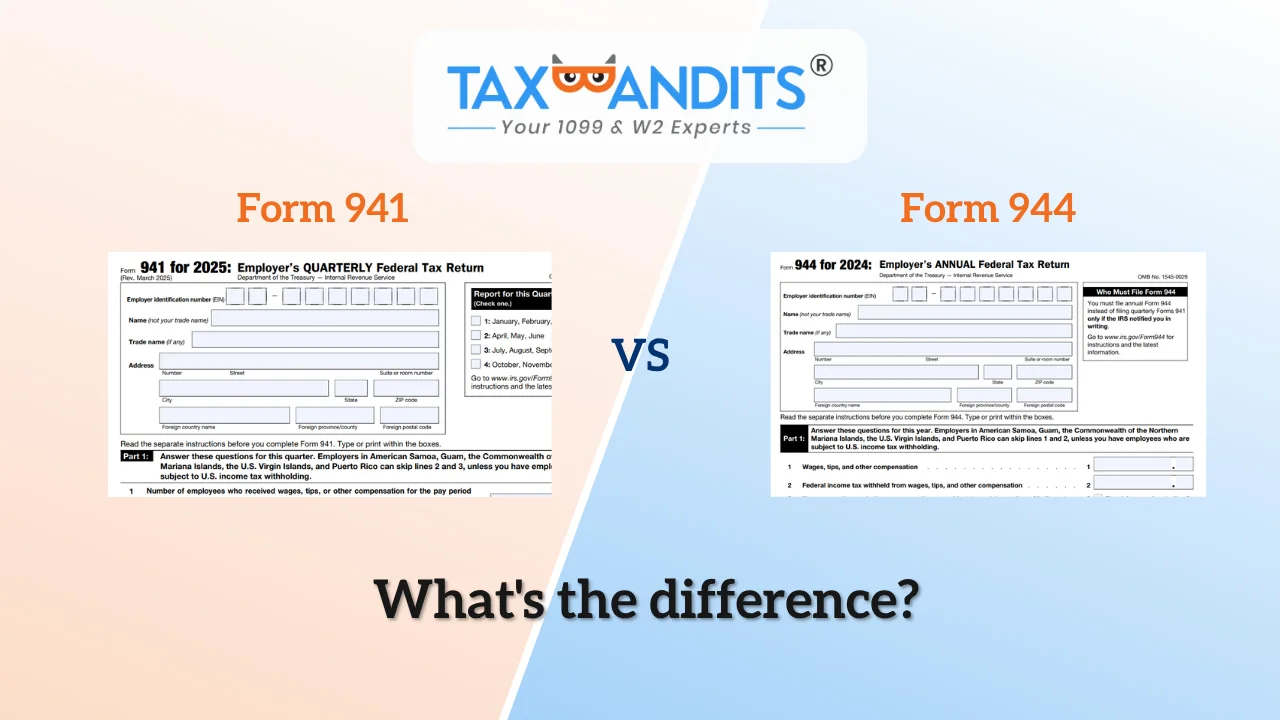

Form 940 vs 941: What’s the Difference?

Form 940 and Form 941 are both IRS payroll tax forms, but they serve different purposes. Form 940 is filed annually to report Federal Unemployment (FUTA) tax, while Form 941 is filed quarterly to report federal income tax withholding, Social Security, and Medicare taxes.

By Charles Hardy | Last Updated:

April 22, 2026

Key takeaways

- Form 940 is filed annually to report Federal Unemployment (FUTA) tax.

- Form 941 is filed quarterly to report federal income tax withholding, Social Security, and Medicare taxes.

- Different purposes: Form 940 reports FUTA tax, which is paid only by the employer, while Form 941 reports payroll taxes, including federal income tax withholding, Social Security, and Medicare (paid by both employer and employee).

-

Most employers need to file both Form 940 and 941 to stay compliant with IRS payroll

tax requirements.

What is the difference between 940 and 941?

Form 940 is used to report FUTA taxes, while Form 941 is used to report federal income tax withheld, Social Security, and Medicare tax withholding.

Check out the table below to find the key differences between Form 940 and 941.

| Form 940 | Form 941 | |

|---|---|---|

| Purpose | Reports Federal Unemployment (FUTA) tax paid by the employer | Reports payroll taxes, including income tax withholding, Social Security, and Medicare |

| Filing Frequency | Filed annually | Filed quarterly |

| Due Dates | January 31 | April 30, July 31, October 31, January 31 |

| Taxes Reported | Employer-paid FUTA tax only | Social Security and Medicare taxes paid by both employer and employee |

| Who is Liable |

Employer only Paid by the employer; it is not withheld from the employee's wages |

Employer and employee Both employee and employer contribute to FICA tax |

Who is required to file Form 940 and Form 941?

Most employers are required to file both Form 940 and Form 941, but the filing requirements differ based on wages and employment.

-

Form 940 must be filed if you:

- Paid $1,500 or more in wages in any calendar quarter, or

- Had at least one employee for 20 or more weeks in a year

-

Form 941 must be filed if you:

- Pay wages subject to federal income tax withholding, or

- Withhold Social Security and Medicare taxes

In general, if your business has employees and processes payroll, you’ll likely need to file Form 941 quarterly and Form 940 annually.

How do you file Form 940 and Form 941?

The IRS allows employers to file Form 940 and Form 941 either electronically (e-file) or by mailing paper forms.

However, the IRS strongly encourages electronic filing, as it is faster, more accurate, and provides confirmation once the return is accepted. Electronic filing also allows you to submit payments securely along with your return.

For businesses managing payroll taxes regularly, using an IRS-authorized e-file provider can simplify the process by:

- Reducing errors

- Ensuring compliance with filing requirements

- Providing real-time status updates

If you’re looking for a faster and more reliable way to file, you can e-file Form 940 and 941 online with TaxBandits and manage your filings in one place.

Success Starts with TaxBandits

The Smart Business Owners Choice