IRS Form 1099 MISC Instructions for 2025

Form 1099-MISC instructions help you accurately report miscellaneous income,

stay IRS-compliant, and file before the deadline.

The Internal Revenue Service (IRS) requires businesses to file Form 1099-MISC to report miscellaneous payments, including rent, royalties, prizes, awards, healthcare payments, legal fees, and other payments.

This guide is comprehensive, providing detailed line-by-line instructions for the accurate completion of Form 1099-MISC.

Table of Contents:

How to fill out Form 1099-MISC?

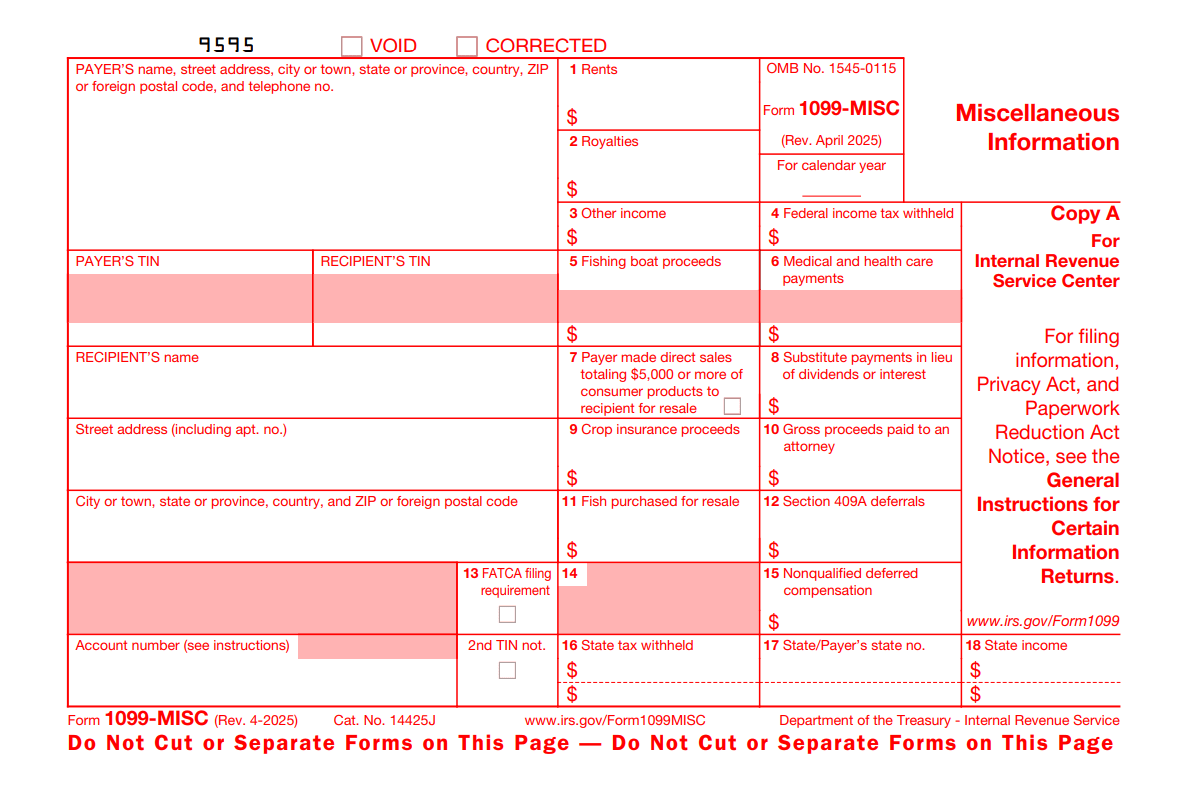

The payers should furnish the following information on 1099-MISC. This includes:

Payer Details:

1. Payer's name

2. Street address, city or town, state or province, country, ZIP, or foreign postal code.

3. Contact number

4. Payer's TIN

Recipient Details:

1. Recipient's name

2. Recipient's TIN

3. Street address (including apt. no)

4. City or town, state or province, country, and ZIP or foreign postal code

5. Check box for 2nd Taxpayer Identification Number (TIN)

In Box 1 to Box 18, the payer reports various payments made and any tax withheld from the contractor/recipient. Here is the breakdown of the line-by-line 1099-MISC instruction guide for reference:

-

Box 1: Rents

Report payment of $600 & above paid as rent.

-

Box 2: Royalties

Report any payments over $10 made to an individual for royalties from oil, natural gas, mineral properties, or Intellectual properties (Copyrights and patents) during the tax year.

-

Box 3: Other Income

Report other $600 or more income that is not reportable in one of the other boxes on the form. This includes prizes, research payments, legal settlements, and deceased employee wages. It does not cover wages (Form W-2) or nonemployee compensation (Form 1099-NEC).

-

Box 4: Federal income tax withheld

Backup withholding applies when a payee has not provided a valid TIN, affecting payments in boxes 1, 2, 3, 5, 6, 8, 9, and 10 on Form 1099-MISC. It also includes income tax withheld from tribal gaming revenue distributions.

-

Box 5: Fishing Boat Proceeds

Fishing boat operators must report each crew member’s share of catch proceeds or fair market value if the boat typically has fewer than 10 crew members. Cash payments of up to $100 per trip for extra duties should also be reported, but wages are on Form W-2.

-

Box 6: Medical And Health Care Payments

Report payments of $600 or more made to physicians, medical and health insurance providers, and other

1099 healthcare service providers, including corporations, except tax-exempt hospitals and government-owned facilities. Payments for prescriptions at pharmacies are not reportable. -

Box 7: Payer made direct sales totaling $5,000 or more of consumer products to the recipient for resale

Check this box (no dollar amount required) if you made direct sales of $5,000 or more for resale outside a retail store. You can report it on Form 1099-MISC or 1099-NEC, but not both.

