Form 1098-Q: What you need to know

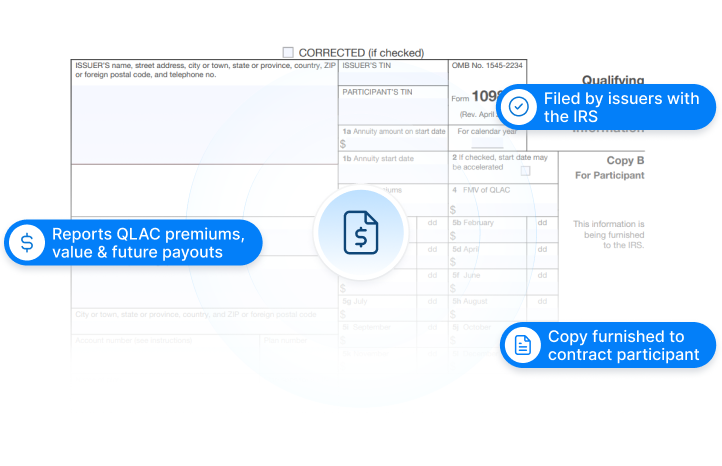

Form 1098-Q is an IRS information return used to report details of a Qualified Longevity Annuity Contract (QLAC), including total premiums paid, fair market value, and future annuity payment information.

Issuers are required to file Form 1098-Q with the IRS and furnish a copy to the contract participant.

Who is required to file Form 1098-Q?

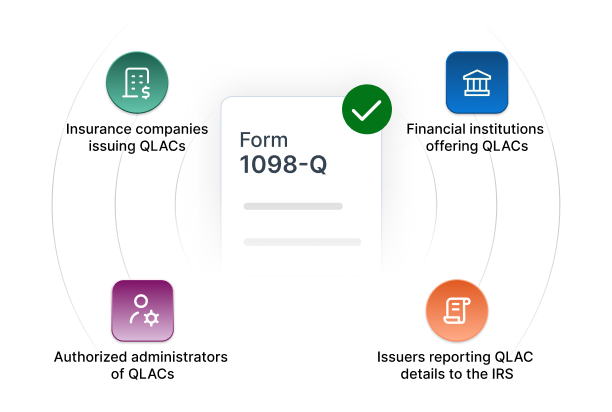

Form 1098-Q must be filed by the issuer of a Qualified Longevity Annuity Contract (QLAC) to report contract details to the IRS. This includes:

- Insurance companies issuing QLACs

- Financial institutions offering annuity contracts that meet QLAC requirements

- Authorized entities responsible for administering and reporting the contract on behalf of the issuer

Deadline to File Form 1098-Q with the IRS

Meet your IRS filing and distribution deadlines to avoid penalties and stay compliant.

| Recipient Copy Distribution | Paper Filing with IRS | Electronic Filing with IRS |

|---|---|---|

| February 02, 2026 | March 02, 2026 | March 31, 2026 |

Information Required to File Form 1098-Q

Discover the key information needed to file Form 1098-Q accurately and efficiently.

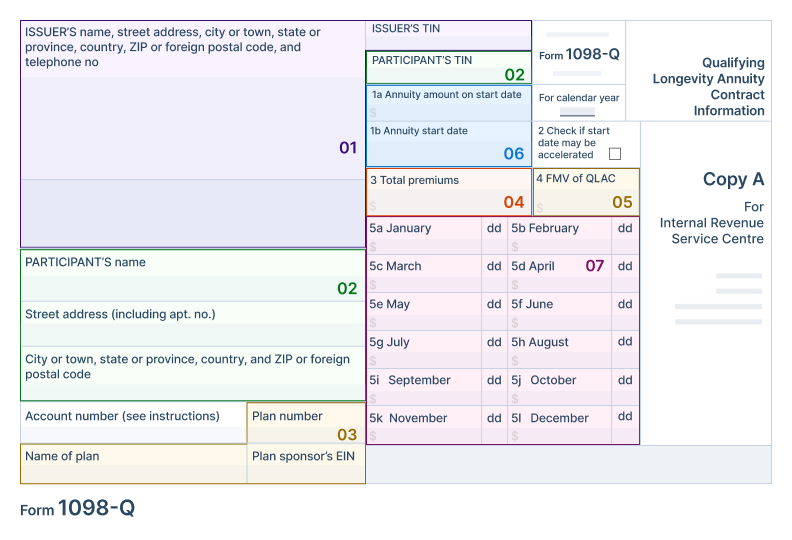

Issuer Information

Name, address, and TIN of the annuity issuer responsible for the QLAC.

Participant Information

Participant's name, address, and TIN (individual who owns the QLAC).

Plan Information (if applicable)

Plan name, plan number, and Employer Identification Number (EIN) if the QLAC is held under a qualified retirement plan.

Total Premiums Paid

Cumulative amount of all premiums contributed to the QLAC through the end of the calendar year.

Fair Market Value (FMV)

Year-end value of the QLAC contract, reported for compliance and tracking purposes.

Annuity Details

- Scheduled annuity start date

- Future periodic payment amount

- Indicate if the start date may be accelerated

Premium Payment Details

- Payment amount per contribution

- Date of each premium payment

The Bandit Commitment

Your Form 1098-Q filing, backed by accuracy and accountability.

Filing Form 1098-Q requires more than submitting data—it demands precise QLAC reporting, structured validation, and a workflow built for compliance.

TaxBandits supports every step of the process, from initial data entry to IRS acceptance and recipient copy distribution.

Getting the right

data in

Every Form 1098-Q starts with validated, structured data—ensuring accurate reporting of premiums, fair market value, and annuity details from the very first step.

