The Bandit Commitment

Ensuring peace of mind for every

941 (sp) Filing.

Filing Form 941 (sp) isn’t just about transmitting it to the IRS! It’s about getting the data right, validating it thoroughly, and owning the right outcome.

The Bandit Commitment defines how TaxBandits approaches compliance: from identifying errors before you file to helping fix them, supporting corrections and retransmissions when needed. We stand with you until your filing is accepted and even beyond.

Getting the right data in

Compliance begins with clean, validated data—long before you start preparing your return.

Simple, guided filing

Navigate every step with clear instructions, real-time AI chatbot assistance, and expert support.

Free corrections & retransmissions

Corrections & retransmissions for your are included with your filing fee.

Money-back guarantee

We do whatever it takes to get your return accepted. If not, your filing fee can be refunded.

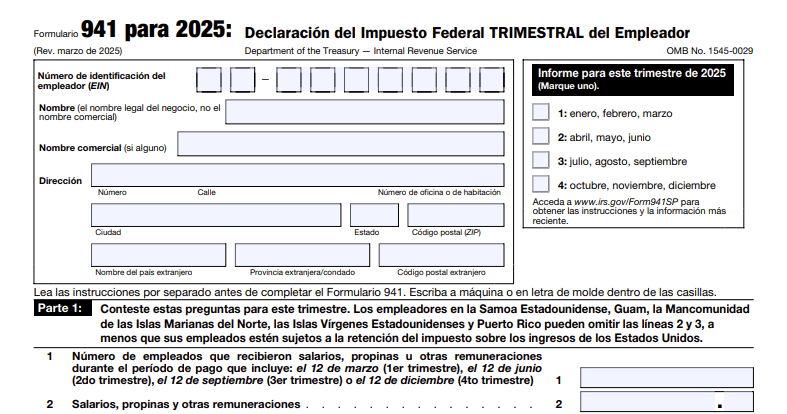

IRS Form 941 (sp) Replaces Form 941-SS and 941-PR

According to the IRS announcement, Form 941-SS and Form 941-PR will no longer be available for tax years beginning after 2024.

Instead, employers in U.S. Territories (American Samoa, Guam, the Commonwealth of the Northern Mariana Islands, and the U.S. Virgin Islands) must file using Form 941.

Those who prefer Spanish can use Form 941 (sp).

Your Trusted Partner for Stress-Free 941 (sp) Filing in Puerto Rico

Discover why employers in Puerto Rico choose TaxBandits for accurate filing.

From Zero Reporting to Bulk Filing—We’ve Got You Covered

-

Easy Zero Reporting

If you had no taxes to report, just select “No Payments” and TaxBandits will generate your zero return with ease.

-

Copy Prior Quarter Data

Copy your previous information into your current 941 (sp) to save time and avoid errors.

-

Filing for Multiple Businesses Made Simple

Upload your data, and our system automatically prepares filings for all your businesses. Download template.

Stay Compliant and File Securely—All in One Place

-

Schedule B (sp) Included

If you are a semi-weekly depositor, the Schedule B (Form 941) (sp) is included at no extra cost, keeping your filing fully compliant.

-

Multiple Tax Payment Options

Easily pay your balance due with EFW, EFTPS, debit/credit card, direct pay, or check/money order — choose what works best for you.

-

Secure Signing Made Simple

Sign your 941 (sp) online using your Online Signature PIN or Form 8453-EMP. You can request a PIN through TaxBandits for free.

Stay compliant with filing made exclusively for Puerto Rico employers

Exclusive Solution Made for Tax Professionals in Puerto Rico

The perfect solution built for accountants, CPAs, 3504 agents, payroll and HCM providers, reporting agents, and more.

Bulk filing made easy

Easily manage filings for a few clients or thousands. Import data with CSV or API, run quick bulk checks, and finish filing faster with reliable tools.

Free Customizable Client Portal

Set up a fully branded client portal where your clients can securely access their returns, e-sign Form 941, and communicate directly with your team—completely under your firm’s branding.

