Trusted by Leading Payroll & Compliance Experts

The Industry’s Only 941 Schedule R Filing Solution — Over a Decade of Expertise

Only a few providers offer a 941 Schedule R filing solution—and TaxBandits stands out as the most reliable. Enterprises nationwide trust us to simplify compliance, reduce risk, and deliver filings with unmatched accuracy.

Or call us at (704) 684-4758 for customized pricing.

Scale Without Stress

Handle aggregate filings for thousands of clients effortlessly. No matter the volume, TaxBandits keeps the process seamless.

Data Imports Made Simple

Eliminate the hassle of gathering payroll data from multiple sources with seamless upload and integration options.

File Confidently & Stay Compliant

Built on enterprise-grade compliance and IRS security standards. Our compliance ensures peace of mind with every filing.

Or call us at (704) 684-4758 for customized pricing.

From Data Import to IRS Filing—Manage Your 941 Schedule R Workflow Seamlessly

Effortlessly manage client data with a flexible data import option

-

Simple Data Input

Enter client data directly into the system—ideal for small volumes of filing.

-

Bulk upload (Excel)

You can bulk upload Schedule R data using Excel, saving time and simplifying the process for multiple clients. Download Template

-

API integration

File directly from your software by integrating with our API. Explore More

Ensure Accuracy and Stay Compliant—Tools That Work for You

-

Accurate data checks

Your Form 941 Schedule R data is automatically validated to catch errors and prompts you to fix them instantly before filing.

-

Built-in reconciliation

Our system automatically reconciles totals from Schedule R with Form 941, ensuring that client allocations match IRS reporting requirements.

-

Easy signature options

Easily e-sign your forms using Form 8453-EMP or an Online Signature PIN. If you don’t have a PIN yet, just request one—it’s free!

Start filing smarter with TaxBandits—making Schedule R easy, accurate, and fully compliant.

Powerful Features Built for Aggregate Filers

Team Management

Invite team members to your account and assign them specific roles—such as preparer, approver, or transmitter—to streamline the filing process.

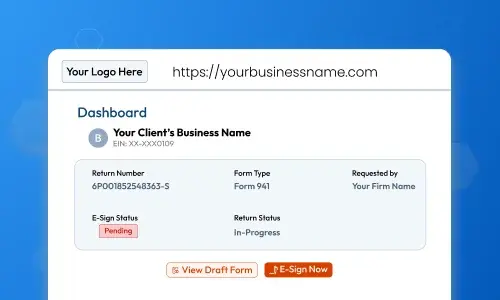

Client Management

Provide your clients with a secure, customized portal featuring your brand logo, theme, and URL, enabling them to e-sign documents and track their filing status.

Email Customization

Customize the sender name and 'From' address on all outgoing emails to align with your firm's branding, fostering trust with your clients.

Automate your client’s filing with our developer-friendly API

-

Free developer account

Get started at no cost with access to all developer tools and resources.

-

Free secure sandbox environment

A safe testing space where you can try out your integrations without affecting real data.

-

Open SDK libraries

TaxBandits offers SDK libraries in various programming languages that help you use our API.

What You Need to File Form 941 Schedule R Online

Ensure you have these details ready before you start filing, for a smooth and timely e-file experience:

-

1. Your Firm Details

- Your legal business name and EIN

- Quarter and tax year you’re filing for

- File type (CPEO, Section 3504 Agent, or other third party)

- Contact information (address, phone, email)

-

2. Aggregate 941 Data

- Total wages, taxes, and deposits reported on your aggregate Form 941

- Form 941 Schedule B information (if you're a semiweekly depositor)

- Form 8453-EMP (if required for e-signature authorization)

-

3. Client-Specific Information (for each client included in Schedule R)

- EIN and legal business name

- Allocated wages and tips

- Federal income tax withheld

- Allocated Social Security and Medicare taxes (including any rounding adjustments)

Need Help Bringing in Your Clients’ Payroll Data?

Our support team can help you get set up with bulk imports or API integration.

How to File Form 941 Schedule R Online with TaxBandits?

-

Step 1: Set Up Your Filing

Select the tax year, quarter, and filer type (CPEO, Section 3504 Agent, or other third party). Enter aggregate wage and tax data for all clients under your EIN, including Schedule B if applicable.

-

Step 2: Complete Client Details & Validate

Enter client-specific information manually or import in bulk via Excel. TaxBandits automatically validates data and reconciles totals with Form 941 to ensure accuracy and compliance.

-

Step 3: Review & E-File Securely

Confirm everything using the Reconciliation Summary, collaborate with clients via the portal if needed, then authorize and transmit your return securely to the IRS.

From Complex to Compliant: Real Stories, Real Results

See how professionals like you have transformed their filing process with TaxBandits.

Simple, Transparent Pricing

Scale your filing easily with pricing that adjusts to the number of Schedule R lines you need.

