IRS Form 941 Instructions for 2026

If you are an employer, you need to fill out and file Form 941 for each quarter. To avoid major mistakes, learn the Form 941 instructions for 2026 and know how to fill out IRS Form 941.

Table of Content:

Complete Business Information

First, complete your basic details in

-

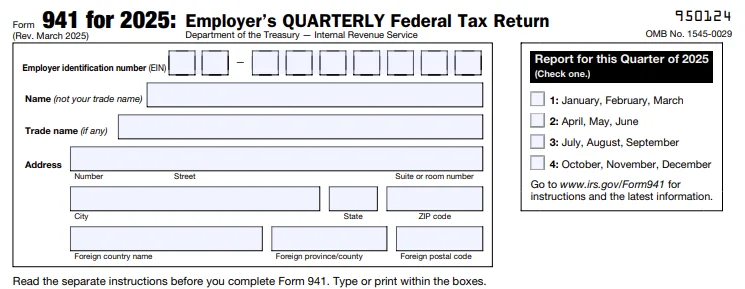

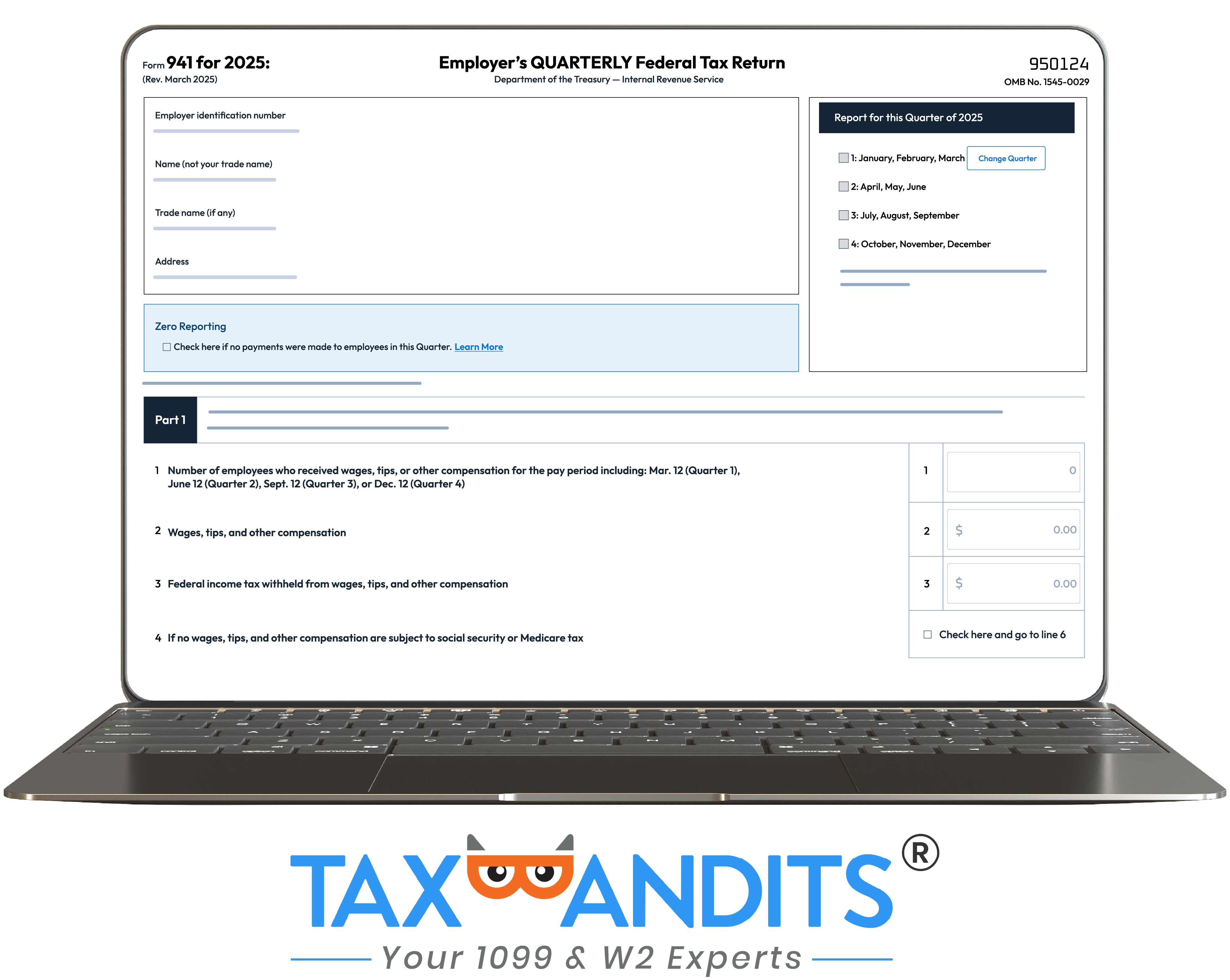

Box 1: Entering Employer Details

In box 1, enter the EIN, name, business name, and address.

