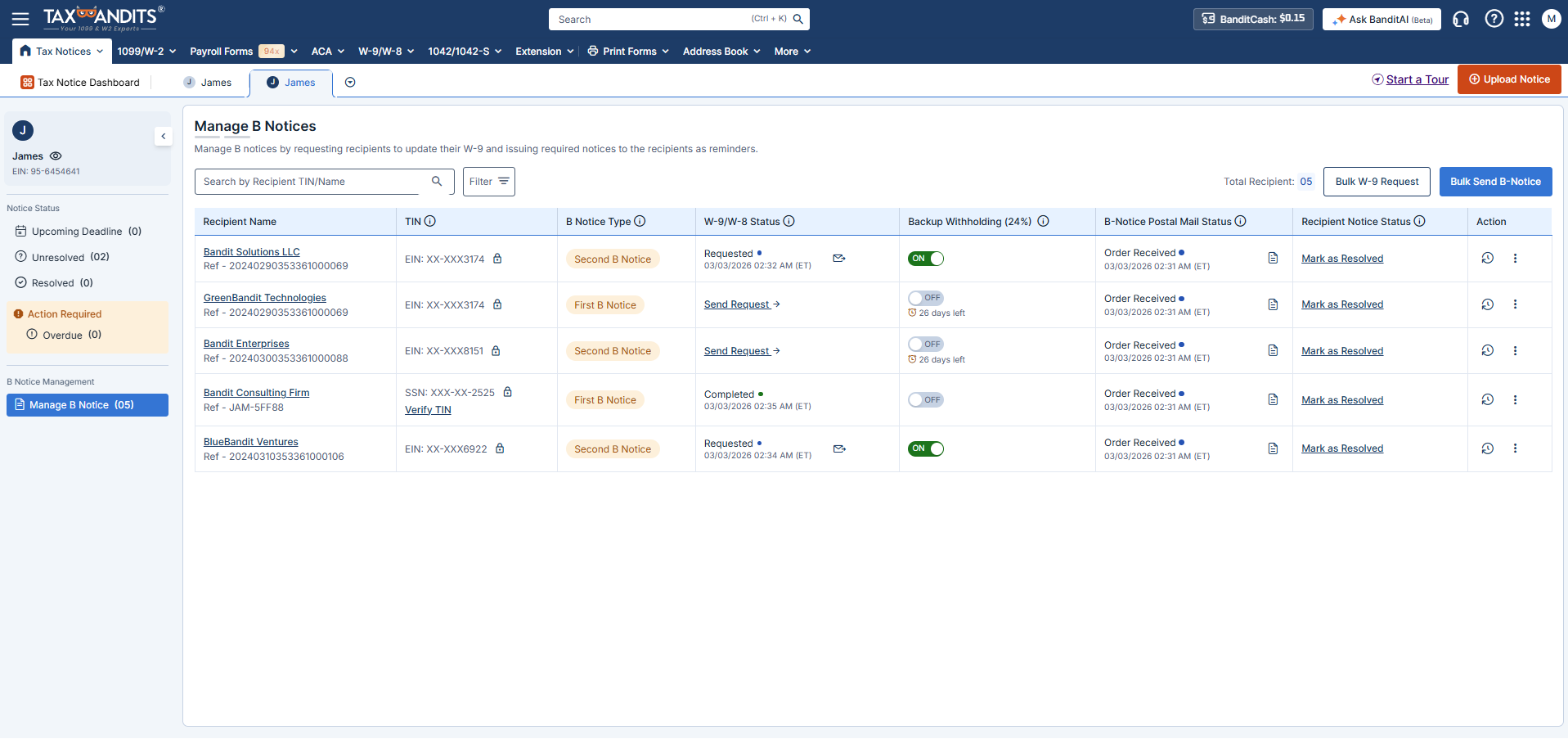

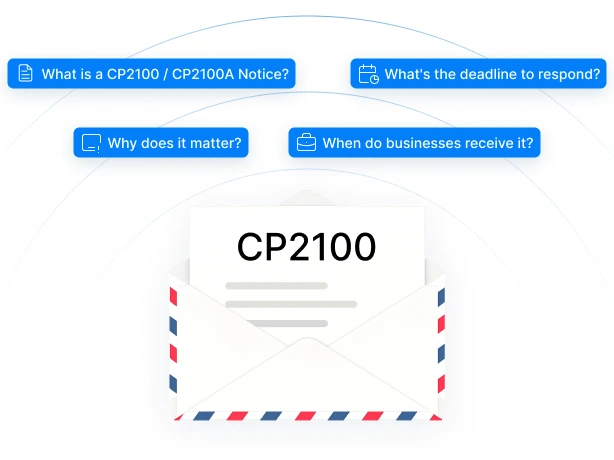

Received a CP2100 or CP2100A Notice from the IRS?