-

Box 8: Substitute payments in lieu of dividends or interest

Report average substitute payments of $10 or more made in lieu of dividends or tax-exempt interest for a customer's securities loan. Substitute payments include interest accrued on securities.

-

Box 9: Crop insurance proceeds

Report the crop proceeds of $600 or more paid to a farmer by an insurance company unless the farmer informed the insurance companies that expenses have been capitalized under sections 278, 263A, or 447.

-

Box 10: Gross proceeds paid to an attorney

Report $600 or more paid to attorneys in legal settlements, even if services were performed for another party.

-

Box 11: Fish Purchased for Resale

Report $600 or more in cash payments to fish sellers if you are in the business of purchasing fish for resale.

-

Box 12: Section 409A deferrals

Report current year deferrals of a nonemployee under a nonqualified deferred compensation (NQDC) plan if it is subject to section 409A and any earnings on current and prior year deferrals.

-

Box 13: FATCA Filing Requirement

This box must be checked to confirm FATCA compliance under Chapter 4 of the IRC. U.S. payers and Foreign Financial Institutions (FFIs) use it to report U.S. accounts or elect to report under FATCA, even if no reportable payments were made.

-

Box 15: Nonqualified deferred compensation

Report payments under an NQDC plan that do not meet the requirements of section 409A. Any payment reported in box 12 is taxable and included in this box.

-

Box 16 to Box 18: State Information

Used for state tax reporting, including state tax withheld (Box 16), state name & ID (Box 17), and state payment amount (Box 18).

Click here to learn more about 1099-MISC State Filing Requirements.

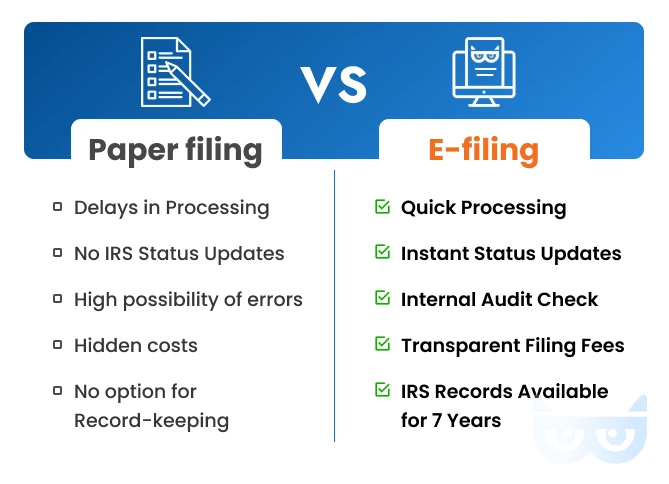

Switch to E-Filing for Form 1099-MISC Today!

Are you ready to file Form 1099-MISC? Create a free account with TaxBandits and e-file your Form 1099-MISC with the IRS and state agencies in just a few minutes. You can also provide recipient copies by postal mail or through online access.

Why is e-filing the best option for filing Form 1099-MISC?

The IRS requires that businesses or individuals file 10 or more 1099-MISC forms electronically instead of mailing paper copies. Furthermore, the IRS strongly encourages electronic filing of 1099-MISC forms to ensure faster processing.

What is the deadline for filing the 1099-MISC in 2026?

The Form 1099-MISC reporting deadlines for the tax year 2024 are listed below.

| Type of Filing | Deadline |

|---|---|

| Sending recipients of 1099-MISC |

February 2, 2026 Get started with TaxBandits and your recipient copies will be delivered on time. |

| Paper filing 1099-MISC | March 2, 2026 IRS suggests filers to file 1099 MISC electronically for quick processing andinstant approval |

| E-filing 1099-MISC | March 31, 2026 Create a free account with TaxBandits today and E-file 1099 MISC in minutes. |

The deadline for sending COPY B to the recipient is February 17, 2026, if you report payments only in box 8 or 10.

Never miss your 1099-MISC deadline

File on-time with TaxBandits and avoid falling into late filing penalties Get Started with Taxbandits and

file your 1099-MISC file in few simple steps.

What are the different copies of Form 1099-MISC?

Form 1099-MISC contains several copies, each serving a unique purpose.

- Copy A: This copy is transmitted electronically to the IRS

- Copy B: This copy is furnished to the vendor/recipient.

- Copy 1: This copy is for state tax filing if needed.

- Copy 2: This copy must be filed with the recipient’s state income tax return if required.

Are you concerned about managing multiple copies of Form 1099-MISC?

Make the switch to TaxBandits today! E-file your 1099-MISC with the IRS and state in just a few simple steps. TaxBandits can also send copies to your recipients via postal mail and online access. Create a Free Account Now!

E-File Form 1099-MISC in minutes with TaxBandits

TaxBandits, an IRS-authorized provider, offers a seamless and secure solution for e-filing your 1099-MISC forms, delivering a streamlined experience with numerous intuitive features. Here are a few simple steps to file your 1099-MISC:

- Step 1: Create a free TaxBandits account or log in if you already have one.

- Step 2: Enter Form 1099-MISC information.

- Step 3: Review the form information.

- Step 4: E-file it with the IRS and the state.

TaxBandits simplifies tax compliance with features like TIN matching and internal audits to ensure accurate filings. Effortlessly file multiple returns using our custom Excel and CSV templates. Easily distribute recipient copies through postal mail or secure online access. With our W-9 Manager, you can request W-9 forms and manage them all in one place.

Why wait? Get started with TaxBandits today and stay compliant with the IRS!