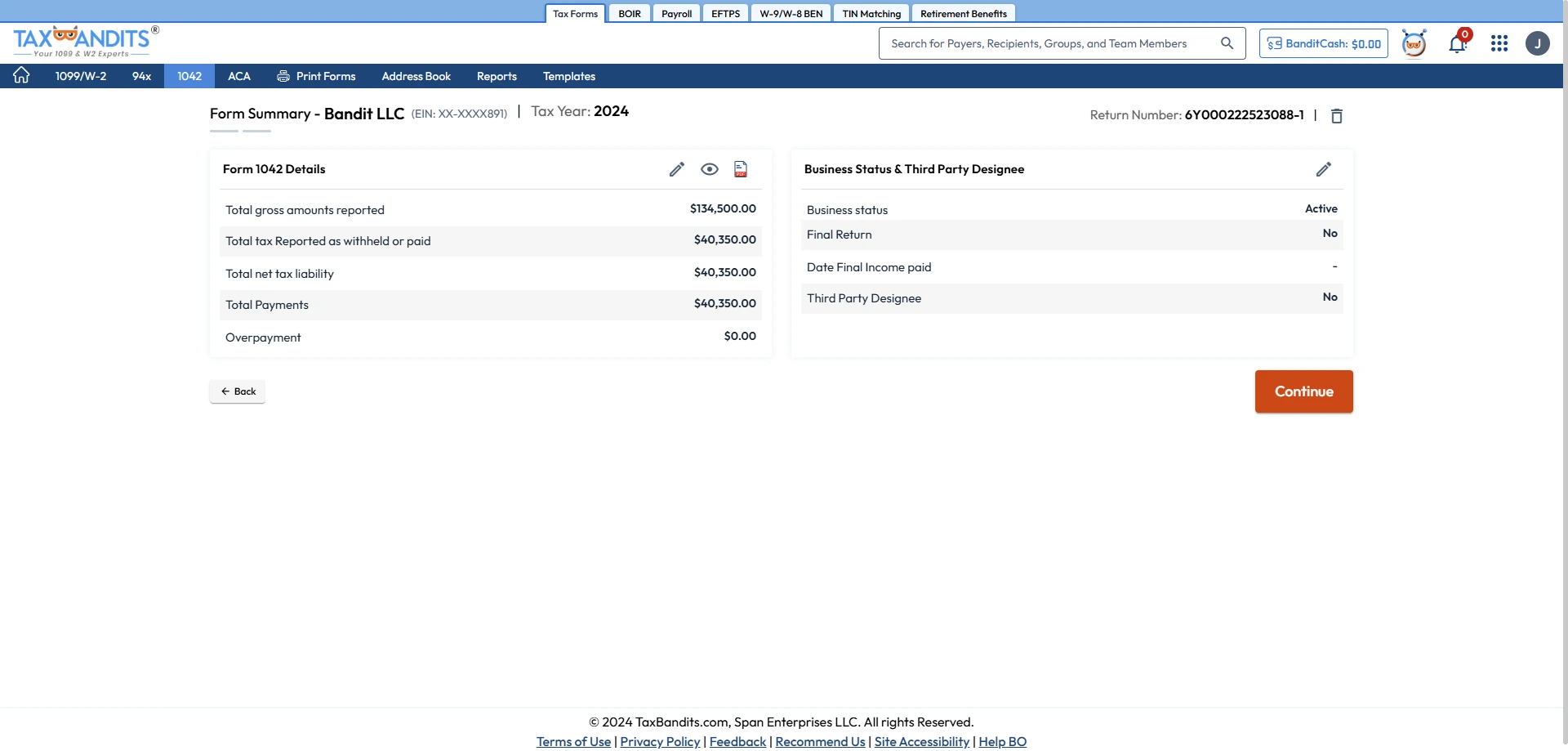

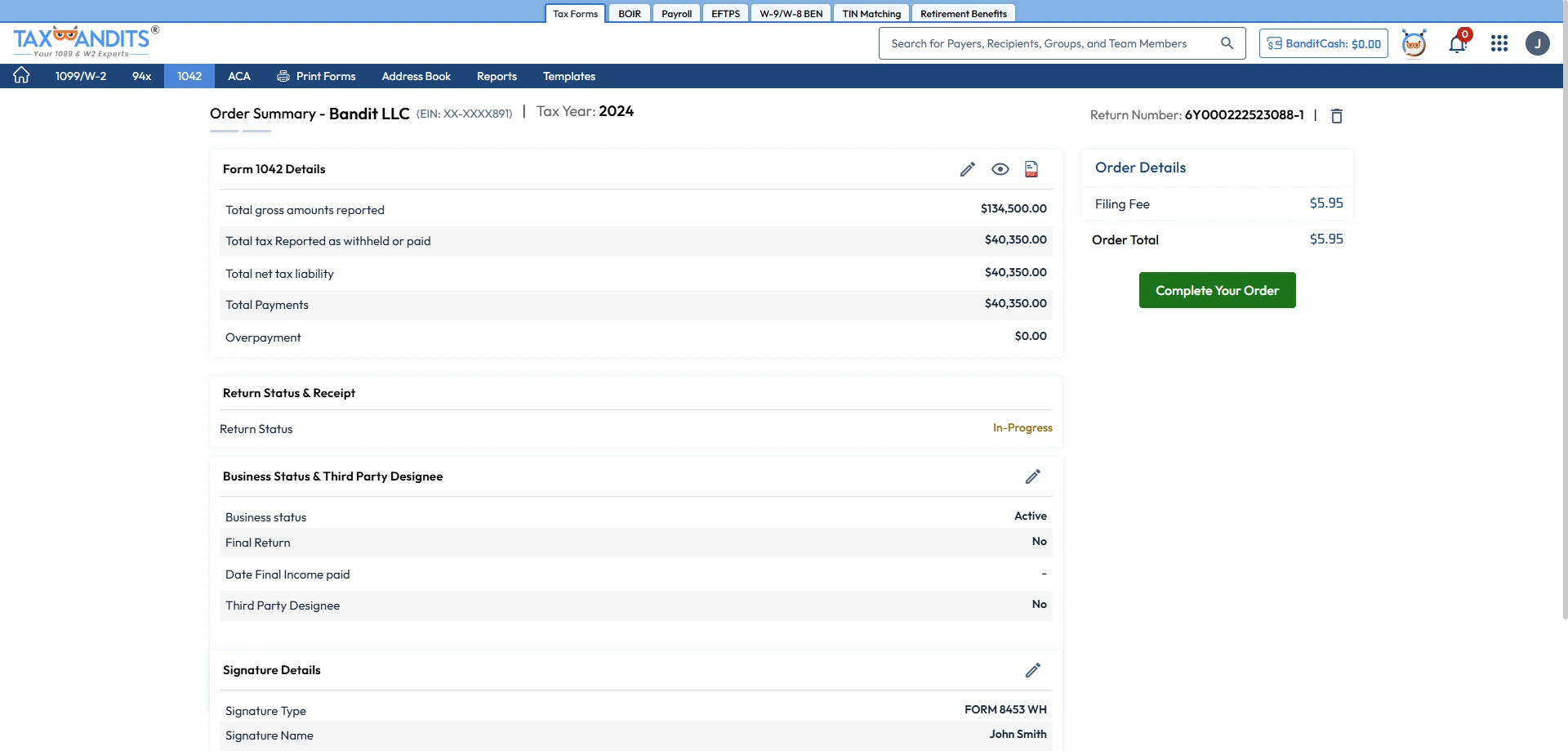

Prepare Form 1042 using reconciled totals from your payments and corresponding 1042-S data to ensure Chapter 3 and Chapter 4 reporting accuracy.

-

Support for Supporting Schedules

Include Schedule Q if you are a Qualified Derivatives Dealer (QDD) at no additional cost, ensuring full compliance with reporting requirements.

-

Attach 1042-S with 1042 (Line 67)

Easily attach your Form 1042-S records to Line 67 on Form 1042 and let the system reconcile your claimed withholding credits.

Ensure accuracy with validations

Our system performs validations throughout the preparation process to help minimize IRS rejections.

-

Form-Level Validations

Detect missing fields, incomplete totals, and inconsistencies in reported withholding amounts before submission.

-

Withholding & Tax Liability Checks

Confirm tax liability amounts align with your total payments and reconcile properly with associated 1042-S filings.

-

Pre-Submission Smart Review

Review flagged issues and error alerts before IRS transmission to improve acceptance rates and filing confidence.

E-sign and E-file with confidence

Complete your filing securely and stay informed throughout the process.