Advantanges of Choosing

Our Software

- Includes 8974, Schedule B, 8453-EMP

- Free retransmission of rejected returns

- Customizable client portal

- World-class support from sign-up to acceptance

Pay as You Go

$9.95/Form

+$0.50 /per Schedule R line

No Subscriptions. No hidden fees.

Just simple, straightforward pricing.

For high-volume filing, call us at (704) 684-4758 for customized pricing.

Frequently Asked Questions

What is Schedule R (Form 941)?

CPEO's and Section 3504 reporting agents are required to attach Schedule R (Form 941) to the aggregate

Form 941. Schedule R simplifies the aggregate reporting process by allocating aggregate wages reported on Form 941 to each of

their clients.

Generally, CPEO's are required by the IRS to file their Schedule R electronically and can file the returns listed on Form 8973. Also, Section 3504 Agents can file the returns listed on their Form

2678 appointment.

Aggregate filers can use their own EIN to file a single Form 941 for all their clients with Schedule R along with their respective wage and tax liability information for the tax period.

Who must File Form 941 Schedule R?

Form 941 Schedule R must be filed by Agents approved by the IRS, under Section 3504, CPEOs, and Other third-party payers such as non-certified PEOs.

Certified Professional Employer Organization (CPEO):

- For all the clients, the aggregate returns filed and Tax paid is under the EIN of CPEOs

- CPEO is solely responsible for timely filing and deposit of taxes withheld.

Section 3504 Agent:

- For all the clients, the aggregate returns filed and Tax paid is under the EIN of Section 3504 Agent

- Both the Employer and 3504 Agent are liable for timely filing and deposit of taxes withheld.

- To request approval to act as an agent for an employer under section 3504, the agent must file Form 2678 with

the IRS.

Other third-party payers (Non-Certified PEOs):

- A Professional Employer Organization (PEO) is a type of third party payer who is responsible for filing and tax payments of the employer.

What are the latest updates in Form 941 Schedule R?

The March 2024 revision of Schedule R introduced several notable changes and reverted to a previous format used in March 2022. Here are the key points explained:

Fundamental Changes in the March Q1 2024 Revision of Schedule R are

- Reverted Format: The Schedule R format has returned to the layout used in the March 2022 revision in which certain columns are now "Reserved for future use" once again, indicating they are not required to be filled out. The following columns include:

- Column m- Form 941, line 11d-Nonrefundable portion of the credit for qualified sick and family leave wages for leave taken after March 31, 2021, and before October 1, 2021

- Column s- Form 941, line 20-Qualified health plan expenses allocable to qualified family leave wages for leave taken before April 1, 2021

- Column t-Form 941, line 23-Qualified sick leave wages for leave taken after March 31, 2021, and before

October 1, 2021 - Column v- Form 941, line 25- Amounts under certain collectively bargained agreements allocable to qualified sick leave wages reported on line 23.

The Schedule R March 2024 revision can be used for quarters starting after December 31, 2023, while the previous version of Schedule R can be used for quarters starting before December 31, 2023.

- When these revisions are applicable:

- The Schedule R March 2024 revision should be used for quarters starting after December 31, 2023.

- Exceptionally, it might be used for filing Form 941-X (Adjusted Employer's QUARTERLY Federal Tax Return or Claim for Refund) for quarters before January 1, 2024. An example is if a client is eligible for the COBRA premium assistance credit after the first quarter of 2022.

- Calendar Year Field: The calendar year field on Schedule R is no longer filled in automatically. This means users now have to enter the year themselves.

- New Checkbox: A new checkbox has been added to indicate whether Schedule R is attached to Form 941 (Employer's QUARTERLY Federal Tax Return) or Form 941-X (Adjusted Employer's QUARTERLY Federal Tax Return or Claim for Refund). This helps clarify the context in which Schedule R is being used.

- Column Usage: Columns f, l, n, o, p, u, w, x, and y on Schedule R are required only when the schedule is attached to Form 941-X (Correction form or ‘Adjusted Employer's QUARTERLY Federal Tax Return or Claim for Refund’). This means you should only fill out these columns if you are using Schedule R to correct a previously filed Form 941. It is essential to understand this distinction to ensure you complete the form correctly and comply with IRS regulations. If Schedule R is not being used with Form 941-X, these columns should be left blank.

Note: Form 941 for 2026 no longer includes specific lines mentioned above for claiming qualified sick and family leave wages or COVID-19-related credits. As a result, employers will need to be aware of these changes when preparing their tax filings.

- Expected Future Use: The IRS expects that this revised Schedule R and its instructions will be used for the second, third, and fourth quarters of 2024 and potentially for a more extended period.

