Form 1042-S Exemption Codes for 2025

Understanding Form 1042-S Exemption Codes

Updated on November 24, 2025 - 10:30 AM by Admin, TaxBandits

Form 1042-S is a crucial document for businesses involved in cross-border transactions, reporting income paid to foreign persons and entities. This article will explore Box-3a & 4a of Form 1042-S, explicitly focusing on the Exemption Codes. Understanding these elements is essential for businesses to accurately report payments to foreign payees and ensure compliance with tax regulations.

Table of Content:

- Form 1042-S- An Overview

- Form 1042-S Box 3- Chapter Indicator

- Boxes 3a and 4a- Chapter 3 and Chapter 4 Exemption Codes

- Box 3a exemption codes

- Box 4a exemption codes.

- Simplify your 1042-S filing with TaxBandits!

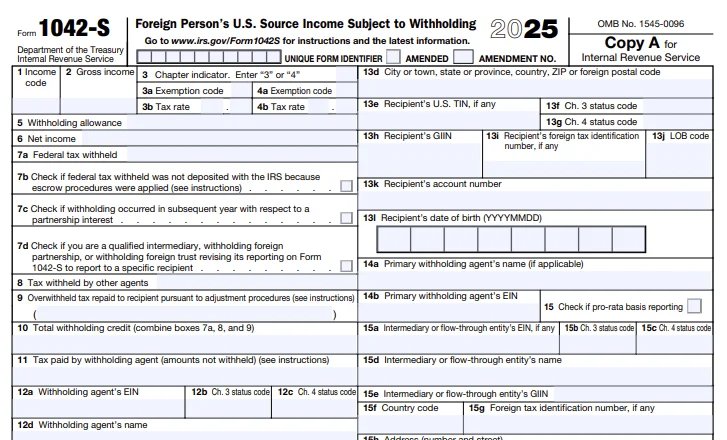

1. Form 1042-S- An Overview

Form 1042-S is a tool that helps the U.S. government keep track of payments made to people or groups from outside the country. It’s not just about reporting the income; it’s about ensuring everyone pays the right amount of taxes. Those in charge of withholding tax, like employers or universities, use this form to report various types of income, such as dividends or scholarships, even if they didn’t withhold any taxes.

Here’s what you report in box 3 of Form 1042-S:

- Box 3 - Chapter Indicator. Enter either “3” or “4”

- Box 3a, 4a - Exemption Code

2. Form 1042-S Box 3- Chapter Indicator

Box 3 of Form 1042-S specifies the Chapter Indicator.

This box indicates whether the withholding falls under Chapter 3 or 4, specifying whether the amounts being withheld are reported under the corresponding sections of the Internal Revenue Code (IRC).

Typically, Chapter 3 represents the withholding that applies to Foreign persons, and Chapter 4 represents the withholding that applies to entities that are foreign financial institutions.

You must enter either ‘3’ or ‘4’ in box 3 of Form 1042-S (not both chapters). If you didn't withhold taxes under Chapter 3 or 4 and are not reporting amounts in Boxes 7 through 9, enter '3.' For payments to U.S. payees, enter '3' and leave Boxes 3a and 3b blank.

3. Boxes 3a and 4a- Chapter 3 and Chapter 4 Exemption Codes

The Exemption Code on Form 1042-S indicates why the recipient of the income is exempt from U.S. taxation. This applies if the tax rate entered in box 3b or 4b is “00.00”.

If the amounts were withheld under Chapter 3, you must adhere to the following conditions:

- In Box 4b, if the tax rate exceeds 0 and is not subject to withholding, enter “00” in Box 4a.

- In Box 4b, if the tax rate entered is “00.00”, you must input the right exemption codes (13 through 21) in Box 4a.

If the amounts were withheld under Chapter 3, you must follow the following conditions:

- In Box 3b, if the tax rate entered is greater than 0 and is not subject to withholding, enter “00” in Box 3a.

- In Box 3b, if the tax rate is subject to backup withholding, then leave Box 3a blank.

If exemption codes 01 or 14 correspond to (effectively connected income), you must enter the recipient's U.S. TIN in box 13e if the income you reported corresponds to a U.S. trade or business. Suppose you don't know the recipient's U.S. TIN, or it's unavailable, you must withhold tax at a rate of 30.00% (30.00) and enter "00" in both boxes 3a and 4a.

Need an easier way to file 1042-S?

Get Started Today with TaxBandits and file Form 1042-S in a few simple steps. You will get instant notification from the IRS about the filing status and deliver recipient copies via Foreign Postal mail or Online access. E-File Now