Tailored, Branded Communications

Create a fully customized client experience — customize email sender details, add branded cover letters with your logo, and include notes when sending copies to clients.

Team Access Made Easy

Invite unlimited team members, define roles like Preparer or Approver, share payment access, and let each submit returns with their PTIN.

Flexible payment options

Choose the payment method that works best for you — BanditCash, prepaid credits, or bundle pricing to fit your workflow.

Call us at (704) 684-4758 for custom pricing or request a live demo to see it in action.

How to File Form 941 (sp) Online with TaxBandits?

Create your free account and follow these steps to e-file effortlessly!

-

Step 1: Complete Required Information

Enter your data manually, or use our 941 CSV template to upload filing information in bulk.

-

Step 2: Pay IRS Balance Due (If Any)

Choose your preferred payment option to pay any balance due. You can make EFTPS and credit card payments directly through TaxBandits.

-

Step 3: Review and Transmit

Sign your Form, review the details, and securely transmit it to the IRS. Get instant IRS status updates on your filing.

Ready to File? E-file seamlessly with TaxBandits!

How to E-File Form 941 (sp)?

The Choice of Leading Brands and Tax Professionals

See how professionals like you have transformed their filing process with TaxBandits.

How Much Does It Cost to E-File?

Compare our pricing and benefits to what you pay now

Why Choose TaxBandits?

-

Includes Schedule B (sp), 8974, and

8453-EMP - Free retransmission of rejected returns

- No-cost corrections (941-X)

- Money-back guarantee

- World-class support in Spanish

Pay as You Go

$5.95/Form

Filing more? View Our Volume-Based Pricing

Choose Bundle Pricing

Save 10%

941 (sp)-Only Bundle

Includes 4 × Form 941 (sp)

$23.80 $21.42

Complete 94x Bundle

Includes 4 × Form 941 (sp) + 1 x

Form 940

$29.75 $26.77

Frequently Asked Questions on Form 941 (SP) Filing

What is Form 941 SP?

Form 941 (SP) is the Spanish-language version of Form 941, the Employer's Quarterly Federal Tax Return. Employers in the United States use Form 941 to report their federal income taxes, Social Security, Medicare, and FICA taxes.

Form 941 (SP) serves the same purpose as Form 941 but is provided in Spanish. It includes all the necessary sections and instructions to be translated into Spanish, allowing employers to report their employment taxes accurately.

Who needs to file Form 941 (sp)?

Employers in the U.S. Territories and Puerto Rican have to report their Federal Income, Social Security, Medicare, and FICA taxes on Form 941 SP for 2024. However, if you are looking to report taxes for prior tax years, use Form 941 PR & Form 941 SS.

The IRS has announced that Form 941 PR & Form 941 SS will no longer be available for 2024.

What Information is Required to File 941 SP Online?

