Penalties for Form 990/990-EZ/990-PF

If an organization fails to file their return after its due date without providing reasonable cause, the following penalties will be enforced:

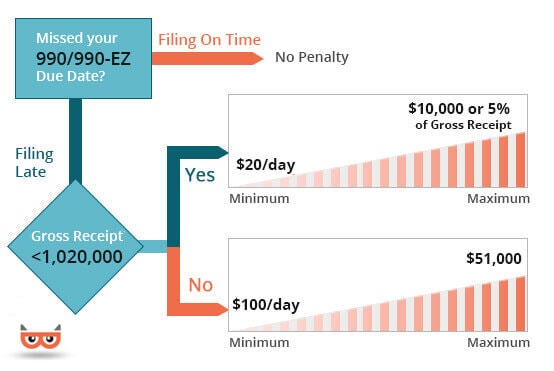

Organizations with gross receipts less than $1,020,000 for its tax year will have a penalty of $20/day for each day that the return is late. The maximum penalty for these organizations is $10,000 or 5 percent of the organization's gross receipts, whichever is less.

Organizations with gross receipts more than $1,020,000 for its tax year will have a penalty of $100/day for up to a maximum of $51,000.

Penalties Against Responsible Person(s):

Organizations which fail to file a completed return or provide proper information will be offered a fixed amount of time to fulfill the necessary filing requirements and will be notified of this time period through written correspondence from the IRS. If no action has been taken after this time period expires, the person responsible for complying will be charged a penalty of $10/day, with a per capita of $5,000 for any one return.

Form 990/990-EZ Penalties

Other penalties such as fines and imprisonment are suitable for willfully not filing returns or filing fraudulent returns and statements with the IRS (See sections 7203, 7206, and 7207).

- Exempt organizations required to file electronically must do so. If not, they are considered to have failed to file their return. A paper return for these organizations can only be used to report a name change to the organization.

- Failure to complete required line items or a required part of a Schedule will result in the return being incomplete with a penalty charged.

- An organization will be responsible for filing a complete and accurate return even if a paid preparer fails to do so.

- Due to states requiring separate filings, failure to meet these requirements can lead to additional penalties.

Other Penalties for Form 990-PF:

Form 990-PF also satisfies filing requirements of tax returns under Section 6011 for tax on investment income imposed by Section 4940 (Section 4948 for Exempt Foreign Organizations). Penalties imposed by Section 6651 for not filing a return without reasonable cause will apply. Willingly failing to file and filing fraudulent returns and statements would result in criminal penalties (see Sections 7203, 7206, and 7207).

Late Payment of Tax:

Organizations that do not pay taxes when due are charged a penalty of 1/2 of 1% of the unpaid tax for each month or a part of the month that the tax is not paid for a maximum of 25% of the unpaid tax (Section 6651). However, this penalty can be waived if the organization provides a reasonable cause why the tax was not paid on time to the IRS and it is accepted. Lastly, interest will be charged on any tax not paid on time at the rate provided by Section 6621.

Failure to Pay Estimated Tax:

Penalties will apply for failing to pay estimated tax on net investment income of domestic private foundations (Section 6655 & Section 4947(a)(1) in the case of nonexempt charitable trusts. This penalty will be extended to any tax on the unrelated business income of the private foundation.

Failure to Pay Employment Tax:

The same penalties that are listed in Section 6656 apply for failure to deposit employment taxes when they are due. Also see sections 11 and 12 of Pub. 15 (Circular E), Employer's Tax Guide, for details.

Note: Typically, a private foundation is subject to penalty if it fails to pay its tax liability of $500 or more in time. Further details on this penalty can be found on Form 2220, Underpayment of Estimated Tax by Corporations, in General, Instruction D.

Success Starts with TaxBandits

An IRS Authorized E-file Provider You can Trust

Create a Free Account