TaxBandits walks you through every step — from collecting W-9s and verifying TINs to

sending B-Notices and staying fully compliant. One platform, full compliance.

Trusted by 1M+ Businesses

IRS-Authorized

SOC 2 Compliant

World-Class Support

Understanding CP2100 / CP2100A

-

What is a CP2100 / CP2100A Notice?

The IRS sends this notice when the payee (recipient) name and TIN on your 1099 filings don't match IRS records — flagging vendors, contractors, or others you've paid and reported.

-

When do businesses receive it?

Typically 3 to 4 months after filing 1099s, once the IRS cross-checks your submissions against their records.

-

What's the deadline to respond?

You have 15 business days to send B-Notices to flagged payees. If they don't respond, backup withholding — 24% of future payments — must begin within 30 business days.

-

Why does it matter?

Ignoring this notice can trigger IRS penalties and ongoing withholding obligations that get harder to unwind over time.

Act within the IRS deadline

from the IRS

flagged payees

if no response

or Form 945

Missing either deadline increases your IRS liability. TaxBandits keeps you on track at every stage.

How TaxBandits Helps You Resolve CP2100 / CP2100A

Everything you need to go from notice to resolution — without switching tools.

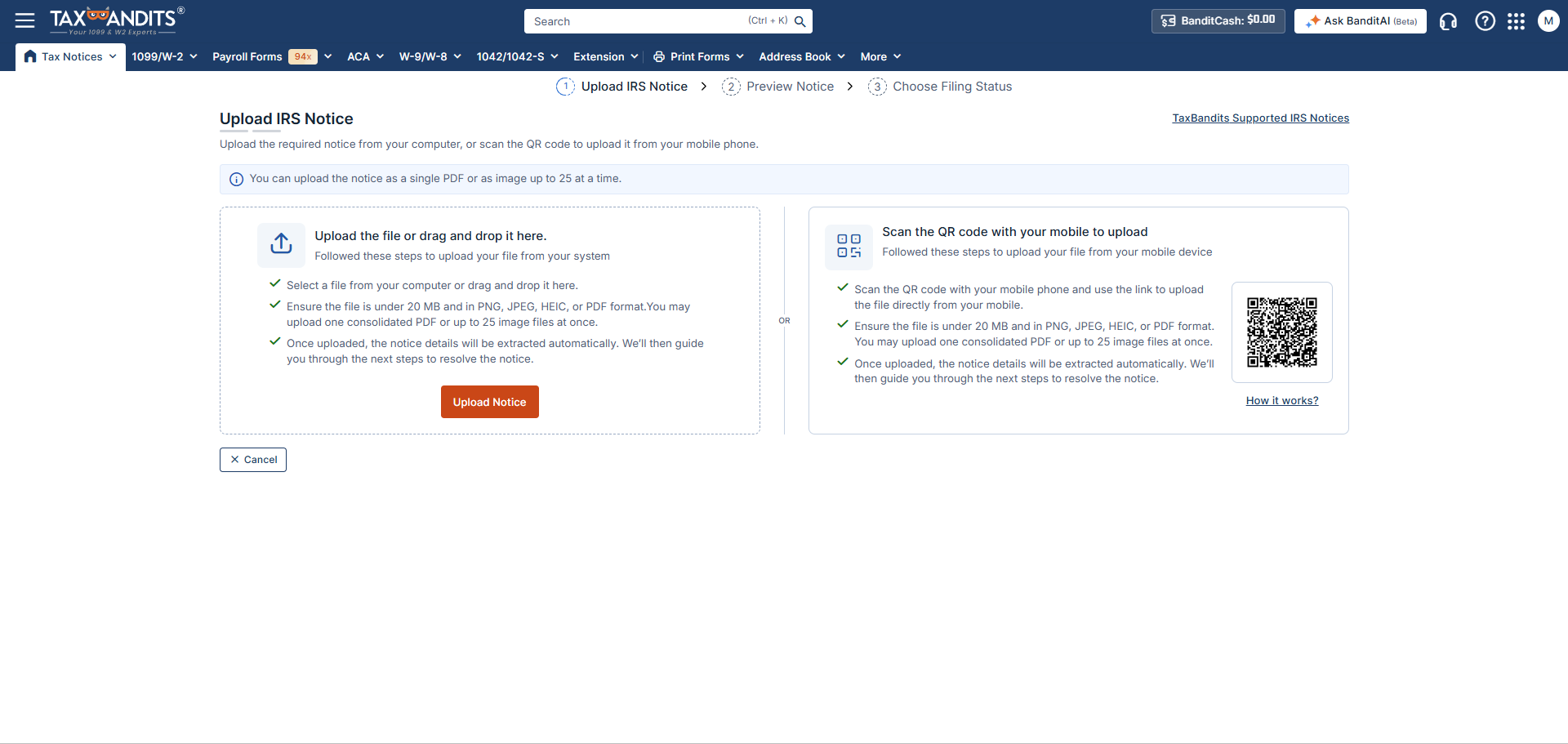

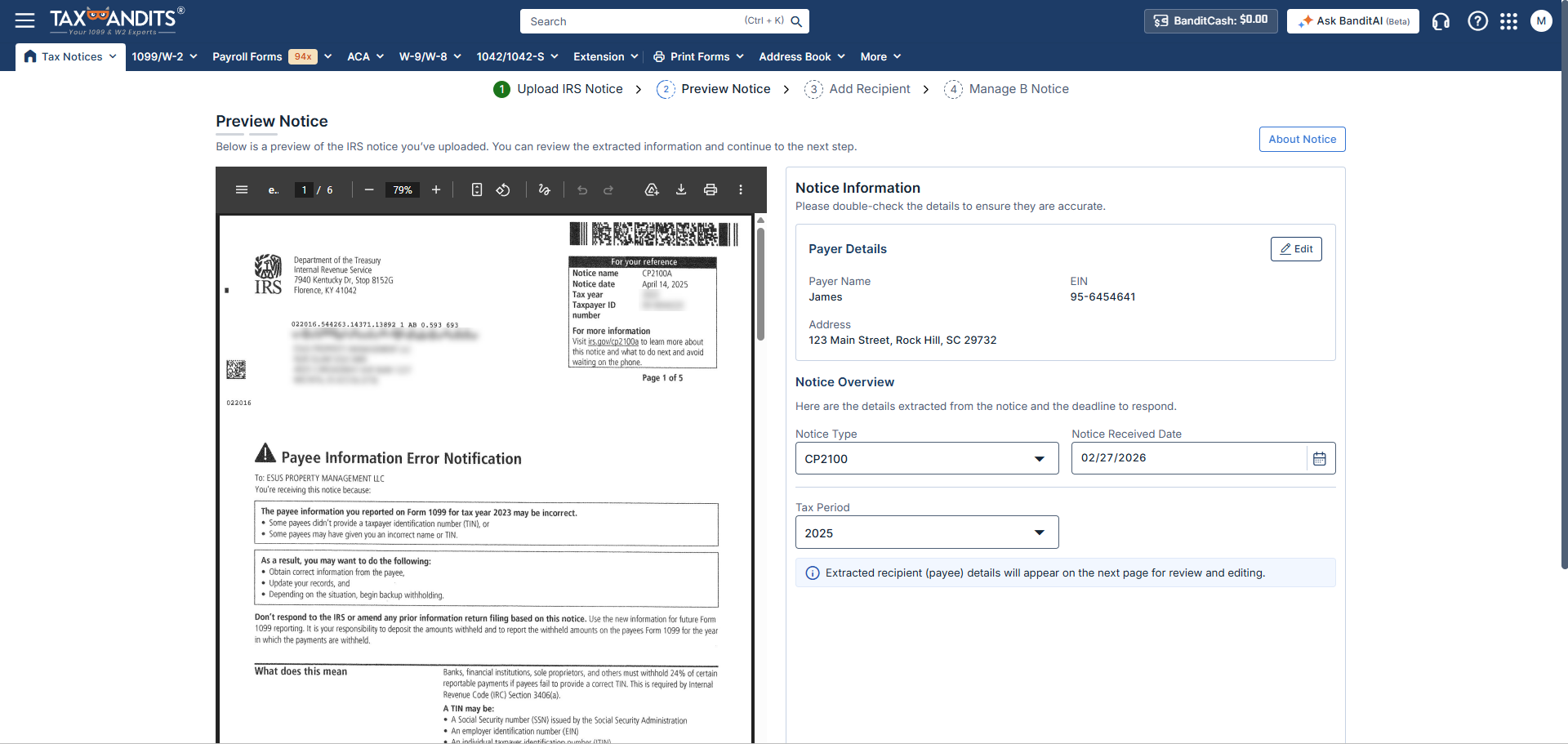

Upload & Extract

Upload your CP2100 or CP2100A notice. TaxBandits automatically identifies the payees with mismatched or missing TINs — no manual data entry, no spreadsheets.