Employer Details

- Name, EIN, and Address

Employment Details

- Employee Count

- Employee Wages

Taxes and Deposits

- Federal Income Taxes

- Medicare and Social Security Taxes

- Deposit Made to the IRS

- Tax Liability for the Quarter

Signing Form 941

- Signing Authority Information

- Online Signature PIN or Form 8453-EMP

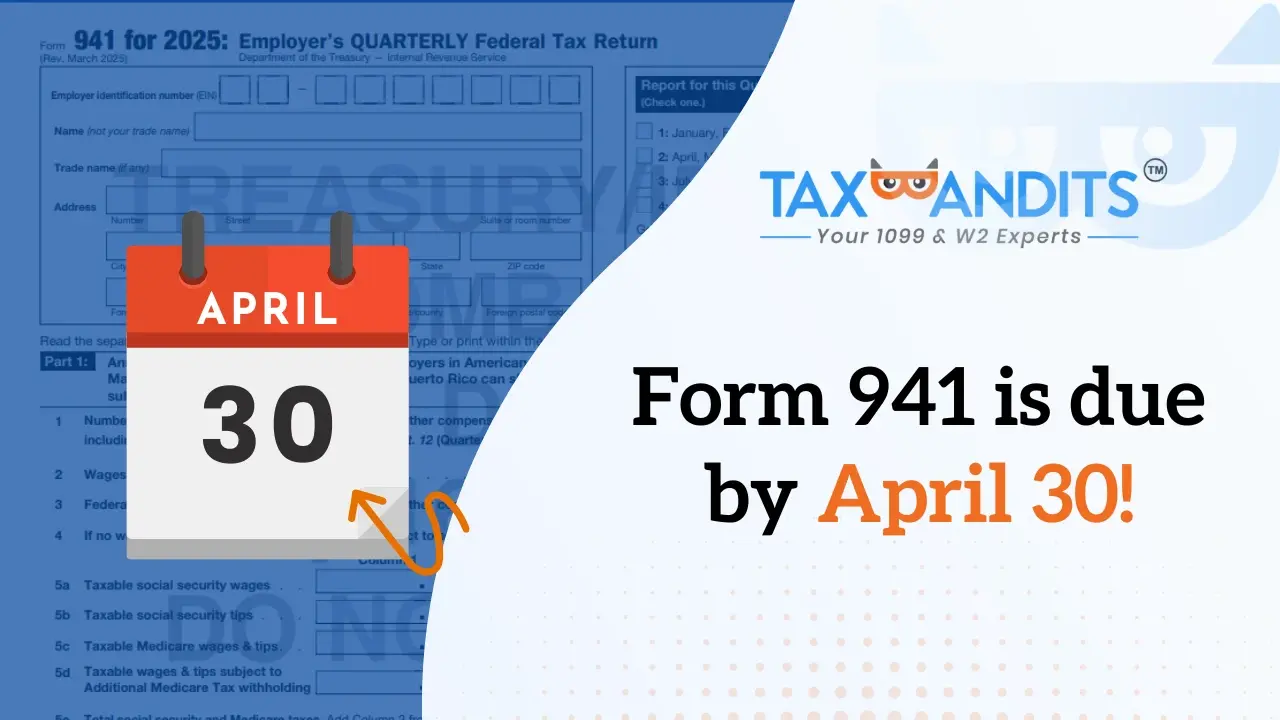

When is Form 941 (sp) due?

The due date to file Form 941 (sp) for the 2026 Tax Year is:

- 1st Quarter (Jan - March): due by April 30, 2026

- 2nd Quarter (Apr - June): due by July 31, 2026

- 3rd Quarter (July - Sep): due by November 02, 2026

- 4th Quarter (Oct - Dec): due by February 01, 2027

What are the Penalties for not filing Form 941 SP?

Employers who file Form 941 SP late will be penalized based on the number of days and a specific condition.

There are two types of penalties for not filing Form 941 SP with the IRS: FTF (failure to file) and FTP (failure to pay).

FTF (failure-to-file):

If you fail to file a return when required, there is an FTF Penalty of 5%. The maximum penalty is generally 25% of the tax due.

FTP (failure-to-pay):

Also, for each whole or part month, the tax is paid late, there is a failure-to-pay (FTP) penalty of 0.5% per month of the tax amount. For individual filers only, the FTP penalty is reduced from 0.5% per month to 0.25% per month if an installment agreement is in effect.

Penalty for not depositing the tax due on time:

| Penalty % | Charged for |

|---|---|

| 2% | Deposits made 1 to 5 days late |

| 5% | Deposits made 6 to 15 days late |

| 10% |

Deposits made 16 or more days late but before 10 days from the date of the first notice the IRS sent asking for the tax due. These amounts should have been deposited but instead paid directly to the IRS or paid with your tax return. However, see Payment with return, earlier in this section, for exceptions |

| 15% | Amounts still unpaid more than 10 days after the date of the first notice the IRS sent asking for the tax due or the day on which you received notice and demand for immediate payment, whichever is earlier. |

TaxBandits Supports Filing of Other 941 Forms

Helpful Resources to File Form 941 (sp) Online

Success begins with TaxBandits

The choice of smart entrepreneurs