-

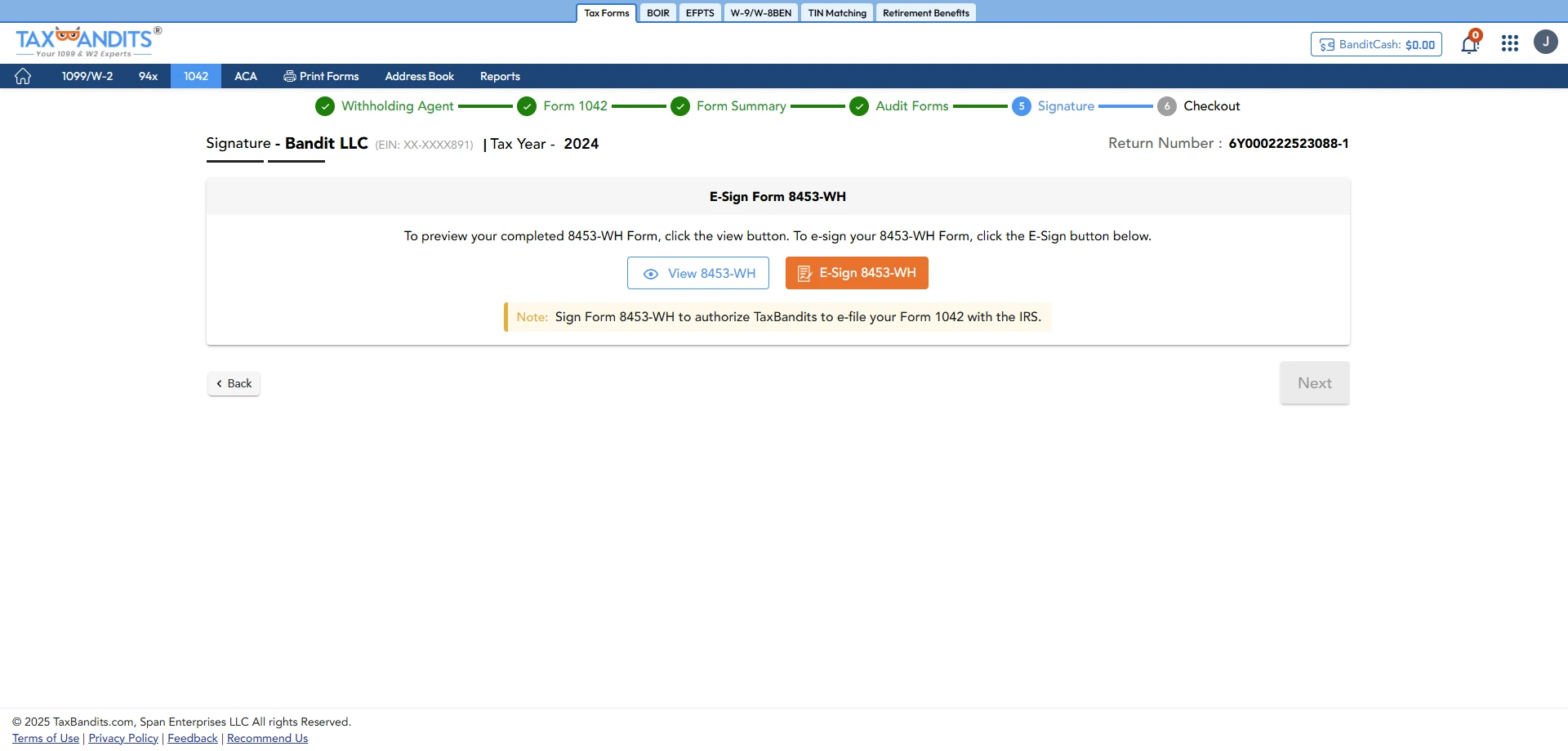

Simple Electronic Signing

Sign Form 1042 electronically using Form 8453-WH or Form 8879-WH for a smooth and secure authorization process.

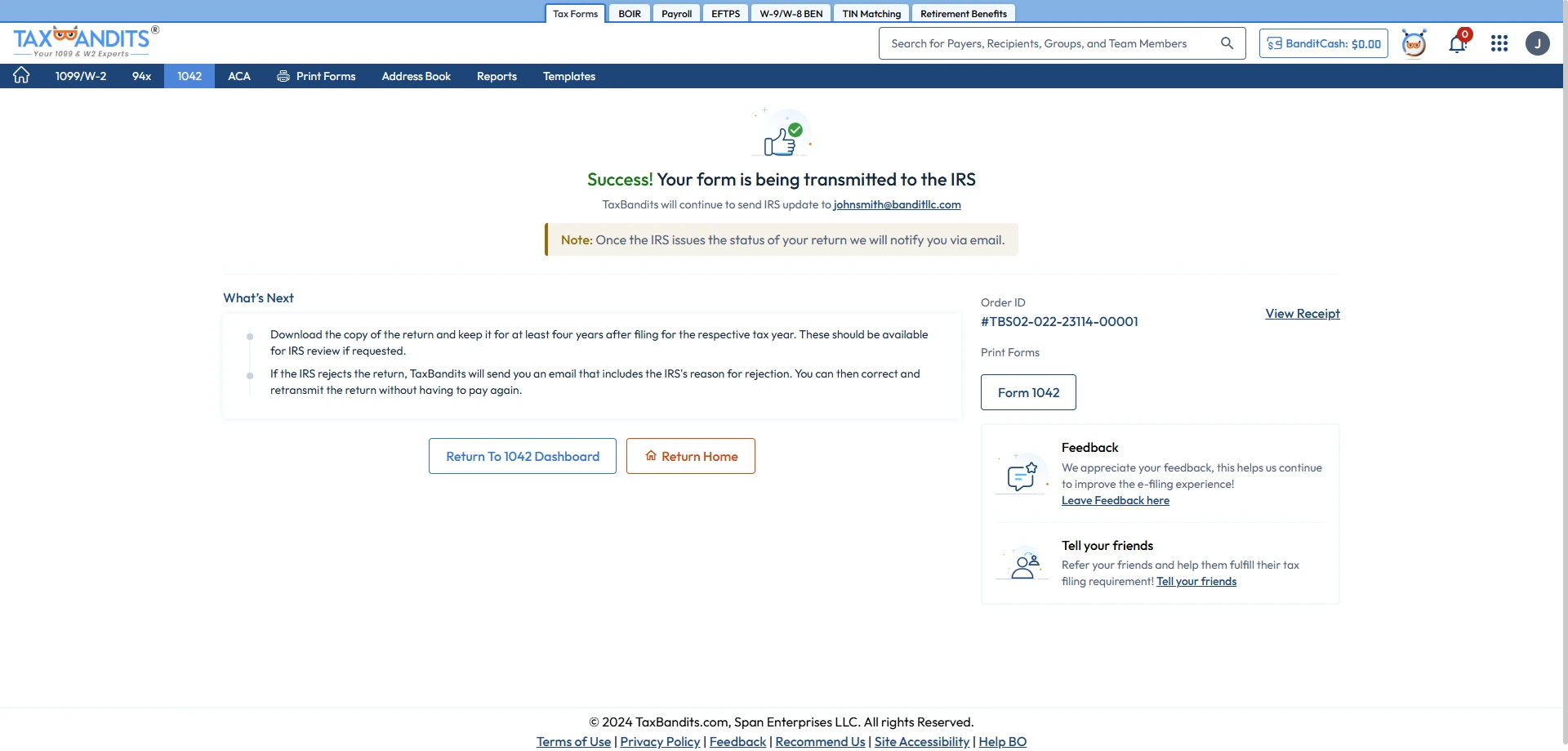

Get real-time status updates via email or text notifications once the IRS processes your Form 1042.

-

Direct IRS E-Filing

Transmit Form 1042 electronically through our IRS-authorized software for timely and compliant annual filing.

-

File an Extension When Needed

Need more time? File Form 7004 in just a few clicks to receive an automatic 6-month extension to submit your Form 1042.

Supporting diverse 1042 reporting needs across industries

From education to finance, organizations across industries rely on TaxBandits for structured, compliant 1042 filing.

Universities & Educational Institutions

Report payments to foreign students, scholars, and researchers with accurate withholding classification.

Financial Institutions & Investment Firms

Manage substitute dividends, interest income, and other foreign payments with structured validation and scalable filing workflows.

Gig Platforms

Report payments to international freelancers and contractors with proper withholding treatment and bulk filing capability.

Trading and Investment Companies

Comply with withholding and reporting requirements for foreign investors across diverse income types.