4. Box 3a exemption codes

The Valid Exemption codes and their definitions are as follows:

| Code | Box 3a exemption codes | Explanation of codes |

|---|---|---|

| 01 | Effectively connected income | If exemption code 01 corresponds to (effectively connected income), you must enter the recipient's U.S. TIN in box 13e if the income you reported corresponds to a U.S. trade or business. |

| 02 | Exempt under IRC | This exemption code can be used if none of the other Chapter 3 exemption codes are applicable. |

| 03 |

Income is not from U.S. sources |

You can use this exemption code if the income is not reported from U.S. sources. |

| 04 | Exempt under tax treaty | You can use this code if you are exempt under Tax treaty condition |

| 05 | Portfolio interest exempt under IRC | You can use this code if the portfolio interest is exempted under IRC |

| 06 | QI that assumes primary withholding responsibility | You can use this exemption code when making a payment to a QI (Qualified Intermediary) that has been stated on Form W-8IMY that it is taking on the main responsibility for withholding under chapters 3 and 4. |

| 07 | WFP(withholding foreign partnership) or WFT (withholding foreign trust) | You can use this exemption code only if you pay to a foreign partnership or trust that has been represented on its Form W-8IMY( Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S. Branches for United States Tax Withholding ) |

| 08 |

U.S. branch treated as U.S. Person |

For Chapter 3 purposes, this exemption code is used when making a payment to a U.S. branch or a territory FI that has been stated on its Form W-8IMY that it agrees to be treated as a U.S. person. |

| 10 |

QI represents that income is exempt |

You can use this code for chapter 3 purposes when paying a QI that hasn't taken on the main responsibility for withholding under chapters 3 and 4 or primary backup withholding responsibility. This applies if the QI has stated on a withholding statement associated with its Form W-8IMY that the income is exempt. |

| 11 | QSL that assumes primary withholding responsibility | For chapter 3, use exemption code 11 when you're making a substitute dividend payment to a financial institution (like a QI) that has stated on its Form W-8IMY that it's acting as a QSL for the linked account. |

| 12 | Payee subjected to Chapter 4 withholding | You can use this exemption code for Chapter 3 purposes if the recipient has been withheld under Chapter 4; thus, Chapter 3 withholding does not apply. When reporting a payment subject to Chapter 4 withholding, ensure that 30% of the tax is withheld, remitted to the IRS, and correctly reported on Form 1042-S. |

| 22 | QDD that assumes primary withholding responsibility | You can use this exemption code if the payment is made to a QI (Qualified Intermediary) acting as a QDD (Qualified derivatives dealers), who is assumed to be the primary withholding agent. |

| 23 | Exempt under section 897(l) | You can use this exemption code for distributions made by a QIE to a qualified foreign pension fund (or an entity, all of the interests of which are held by a qualified foreign pension fund) that are exempt under section 897(l). |

| 24 | Exempt under section 892 | You can use this exemption code for income paid to a foreign government or an international organization exempted under section 892. |

5. Box 4a exemption codes.

The Valid Exemption codes and the definition are as follows:

| Code | Box 4a exemption codes | Explanation of Codes |

|---|---|---|

| 13 | Grandfathered payment | You can use exemption code 13 for Chapter 4 purposes only when paying under a grandfathered obligation. |

| 14 | Effectively connected income | If exemption code 14 corresponds to (effectively connected income), you must enter the recipient's U.S. TIN in box 13e if your reported income corresponds to a U.S. trade or business. |

| 15 | Payee not subject to Chapter 4 withholding |

For Chapter 4 purposes, you can use exemption code 15 if the payment is withholdable but has not been withheld due to the payee's Chapter 4 status. Also, if you apply for a 90-day grace period for the withholdable payment, you can use this same code.

Struggling with Filing Form 1042-S?

Selecting the wrong exemption code could lead to IRS penalties! Avoid costly mistakes—TaxBandits makes e-filing simple, accurate, and stress-free. |

| 16 | Excluded nonfinancial payment | Exemption code 16 is utilized for Chapter 4 payments as defined in Regulations Section 1.1473-1(a)(4)(iii). If exemption code 16 is the only one that applies, then use it; if not, use the other exemption code that applies |

| 17 | Foreign Entity that assumes primary withholding responsibility | You can use this exemption code 17 for Chapter 4 only when paying a QI that assumes primary withholding responsibility (WP or WT). |

| 18 | U.S. Payees—of participating FFI or registered deemed-compliant FFI | Exemption code 18 is exclusively utilized in Chapter 4 when paying a participating FFI or registered deemed-compliant FFI (Foreign financial institutions). |

| 19 | Exempt from withholding under IGA | You can use this code when exempt from withholdingunder under Inter-governmental agreement (IGA) |

| 20 | Dormant account | Exemption code 20 can be used for Chapter 4 if the withholding statement attached to the Form W-8IMY of a participating FFI or registered deemed-compliant FFI states that the payment is allocable to a dormant account holder and that the escrow procedure of Regulations section 1.1471-4(b)(6) is applicable. |

| 21 | Other—payment not subject to Chapter 4 withholding | Use exemption code 21 for Chapter 4 purposes if the payment is exempt from Chapter 4 withholding and no other Chapter 4 exemption code applies. Income code 37 (return of capital) also uses this code to report non-dividend payments. |

Learn More about the Form 1042-S Instructions in detail here.

6. Simplify your 1042-S filing with TaxBandits!

TaxBandits, an authorized e-file provider, offers a secure solution for tax professionals and businesses of all sizes to e-file 1042-S. Our user-friendly software simplifies the process, allowing you to maintain compliance in just a few steps:

To complete and e-file 1042-S using TaxBandits, follow the following instructions.

- Step 1: Create an account and choose Form 1042-S.

- Step 2: Enter Information on the 1042-S Form.

- Step 3: Review and send the IRS Form 1042-S.

- Step 4: Distribute recipient copies through postal mail(foreign) or online access services.

Get Started with TaxBandits to E-File your 1042-S Online in minutes!

Success Starts With TaxBandits

An IRS Authorized E-file Provider You can Trust