-

Box 2: Choosing Quarter

In box 2, choose a quarter for which Form 941 is being filed.

For example, if you are filing the Form for the first quarter of the 2026 tax year, put an “X” in the box next to “January,

February, March.”

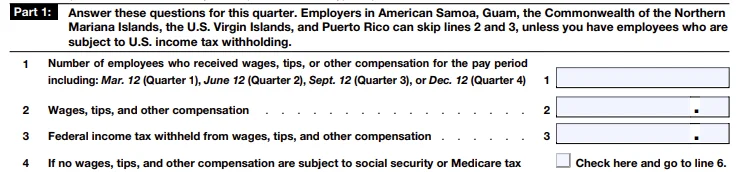

Part 1 - Questions for the quarter

Part 1 reports the Number of employees, their wages, and the federal income taxes withheld from their paychecks.

Part 1 consists of 15 lines where each line is explained in detail with the information that must be entered.

-

Line 1

Enter the number of employees, who got wages, tips, or other pay in the particular quarter

-

Line 2

Enter the complete wages, tips, paid and other pay to your employees

-

Line 3

Enter the federal income tax withheld from the employee’s paycheck

-

Line 4

Check this box if wages are not subject to social security and medicare tax. And if it doesn't apply, please skip this line

-

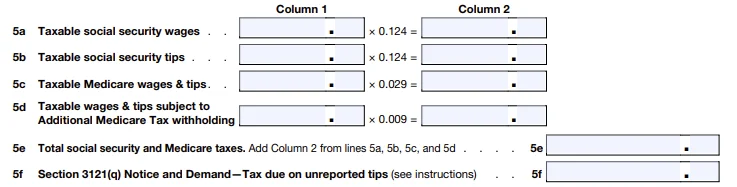

Line 5a : Taxable Social Security Wages

Line 5a = Column 1 x 0.124 = Column 2Enter the tax due that you have received from the Section 3121(q) Notice and Demand

-

Line 5b : Taxable social security tips

Enter the tips reported for all your employees during the quarter

Line 5b = Column 1 x 0.124 = Column 2 -

Line 5c : Taxable Medicare wages & tips

Enter the wages, tips, that are subject to medicare tax

Line 5c = Column 1 x 0.029 = Column 2 -

Line 5d : Taxable wages & tips subject to Additional Medicare Tax withholding

Enter all the taxable wages & tips subject to Additional Medicare Tax withholding

Line 5d = Column 1 x 0.009 = Column 2 -

Line 5e : Total social security and Medicare taxes

Sum of Column 2 from Lines 5a, 5a(i), 5a(ii), 5b, 5c and 5d.

Looking to Calculate Taxes to be reported on Form 941?

Use our Free Payroll Tax Calculator to compute Federal Income tax, Social Security, and Medicare taxes that is to be withheld from each employees paycheck.

-

Line 5f : Section 3121(q) Notice and Demand—Tax due on unreported tips

Enter the tax due that you have received from the Section 3121(q) Notice and Demand

The IRS issues Section 3121(q) Notice and Demand to employers advising them to report tips that their employees have failed to report. Employers aren’t liable for their share of social security and medicare taxes unless the employer receives this notice.

-

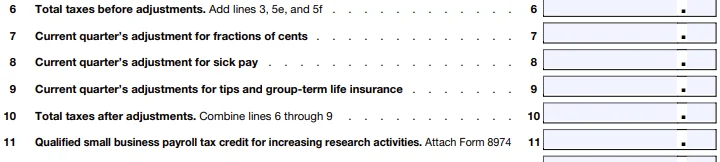

Line 6 : Total taxes before adjustments

Enter the sum of Line 3, 5e, and 5f

-

Line 7 to 9 : Tax Adjustments

Enter the Adjustment for a fraction of cents (Line 7), sick pay (Line 8), tips and group life insurance (Line 9)

-

Line 10 : Total taxes after adjustments

Enter the sum of line 6 to line 9

-

Line 11 : Qualified small business payroll tax credit for increasing research activities

Enter the amount calculated in Form 8974 and attach.

Form 8974 is used to determine the amount of credit that can be claimed for the increasing

research activities.