Gaming and Casinos

Accurately report winnings paid to foreign individuals with validated income classification and secure distribution.

Payment Platforms

Process and report cross-border payments for clients with structured data import and high-volume filing support.

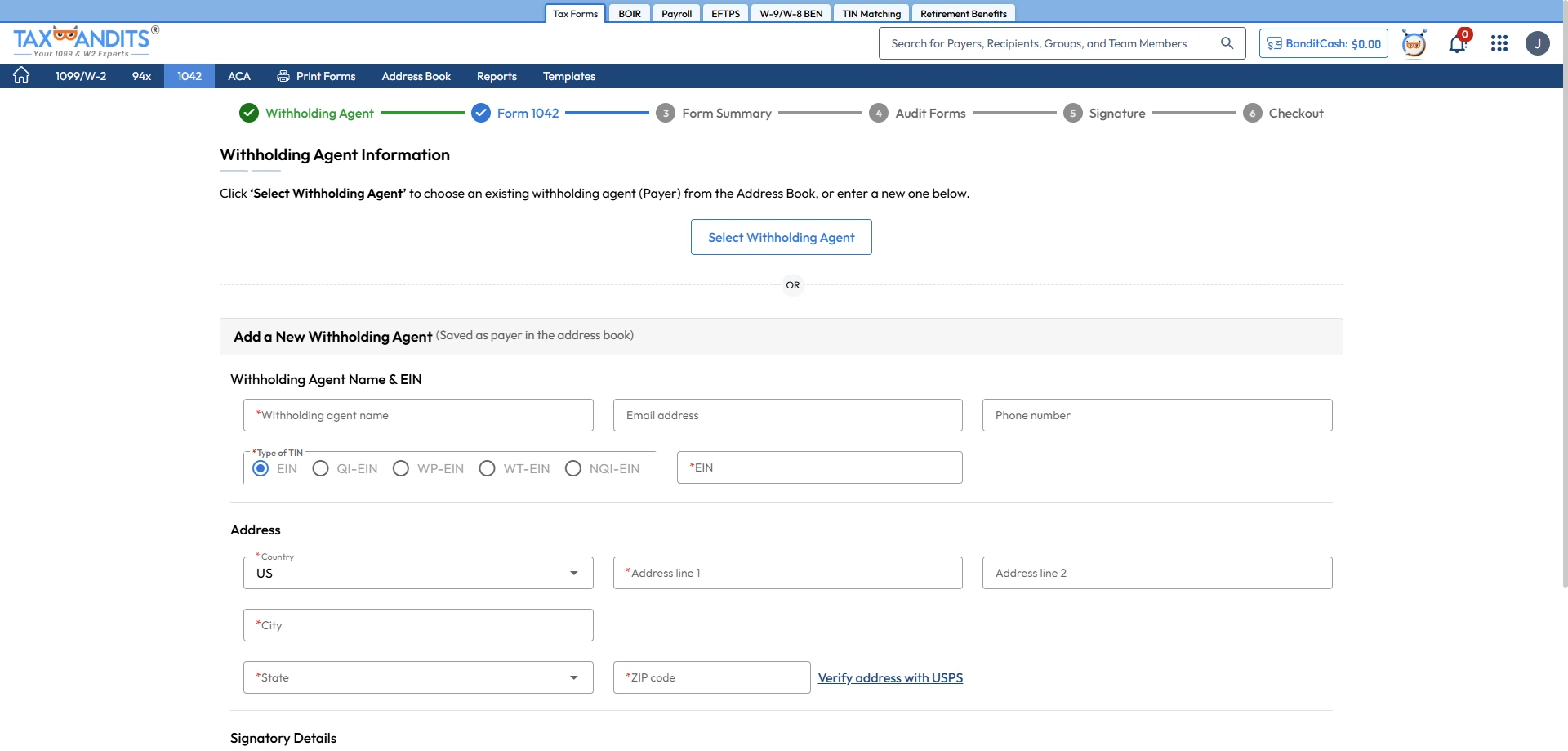

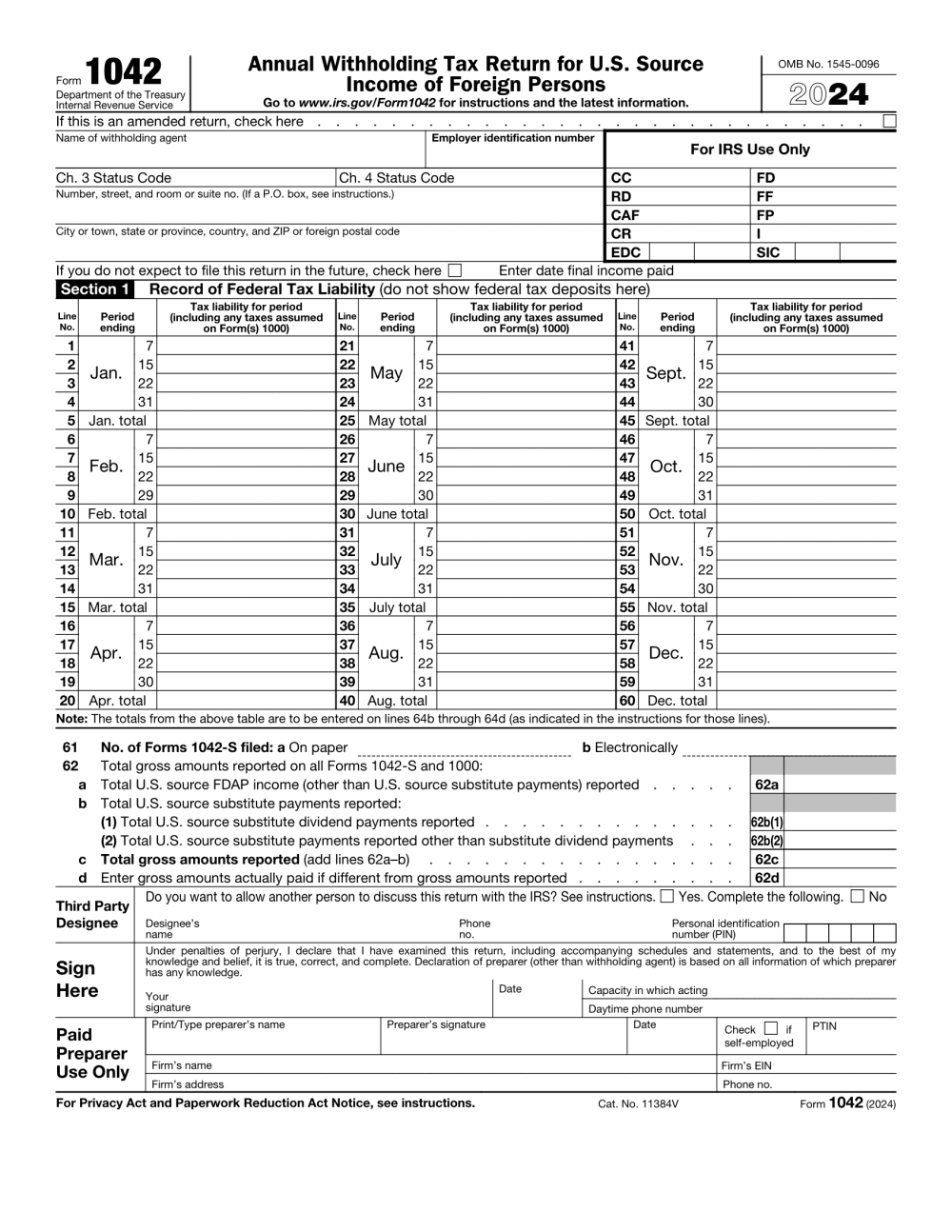

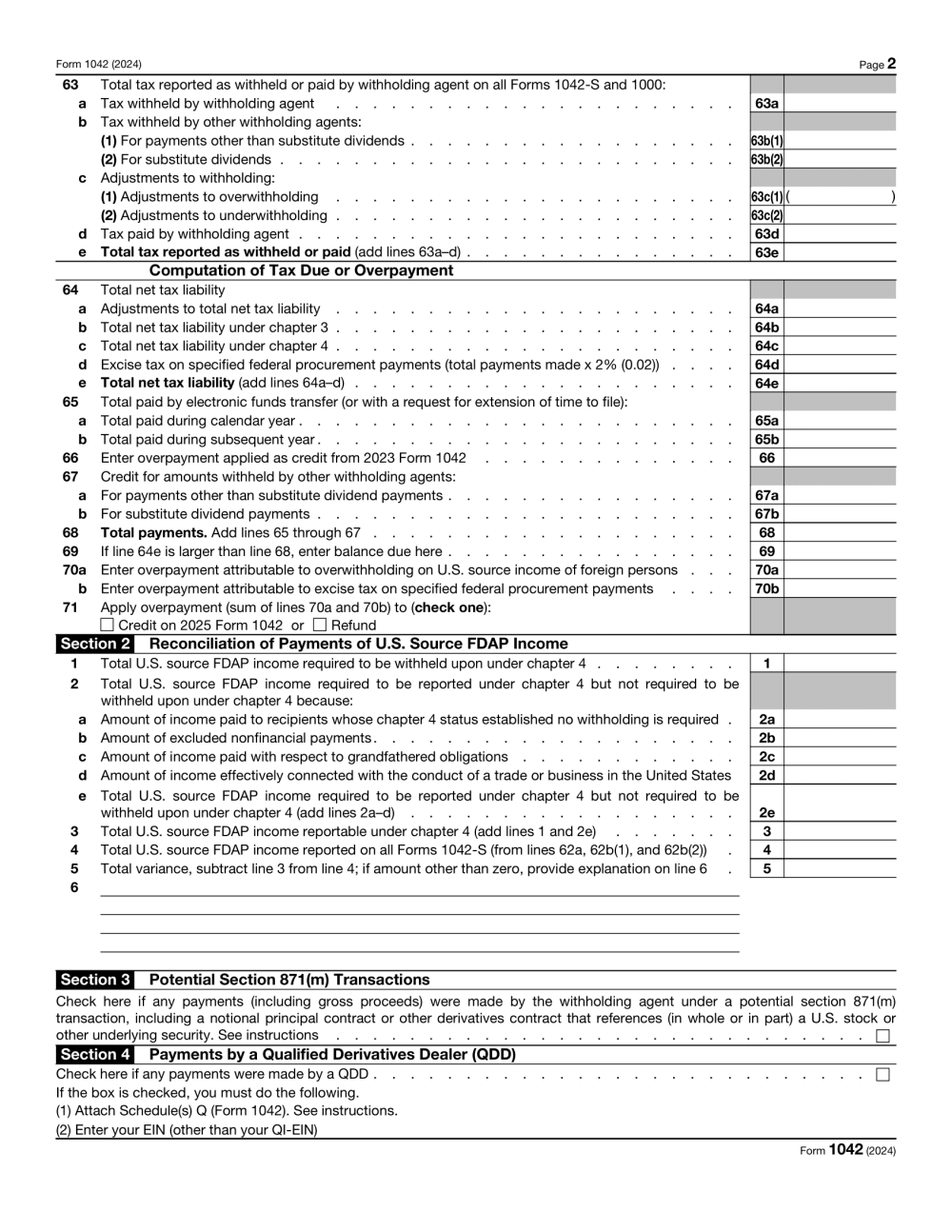