- Auto-extraction

- No manual entry

- Instant identification

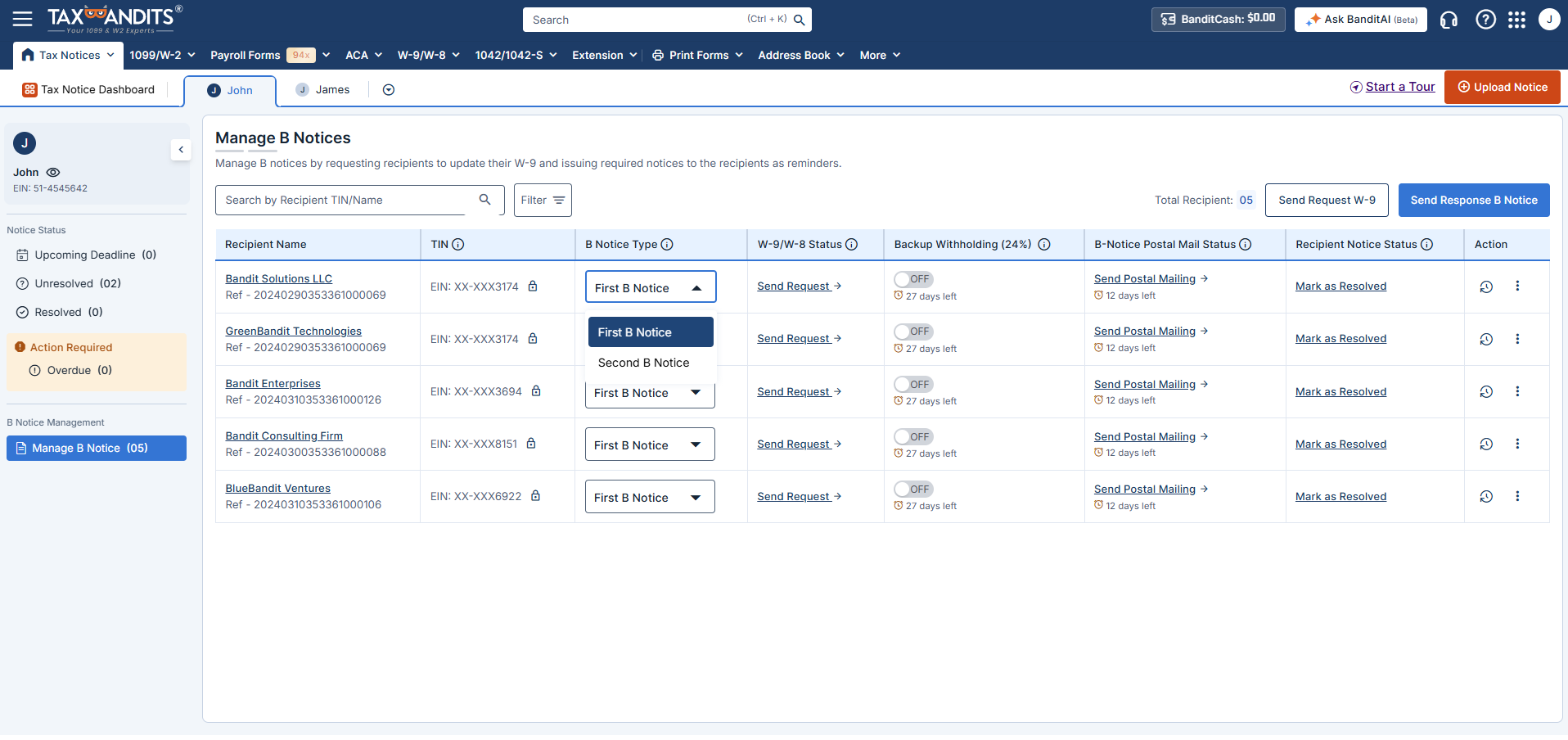

Collect W-9s & Verify TINs

Send digital W-9 requests to flagged payees and track responses in real time. Once submitted, TaxBandits runs TIN matching against IRS records — so you know the data is accurate before you file anything.

- Digital W-9 requests

- Real-time tracking

- IRS TIN matching

B-Notice Mailing & Withholding Tracking

Payees who don't respond trigger a B-Notice obligation. TaxBandits prints and mails first and second B-Notices on your behalf — IRS-compliant and on time. A small postal fee applies. Track every payee's withholding status — active, pending, or resolved — from one dashboard.

- 1st & 2nd B-Notices

- IRS-compliant mailing

- Withholding dashboard

File 1099 Corrections or Form 945

Every resolution path ends here. If the payee provided a valid TIN, file corrected 1099s directly from TaxBandits. If backup withholding was applied, e-file Form 945 to report withheld amounts to the IRS. Either way, you're covered.

- 1099 corrections

- Form 945 e-filing

- Direct IRS submission

Pay only when you mail B Notices to recipients

No hidden fees, no surprise costs.

What’s Included

- Mailing of B Notices to recipients (First & Second)

- Real-time status tracking

$4.99/Notice

Frequently Asked Questions

Common questions about CP2100 notices and how TaxBandits handles them.

What is the difference between CP2100 and CP2100A?

CP2100 is issued when there are 50 or more payee TIN errors. CP2100A is issued for fewer than 50. The compliance obligations are identical for both.

Do I need to send a B-Notice if the payee is no longer active?

Yes. The B-Notice obligation is tied to the filing, not the current status of the relationship. If the payee was reported on a 1099 with a mismatched TIN, you're still required to send the notice.

What's the difference between a first and second B-Notice?