Guided, end-to-end compliance

From capturing QLAC contract details to transmitting filings and furnishing participant copies, TaxBandits manages the entire process to keep your reporting complete and compliant.

No-cost corrections & retransmissions

If corrections or retransmissions are needed, they are covered under your existing filing fee—no additional charges, no surprises.

Money-back guarantee

If the IRS rejects your form or identifies it as a duplicate filing, your filing fee may be refunded—because unsuccessful filings should not result in added cost.

How to File Form 1098-Q with TaxBandits

From IRS filing to recipient copies, TaxBandits handles the entire process seamlessly.

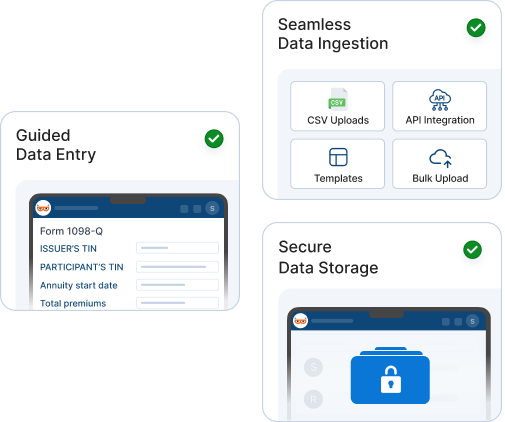

Prepare forms with ease

QLAC contract data is detailed. TaxBandits gives you a structured, error-resistant way to get it in.

-

Guided Data Entry:

Step-by-step workflow walks you through each field on the form so nothing gets missed.

-

Flexible Data Import:

Bring in issuer and participant data via CSV templates, bulk uploads or integrations to simplify high-volume filings.

-

Secure Data Storage:

All filing data is securely stored for easy access, status tracking, and future reference.

Ensure accuracy with validations

Our system performs checks at every stage of your Form 1098-Q filing to identify and resolve errors before submission.

-

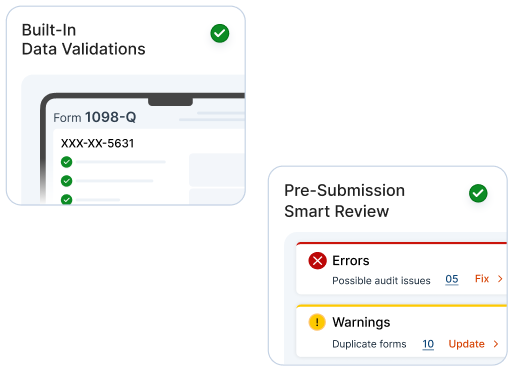

Built-In Data Validations:

Automatically detect missing TINs, incorrect premium amounts, invalid dates, and data inconsistencies before they cause delays.

-

Pre-Submission Smart Review:

Review flagged alerts and resolve issues in advance to ensure accurate filings and stronger acceptance rates.

Secure IRS e-filing and recipient copy distribution

Submit your Form 1098-Q securely and furnish participant copies, all within a single, streamlined workflow.

-

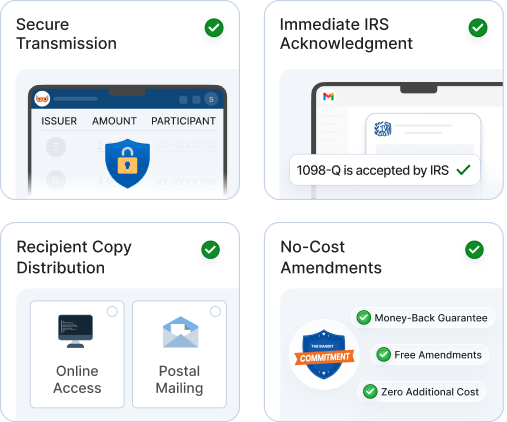

Immediate IRS Acknowledgment:

Receive instant IRS acknowledgment, typically within 24 hours of submission.

-

Secure Transmission:

Enterprise-grade encryption handles every submission—no paperwork, no manual handoffs.

-

Recipient Copy Distribution:

Furnish participant copies via postal mail, secure online access, or both to meet your compliance needs.

-

No-Cost Amendments:

File corrections and retransmissions anytime at no additional cost, backed by the Bandit Commitment.

FAQs

Frequently Asked Questions about Form 1098-Q

A QLAC is a deferred annuity purchased within a qualified retirement plan that provides guaranteed income at a later age, typically no later than age 85. It is designed to help manage longevity risk and may offer relief from Required Minimum Distribution (RMD) calculations.

Failing to file Form 1098-Q on time can result in IRS penalties. Late filing penalties range from $60 to $340 per form, depending on how late the submission is. If the IRS determines intentional disregard, the penalty increases to $680 per form with no maximum limit. Learn more about 1099 penalties.

Premiums paid toward a QLAC must not exceed the limit set by the IRS.

- For the 2025 tax year, the maximum premium limit is $200,000, applied to the total amount invested across all QLAC contracts owned by an individual.

- This limit is adjusted annually for inflation, with increases rounded down to the nearest $10,000.

- Issuers must verify that total premiums do not exceed the applicable IRS threshold for the given year.

Yes! A QLAC can be funded using eligible retirement accounts such as IRAs or employer-sponsored plans. However, total premiums across all QLACs must not exceed the IRS limitation amount.

A QLAC can be structured to continue providing value after the participant passes. Depending on the contract terms, beneficiaries may receive a return of premiums paid, or a surviving spouse may receive ongoing annuity payments.

However, these provisions must be set up correctly within the contract—any arrangement that falls outside IRS rules risks disqualifying the contract's QLAC status entirely, triggering immediate RMD exposure on the full account value.

Success Starts With TaxBandits

An IRS Authorized E-file Provider You Can Trust!