Information Required to E-File Form 1042 Online

-

1. Withholding Agent Information

- Name, EIN, Address, Chapter 3 & Chapter 4 Status Codes

-

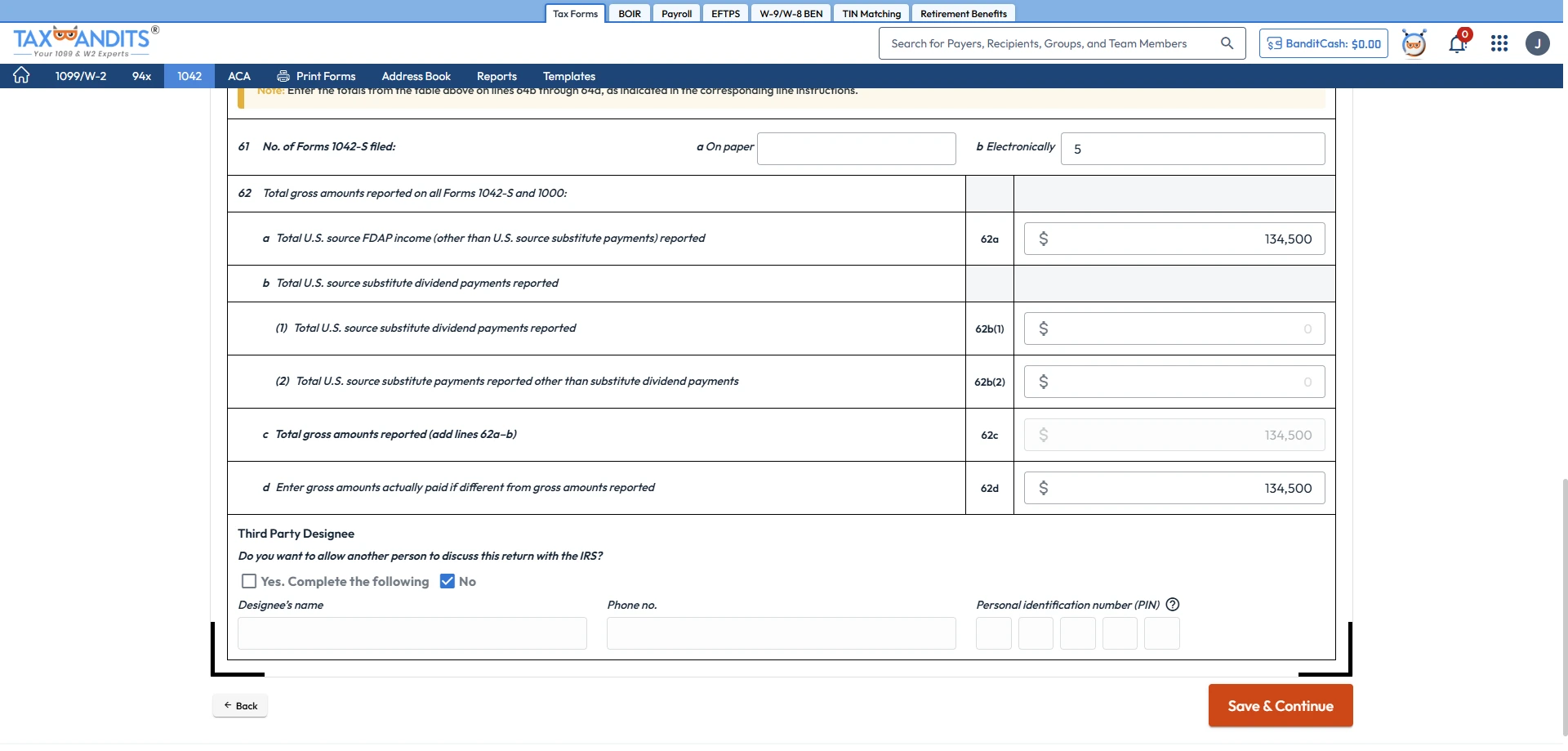

2. Record of Federal Tax Liability Information

- Tax Liability for the Year

- Number of 1042-S Filed Electronically or on Paper

- Total Gross Amounts Reported on Forms 1042-S and 1099