A first B-Notice informs the payee of a TIN mismatch and requests a corrected W-9. A second B-Notice — triggered by a second mismatch within 3 years — requires the payee to obtain TIN validation directly from the IRS or Social Security Administration.

How long do I need to apply backup withholding?

Backup withholding continues until the payee provides a valid TIN or certifies their TIN is correct. There is no automatic expiration.

What happens if I miss the 15-day B-Notice deadline?

You remain liable for any backup withholding you were required to collect but didn't. The IRS can assess penalties under IRC §3406 for failure to withhold.

Can B-Notices be sent electronically?

The IRS requires B-Notices to be mailed to the payee's last known address. TaxBandits handles the printing and mailing on your behalf,

ensuring IRS-compliant delivery.

What type of payments are subject to backup withholding?

Backup withholding may apply to the following reportable payments when a valid TIN is not provided or is incorrect:

- Nonemployee compensation (Form 1099-NEC)

- Rents, royalties, commissions, attorney payments, and other miscellaneous income (Form 1099-MISC)

- Interest income (Form 1099-INT)

- Dividends (Form 1099-DIV)

- Patronage dividends (Form 1099-PATR)

- Original issue discount paid in cash (Form 1099-OID)

- Broker and barter exchange proceeds (Form 1099-B)

- Certain gambling winnings (Form W-2G), if not subject to regular gambling withholding

- Payment card and third-party network transactions (Form 1099-K)

- Certain taxable government payments, including grants and agricultural payments (Form 1099-G)

Can I file 1099 corrections and Form 945 through TaxBandits?

Yes. Both are supported directly within TaxBandits — no separate tools or platforms needed.

Ready to resolve your CP2100 notice?

Upload your notice and let TaxBandits guide you — W-9 collection, TIN matching,

B-Notice mailing, and 1099 corrections. All in one place.