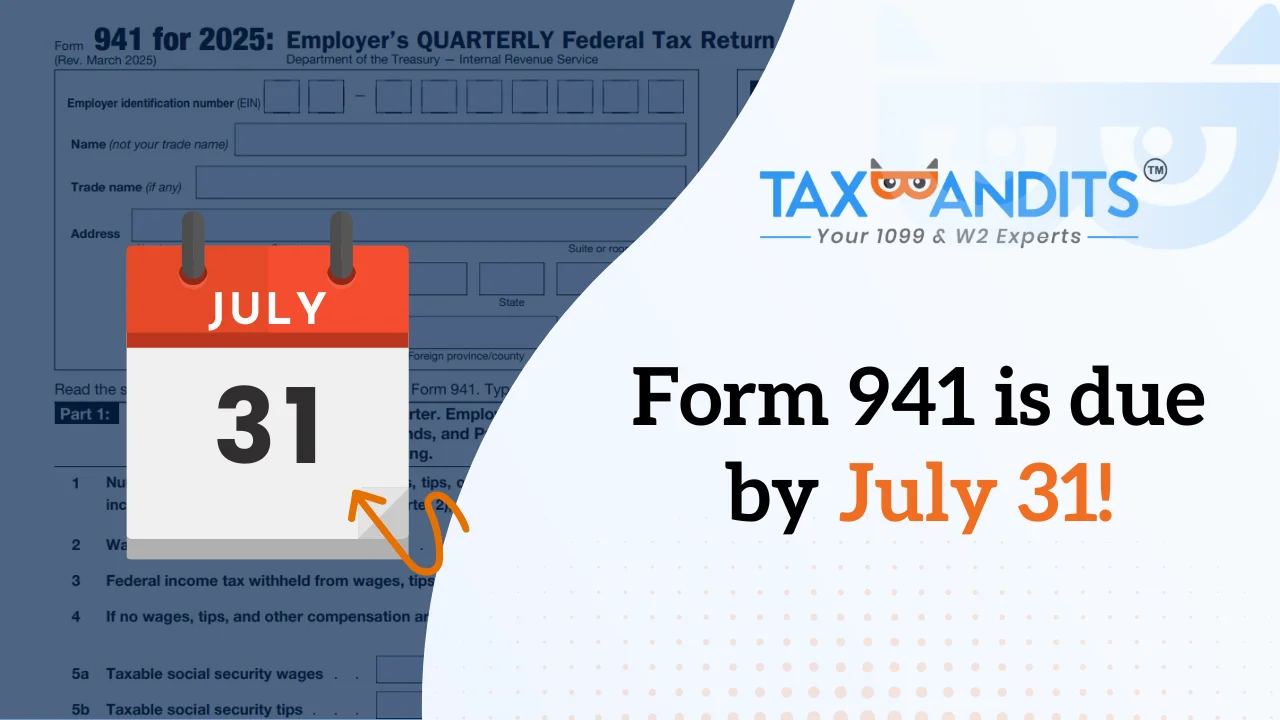

When is the 2026 Form 941 Schedule R due?

Form 941 Schedule R is generally due by the last day of the month following the end of the quarter. You’re required to file Form 941 for each quarter.

- First-quarter (JAN, FEB, MAR) is due on April 30, 2026

- Second-quarter (APR, MAY, JUN) on July 31, 2026

- Third-quarter (JUL, AUG, SEP) on November 02, 2026

- Fourth-quarter (OCT, NOV, DEC) on February 01, 2027

Click here to learn more about Schedule R (Form 941) deadlines.

What are the penalties for not filing Form 941 Schedule R on time?

Generally, the CPEO is solely responsible for paying the client's employment taxes, filing returns, and making deposits and payments for the reported taxes. IRC Section 3504 Agents and their clients are both responsible for paying their employment taxes, filing returns, and making deposits and payments for the reported taxes. Click here to learn more about Form 941 penalties.

How to Correct Form 941 Schedule R?

You must follow a specific process to amend your Schedule R(Form 941). Here’s a step-by-step explanation.

Steps to Correct Schedule R(Form 941)

- Complete Form 941-X: File Form 941-X, “Adjusted Employer’s QUARTERLY Federal Tax Return or Claim for Refund,” to correct errors on a previously filed Form 941. Fill out Form 941-X with the corrected information. On this form, you'll indicate the specific corrections needed.

-

Attach Corrected Schedule R: Attach the corrected Schedule R to Form 941-X. Ensure that the revised Schedule R reflects accurate information. In schedule R (Form 941), check the box for 941-X, and fill in the Client EIN details followed by the lines corresponding to Form 941-X.

Columns f, l, n, o, p, u, w, x, and y on Schedule R are required only when Form 941-X is attached to it.

- Transmit to the IRS: File Form 941-X along with the corrected Schedule R to the IRS.

Use the above steps if you have missed filing for a client, are considering adding a new client, or need to correct information in a previously filed return.

Helpful Resources

Success Starts with TaxBandits

The Smart Business Owners Choice