- Total Tax Withheld or Paid

-

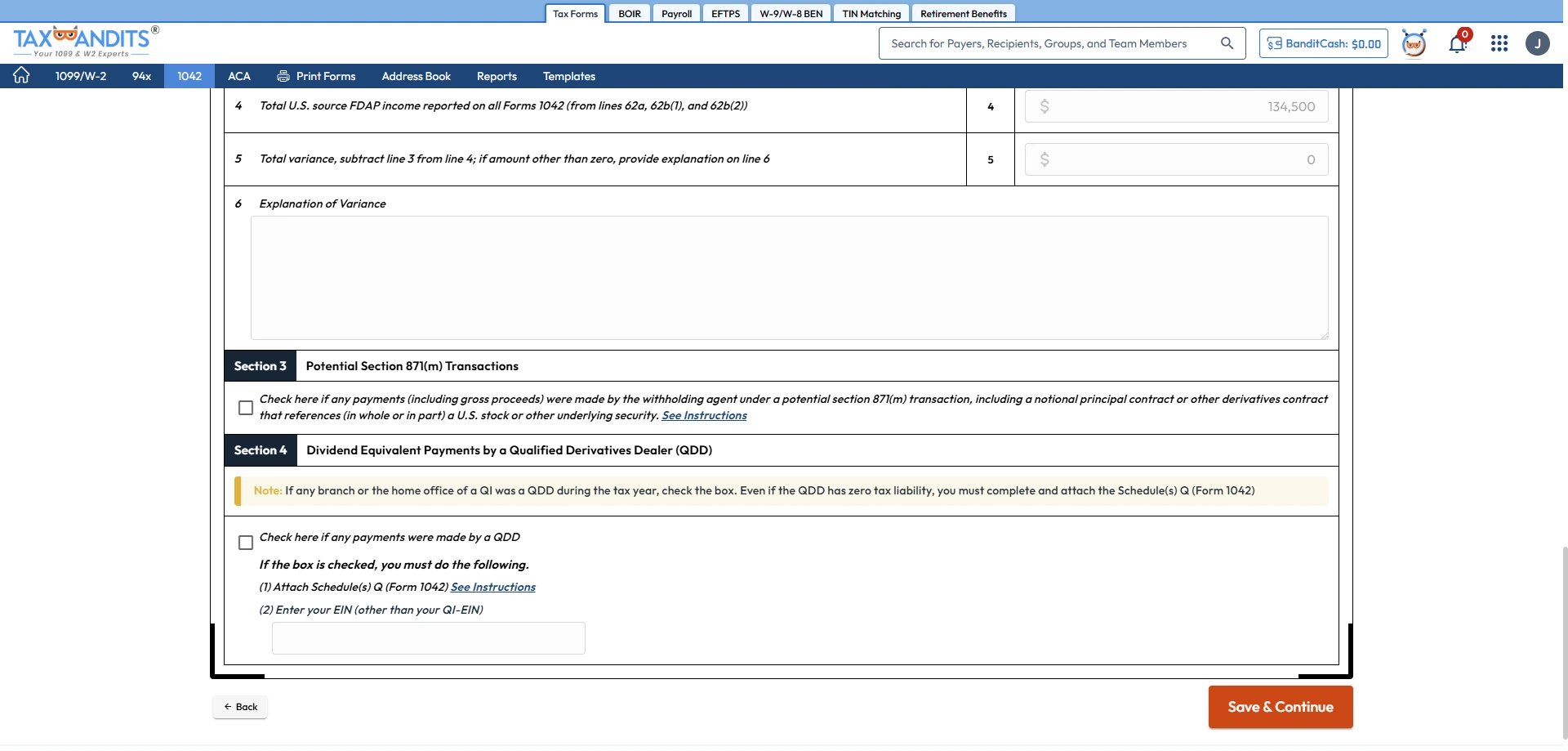

3. Reconciliation of U.S.-Source FDAP Income

- Tax Liability for the Year

- Total U.S.-Source FDAP Income Paid

- Income Reported on Form 1042-S

- Exemptions or Reductions Due to Tax Treaties

-

4. Potential Section 871(m) Transactions

- Total Amount of Dividend Equivalent Payments

- Total Withholding Tax on 871(m) Payments

-

5. Payments by a Qualified Derivatives Dealer (QDD)

- Attach Schedule Q (Form 1042)

- Enter EIN Other Than QI-EIN

Get Started with TaxBandits to E-File your 1042 Online in minutes!

How to File Form 1042 Electronically with TaxBandits?

Create your free account and follow these simple steps to e-file Form 1042 effortlessly!