-

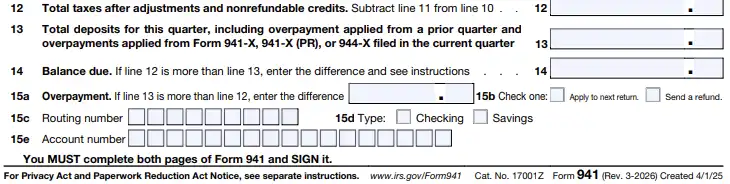

Line 12 : Total taxes after adjustments and nonrefundable credits

To get this amount, Subtract line 11 from line 10 as the amount on line 12 can’t be less than zero.

-

Line 13 : Total deposits for this quarter, including overpayment applied from a prior quarter and overpayments applied from Form 941-X, 941-X (PR), or 944-X filed in the current quarter.

-

Line 14 : Balance due

If the amount you entered in line 12 is more than the amount entered in line 13. Enter the difference and refer to the instructions below:

- You can make federal tax deposits for the amount shown on line 14 using EFW.

- If you are a monthly schedule depositor and making a payment for the amount shown on Line 14, you can pay by EFW, EFTPS, Credit or debit card, check, money order.

- File Form 941-V, if you prefer to pay the balance due using check or money order.

- If you were unable to pay the balance due in full you can apply for an installment agreement online. To apply using the Online Payment Agreement Application, please visit IRS.gov/OPA.

Note: TaxBandits supports EFTPS Payments, where you can pay your federal taxes in a easy and secure way.

-

Line 15 : Overpayment

Form 941 for 2026 now includes dedicated fields (Lines 15c–15e) to collect bank account information, allowing employers to receive refunds for overpayments via direct deposit.

-

Line 15a : Overpayment

If the amount on Line 13 is more than the amount on Line 12, enter the difference on Line 15a.

- Do not enter an amount on both Line 14 and Line 15a.

- Line 15a represents the total overpayment for the quarter.

-

Line 15b : Apply to Next Return or Request a Refund

If you overpaid your taxes for the quarter, you must choose how you want the overpayment handled.

You may:

- Apply the overpayment to your next Form 941 return, or

- Request a refund

Check only one box on Line 15b.

If you:

- Don’t check a box, or

- Check both boxes,

The IRS will generally apply the overpayment to your next return.

The IRS may apply your overpayment to any past-due tax balance under your EIN, regardless of your selection.

If the overpayment amount is less than $1, the IRS will refund or apply it only if you submit a written request.

If you select “Refund” but do not complete Lines 15c–15e (Direct Deposit section), your refund may be delayed.

Direct Deposit

To receive your refund via direct deposit, you must complete Lines 15c–15e.

Direct deposit provides faster refunds, increased security, and reduced paper processing.

-

Line 15c : Routing Number

Enter your bank’s 9-digit routing number.

-

The first two digits must be:

- 01 through 12, or

- 21 through 32

- Confirm with your financial institution that direct deposits are accepted.

You should verify your routing number if:

- The routing number on your deposit slip differs from your checks

- You are depositing into a savings account that does not allow check writing

- Your checks list a different financial institution

-

The first two digits must be:

-

Line 15d : Type of Account

Select the appropriate account type:

- Checking

- Savings

Check only one box. Selecting the wrong account type may cause your deposit to be rejected.

If unsure, confirm with your financial institution.

-

Line 15e : Account Number

Enter your bank account number where the refund should be deposited.

- Maximum: 17 characters

- May include numbers and letters

- Hyphens are allowed

- Do not include spaces or special symbols

- Leave unused boxes blank

If your refund deposit amount differs from what you expected, the IRS will mail an explanation within approximately two weeks after the deposit.

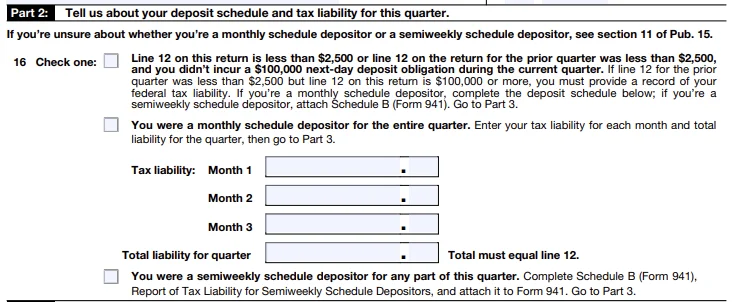

Form 941 Part 2 - Deposit schedule and tax liability for the quarter

Part 2 requires information about tax liability for the quarter, whether you are a semiweekly or monthly depositor.

-

Line 16

you have options to check any one of the boxes based on your tax liability.

Check box 1, If Line 12

- On your Form 941 was less than $2,500

- On your previous quarterly return was less than $2,500

- You didn’t incur a $100,000 next-day deposit obligation during the current quarter

Check box 2, If you were

- A monthly schedule depositor for the entire quarter, and enter your tax liability for each month of the quarter (Month 1, Month 2, and Month 3).

