Form 941 for 2026: Employer’s Quarterly Federal Tax Return

If you’re an employer paying wages to employees, you’ll likely need to report quarterly payroll taxes using Form 941 for 2026. This guide covers everything you need to know to complete and file it accurately.

By Charles Hardy | Last Updated: March 31, 2026

Key Points about Form 941:

- Purpose – Reports federal income tax withheld and employer/employee Social Security and Medicare taxes.

- Taxes Reported – Total wages paid, tips received, federal tax withheld, and applicable tax credits or adjustments.

-

Deadline – Due quarterly on the last day of the month following the end of

each quarter.

Form 941 - Employers Quarterly Federal Tax Return

Table Of Contents:

- What is a 941 Form?

- Who is required to file Form 941?

- Who is exempt from filing Form 941?

-

What information is reported on the

941 Form? - What are the 2026 updates to Form 941?

- How do you file Form 941?

- When is Form 941 due?

- What happens if you file Form 941 late?

-

How can you correct mistakes on

Form 941? -

What is Form 941?

Form 941, Employer’s Quarterly Federal Tax Return, is an IRS form used to report federal income tax, Social Security, and Medicare taxes withheld from employees’ paychecks. Employers also use it to report and pay their own share of Social Security and Medicare taxes.

So, if you’re an employer who pays wages to employees, you’re generally required to file federal Form 941 each quarter to report these payroll taxes.

Get Your Free Form 941 E‑Book Now

New to Form 941 filing? Download our free e-book to get:

- A clear breakdown of Form 941

- Key deposit requirements you can’t miss

- Simplified methods for efficient filing—and more

Who is required to file tax Form 941?

- If you’re an employer who pays wages subject to federal income tax withholding, Social Security tax, or Medicare tax, you’re required to

file Form 941. -

If you did not pay any employees during the quarter and have

no taxes to report, you’re still required to file Form 941, unless you’ve filed a final return or qualify for an exception.

File Your Form 941 Confidently

TaxBandits, an IRS-authorized e-file provider, makes your

941 quarterly

tax filing easy, quick, and error-free.

Who is Exempt from Filing the 941 Form?

You may not need to file a 941 form if:

- You're a seasonal employer and didn’t pay wages during

the quarter - You employ farm workers (file Form 943 instead)

- You employ household workers (report using Schedule H with your Form 1040)

- Your total annual tax liability is less than $1,000, and the IRS has notified you to file Form 944 annually instead

What Information is Reported on the

941 Form?

Here’s a quick walkthrough of what you’ll need to report on the 941 form (refer to the image for visual guidance):