-

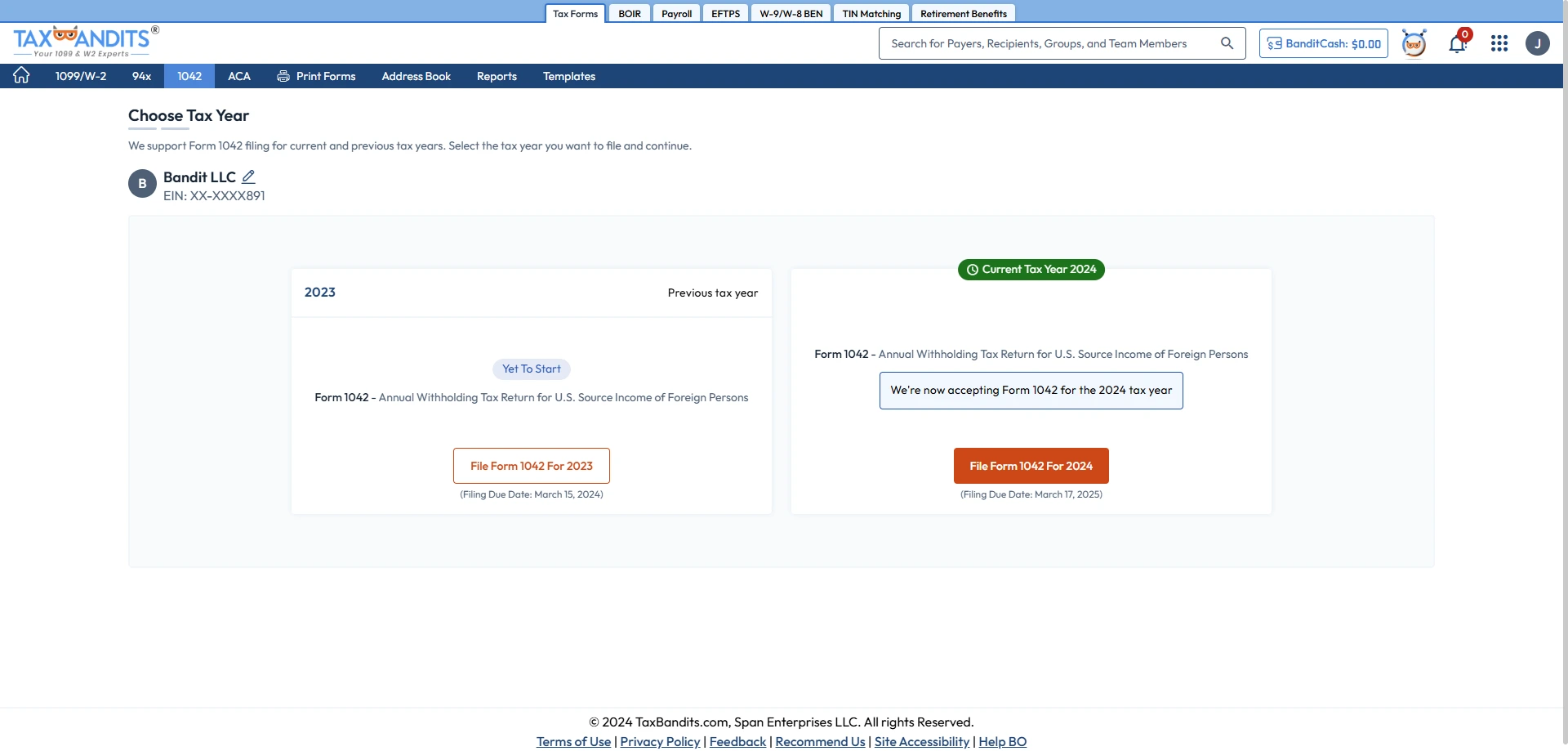

Step 1: Select Form 1042

Choose Form 1042 and select the appropriate tax year.

-

Step 2: Enter Form Information

Enter the Withholding agent details, income type, tax withheld, and any applicable exemptions.

-

Step 3: Review and Transmit

Ensure the entered information is correct. Once confirmed, pay and transmit it to the IRS.

Are you ready to start your Form 1042 filing with TaxBandits?

How to File 1042 Electronically

Our Customer Reviews

Trusted and loved by users like you.

4.9 rating of 52,784 reviews

Trusted and loved by users like you.

4.9 rating of 52,784 reviews

Transparent, Volume-Based Pricing for 1042 Compliance

Scalable per-form pricing designed for businesses of all sizes

|

Form 1042

Pricing per form based on volume |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

|

No. of Forms |

1 |

2-10 |

11-50 |

51-250 |

250+ |

||||||

|

Federal Filing |

$9.95 |

$8.95 |

$8.05 |

$7.25 |

$6.55 |

||||||

|

Form 1042

Pricing per form based on volume |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

|

No. of Forms |

Federal Filing |

||||||||||

|

1 |

$9.95 |

||||||||||

|

2-10 |

$8.95 |

||||||||||

|

11-50 |

$8.05 |

||||||||||

|

51-250 |

$7.25 |

||||||||||

|

250+ |

$6.55 |

||||||||||

Frequently Asked Questions on 1042 Filing

What is Form 1042?

Form 1042, Annual Withholding Tax Return for U.S. Source Income of Foreign Persons, is used to report withholding on U.S. source income paid to foreign persons, including interest, dividends, and other FDAP income.

Get detailed information about IRS Form 1042.

What’s new in Form 1042 for the 2025 Tax Year?

The following are the changes made by the IRS to Form 1042 for 2025:

- New Rule for Borrow Fees (Notice 2025-63)

- Updated Refund Claim Requirements for Withholding Agents

- Direct Deposit Now Encouraged for Refunds

- New Direct Deposit Information Lines Added (71b–71d)

- IRS Direct Pay Added as a Payment Option

- Credit Forward Framework Eliminated After 2024

Check out our latest article to know more about the changes to Form 1042.

Who Must File Form 1042?

Form 1042 is required for entities that withhold tax on U.S. source income paid to foreign persons. This includes:

- U.S. financial institutions and businesses making payments to foreign individuals or entities

- Withholding agents responsible for tax deductions on FDAP income

- Qualified Intermediaries and certain foreign partnerships

For more detailed information on this,

click here.

What is Schedule Q (Form 1042)?

Schedule Q (Form 1042) provides detailed information about the tax liability of Qualified Derivatives Dealers (QDD), even if a particular QDD has no tax liability. This schedule is part of the annual reporting requirements for U.S. source income paid to foreign persons and is related to the reporting of withholding taxes.

What’s New?

Schedule Q has been amended to reflect Notice 2024-44, which extends the transition relief for certain provisions of the section 871(m) regulations. This change affects Qualified Derivatives Dealers (QDDs) and their reporting requirements.

What are the Chapter 3 and 4 status codes on Form 1042?

On Form 1042, Chapter 3, and Chapter 4, status codes are used to identify the specific classification of withholding agents and recipients under U.S. tax laws. These codes are important for determining tax withholding and reporting requirements under Chapters 3 and 4 of the Internal Revenue Code (IRC).

- Chapter 3 Status Codes: Chapter 3 governs withholding tax on payments of U.S.-source income made to foreign persons. The status codes identify the recipient type under Chapter 3.

- Chapter 4 Status Codes: Chapter 4 refers to the Foreign Account Tax Compliance Act (FATCA), which aims to prevent U.S. tax evasion by requiring foreign financial institutions (FFIs) and other entities to report U.S.-owned accounts. Status codes under Chapter 4 identify the recipient or withholding agent's FATCA classification.

When is the deadline to file Form 1042?

The Form 1042 due date falls on the 15th day of the third month after the end of the calendar year (March 15). If the due date falls on a Saturday, Sunday, or federal holiday, file Form 1042 by the next business day.

Check out the 1042 deadline for the 2025 tax year.

What happens if I don't file Form 1042?

If you file Form 1042 late or fail to pay or deposit the tax when due, you may be subject to penalties and interest.

Get more information about Form 1042 penalties for late filing and payments.

Helpful Resources to File 1042 Online

What is Form 1042

Form 1042 Instructions

Form 1042 Due Date

Form 1042 Penalties

Form 1042 Mailing Address

Form 1042 and 1042-S

Helpful Resources to File 1042 Online

Ready to File Form 1042 Online?

Trusted by Business Owners and Tax Professionals