- Your total liability for the quarter must be equal to line 12 on your tax form 941.

Check box 3, If you were

- A semiweekly depositor during any part of the quarter.

- You must also enter the tax liability on Schedule B (Form 941), Report of Tax Liability for Semiweekly Schedule Depositors, and attach it along the Form 941 if you were a semiweekly depositor.

Form 941 Part 3 - About your business

The third portion of the 2026 IRS Form 941 collects information that will not be relevant to every business, for example, if the business is closing or is a seasonal employer. If the question does not apply to the business you are filing for, leave the field blank.

-

Line 17 : If your business has closed or you stopped paying wages

If your business was closed or you stopped paying wages in the quarter, check on line 17 and enter the final date when you paid wages.

-

Line 18 : If you are a seasonal employer and you don’t have to file a return for every quarter of

the yearIf you are a seasonal employer and don’t have to file Form 941 every quarter, then check the box under line 18.

If lines 17 and 18 don’t apply to your business, then just leave Part 3 blank and move on to Part 4.

Form 941 Part 4 - Third-party designee

Part 4 requires information about the third party designee that the employer authorizes to discuss with the IRS.

Check “Yes”, If you wish to discuss this return with the IRS and provide the designee name and phone number. Also, enter the 5 digit pin to use while talking with the IRS.

Check “No”, if you don’t wish to discuss.

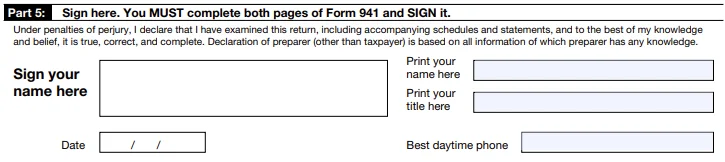

Form 941 Part 5 - Signature

Once each and every part is completed, you are required to sign Form 941.

The following persons are authorized to sign the return for each type of business entity.

- Sole proprietorship: Individual who owns the company

- Corporation or an LLC treated as a corporation: President, vice president, or other principal officer

- Partnership or an LLC treated as a partnership: Partner, member, or officer

- Single-member LLC: Owner of the LLC or a principal officer

- Trust or estate: The fiduciary

Paid Preparers Using Only Form 941 must be

- 941 Form must be signed by a duly authorized agent of the taxpayer if a valid power of attorney has been filed.

-

If the form is prepared by the paid preparer, enter their information such as name, signature, address, PTIN, and

contact number.

- A paid preparer is someone who completes your Form 941 filing and is responsible for preparing payroll tax forms on

your behalf. - If your Form 941 is filed by a paid preparer, they have to enter their information on part 5.

E-file your Form 941 with TaxBandits

TaxBandits provides you with a smart and reliable solution to e-file your Form 941 with ease and confidence. Our software guides you through every step of the filing process with simple and proper instructions for your convenience, allowing you to complete your 941 form process in a few minutes!.

Sign up today – File your 941 easily!

Let us take the stress out of filing Form 941

Trusted by small business owners and tax professionals alike, TaxBandits makes Form 941 filing simple with our easy-to-use software.

Experience accurate, stress-free filing today.

Advantages of Filing Form 941 with TaxBandits

- Simplified Zero Reporting

- Copy Prior Quarter Data

- Option to Pay Balance Due

- Instant IRS Status Updates

- Support Prior Year Filing

- Flexible Bulk Upload

Download Free

Form 941 Guide

Get your guide and file accurately and on time—with confidence.

- Step-by-step line instructions

- IRS tips & deadlines

- Avoid common filing errors

Other Suggestions

Related Topics

IRS Form 941

- Form 941

- Form 941 Instructions

- Form 941 Due Dates

- Form 941 Mailing Address

- Form 941 Schedule B

- Form 941 Penalty

- Form 941 ERC

- Form 940 vs 941

- Form 941 vs 944

Revised Form 941 for 2023

Form 941 Worksheets

- Form 941 Worksheet 4 for Q3 & Q4 2021

- Form 941 Worksheet 2 for Q2 2021

- Form 941 Worksheet 1

- Form 941 Worksheets

IRS Form 941-X

Revised Form 941 for 2022

Revised Form 941 for 2021

- IRS Form 941 for Q4 2021

- Revised Form 941 for 2nd Quarter, 2021

- Form 941 Quarter 2 vs Quarter 1, 2021

- Revised Form 941 Schedule R for Q2 2021

- Revised Form 941 for 1st Quarter, 2021

Revised Form 941 for 2020

- Revised Form 941 for 2nd Quarter

- Revised Form 941 for 3rd & 4th Quarters

- Revised Form 941 Schedule R

- Revised Form 941-X