-

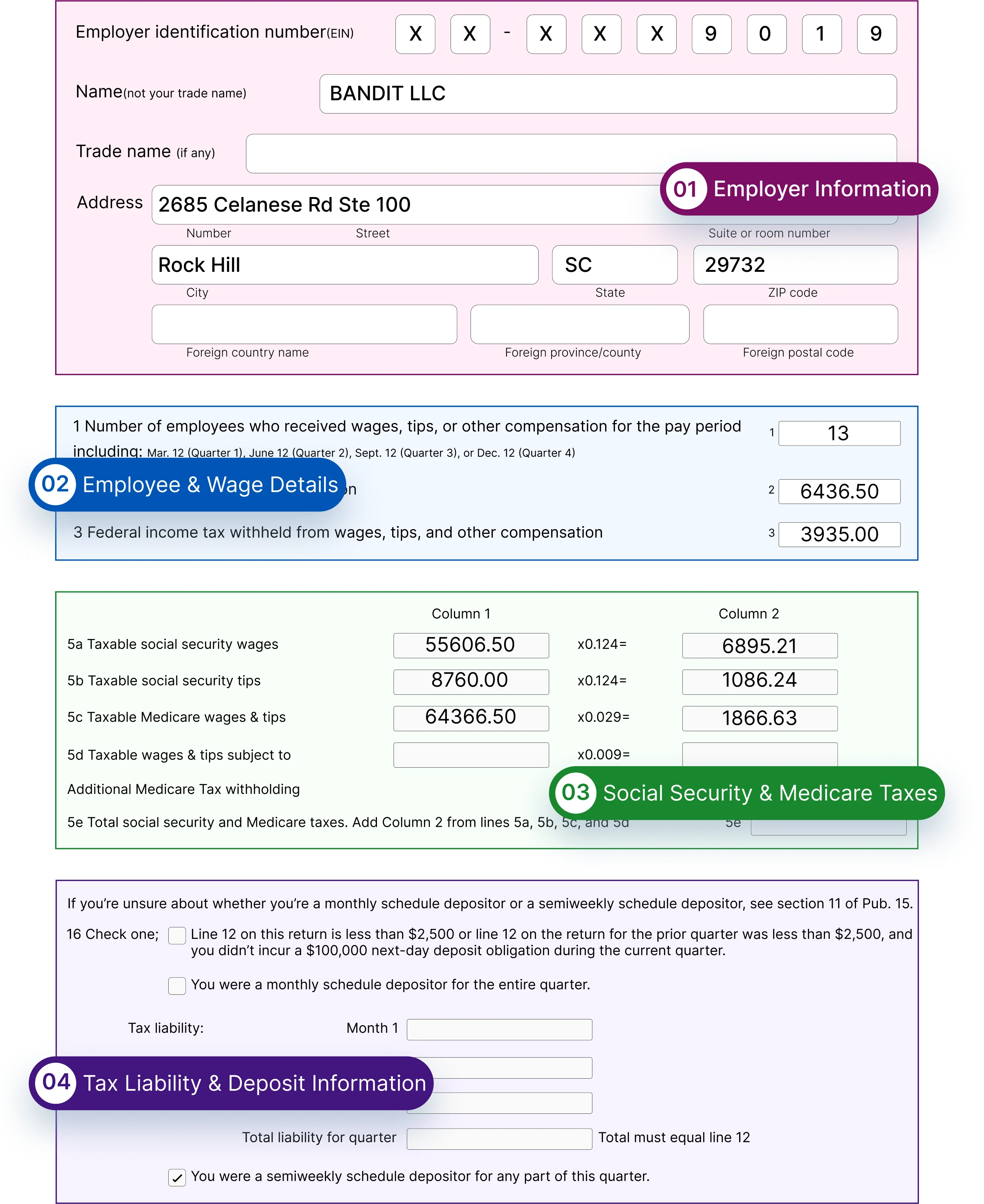

1. Employer Information

Provide your EIN, business name, and address (See label 1

in the image). -

2. Employee & Wage Details

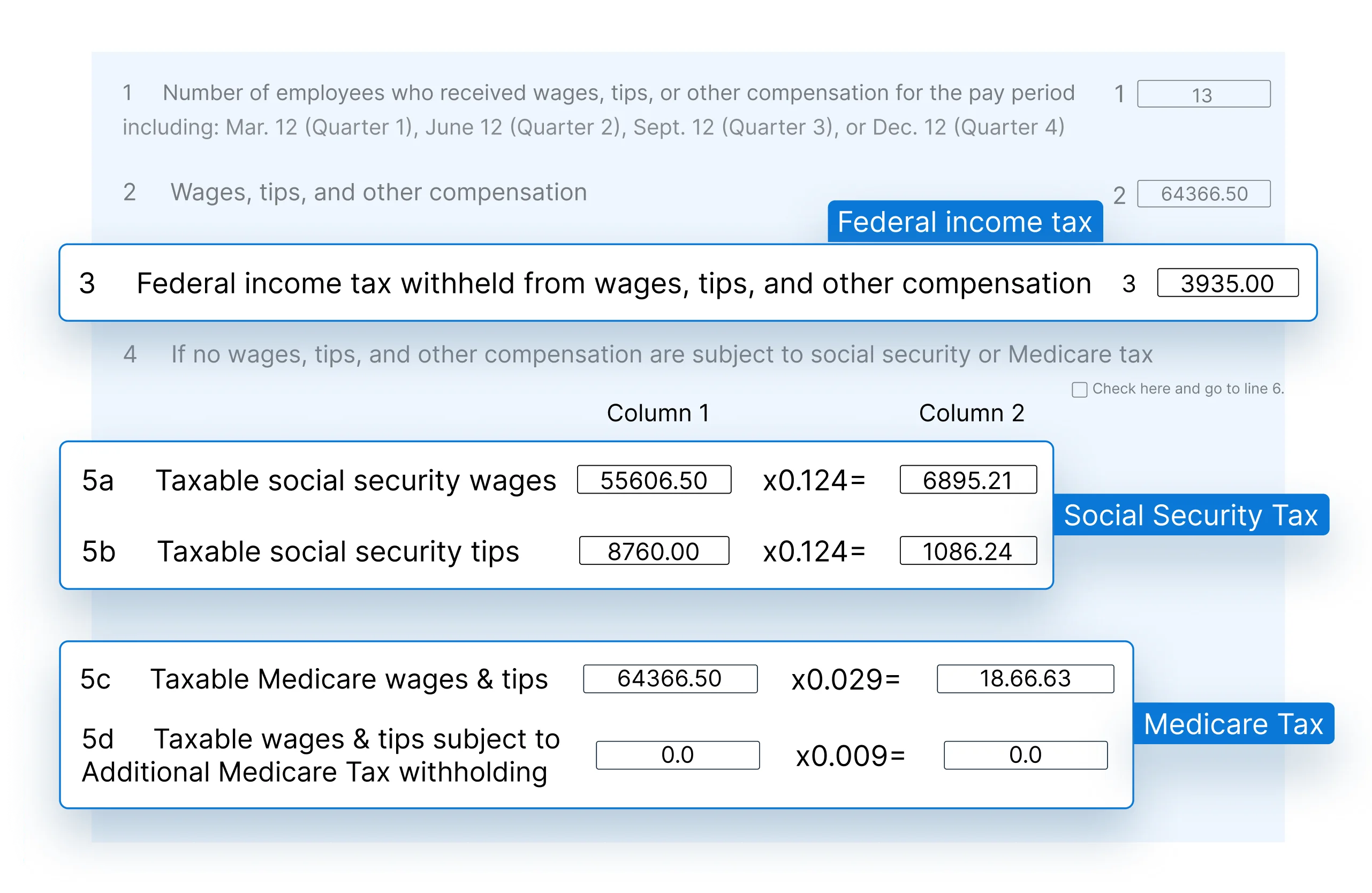

Report the number of employees, total wages paid, and federal income tax withheld for the quarter (See Lines 1–3 under label 2).

-

3. Social Security & Medicare Taxes

Include the amount of Social Security and Medicare taxes withheld from wages (See Lines 5a–5e under label 3).

-

4. Tax Liability & Deposit Information

Indicate whether you’re a monthly or semiweekly depositor and provide a breakdown of your tax liability by month (See label 4

in the image).

Check out our article for step-by-step instructions to complete your

941 Form.

Understanding Payroll Tax Calculations

When calculating the total amount owed to the IRS, remember:

-

Social Security tax: 6.2% withheld from the employee and 6.2% paid by the employer, up to a wage limit of $184,500

for 2026. - Medicare tax: 1.45% withheld from the employee and 1.45% paid by the employer. There's no wage base limit.

- Additional Medicare tax: Withhold an extra 0.9% from employee wages exceeding $200,000—this is employee-only and has no employer match.

As an employer, you're responsible for withholding these taxes from each paycheck and submitting both the employee and employer portions to the IRS.

Tip: The image highlights where to report each item on Form 941—making it easier for you to fill out with confidence.

IRS Form 941 Updates for 2026: What You Need to Know

The IRS has released Form 941 for the 2026 tax year, bringing a few important updates. These include an increase in the Social Security wage base limit and updated tax thresholds for household and election workers.

Additionally, the IRS has included a dedicated checkbox section for aggregate filers and new fields to enter bank account information to claim refunds for overpayment amounts reported on Form 941.

How to file your 941

Quarterly Report?

You can either file Form 941 electronically or by mailing a paper return to the IRS. However, the IRS recommends e-filing 941, as it is generally faster, more secure, and provides instant confirmation.

If you still choose to file 941 on paper, you can complete the form and mail it to the IRS. The mailing address depends on your business’s location and whether payment is included.

If you need to send a payment, mail a check made out to the U.S. Treasury along with the form, or pay online via the Electronic Federal Tax Payment System.

Form 941 Reporting Made Simple – Fast, Secure, and IRS-Authorized!

When tax deadlines come, TaxBandits is here to help you. TaxBandits offers error-free filing and

guaranteed acceptance, giving you peace of mind.

When is the due date to file Federal

Form 941?

You are required to file Form 941 on the last day of the month following each quarter. Check the Form 941 filing deadlines for each quarter of the 2026 tax year.

Never Miss Your Deadlines –

Get Alerts!

Stay informed about your quarterly Form 941 tax filing with free deadline alerts from TaxBandits.

What happens if you file Form 941 late?

If you fail to file a Form 941 on or before the due date, you may be subject to a penalty of 5% of the unpaid tax amount for each month the return is late. The penalty will be up to a maximum of 25%.

Check out our article about Form 941 penalties.

How can you correct a mistake made on

Form 941?

If there is any error on your previously filed Form 941, it must be corrected using Form 941-X. You must use a separate Form 941-X for each quarter or Form 941 that needs correction.

Until 2023, Form 941-X can only be filed on paper. However, starting in 2024, the IRS supports the e-filing of 941-X.

Form 941 corrections are included at no extra cost when you file your original return with TaxBandits. Learn More

Article Sources:

- Internal Revenue Service. "Form 941: Employer’s Quarterly Federal Tax Return".

- Internal Revenue Service. "Instructions for Form 941".

- Internal Revenue Service. "Schedule B (Form 941): Report of Tax Liability for Semiweekly Schedule Depositors".

- Internal Revenue Service. "Form 941-X: Adjusted Employer’s Quarterly Federal Tax Return or Claim for Refund".

- Internal Revenue Service. "Publication 15".

Ready to Start Filing Your Form 941?

Related Topics

IRS Form 941

- Form 941

- Form 941 Instructions

- Form 941 Due Dates

- Form 941 Mailing Address

- Form 941 Schedule B

- Form 941 Penalty

- Form 941 ERC

- Form 940 vs 941

- Form 941 vs 944

Revised Form 941 for 2023

Form 941 Worksheets

- Form 941 Worksheet 4 for Q3 & Q4 2021

- Form 941 Worksheet 2 for Q2 2021

- Form 941 Worksheet 1

- Form 941 Worksheets

IRS Form 941-X

Revised Form 941 for 2022

Revised Form 941 for 2021

- IRS Form 941 for Q4 2021

- Revised Form 941 for 2nd Quarter, 2021

- Form 941 Quarter 2 vs Quarter 1, 2021

- Revised Form 941 Schedule R for Q2 2021

- Revised Form 941 for 1st Quarter, 2021