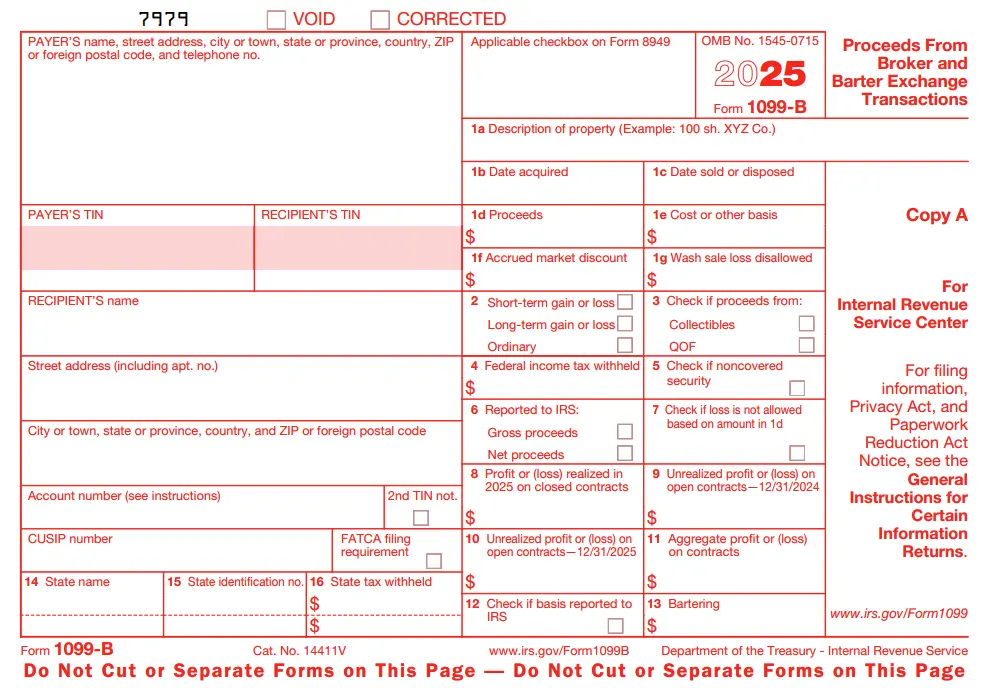

IRS Form 1099-B for 2025: Proceeds From Broker and Barter

Exchange Transactions

Charles Hardy | Last Updated: November 17, 2025

The IRS mandates e-filing when you file 10 or more tax returns for the 2025 tax year. E-file Now

Quick Overview of Form 1099-B for 2026:

- Form 1099-B: Proceeds From Broker and Barter Exchange Transactions

- What’s reported on Form 1099-B: Proceeds from the sale of stocks, bonds, and other securities.

- Who needs to file: Broker or Barter exchange

- Filing Frequency: Annual

-

When it is due:

- Electronic Filing: March 31, 2026

- Recipient Copy: February 2, 2026

- Paper Filing: March 2, 2026

TaxBandits simplifies your 1099-B filing. See how!

What is IRS Form 1099-B?

Form 1099-B, Proceeds from Broker and Barter Exchange Transactions is an IRS tax form used to report the sale of stocks, bonds, mutual funds, and other securities through a brokerage account. It is also used to report proceeds from

barter exchanges.

What are the new changes in Form 1099-B for the 2025 tax year?

For the 2025 tax year, the IRS has introduced a new update to Form 1099-B that affects how payer and recipient address information is reported.

The address fields for both the Payer and the Recipient have now been divided into separate entry boxes. This means you will need to enter each part of the address — such as street address, city, state, ZIP code, and country — in its own dedicated field, rather than entering the entire address in a single line.

Who must file Form 1099-B?

Broker or barter exchanges are required to file Form 1099-B for each person:

- Brokers: A broker who sells stocks, commodities, regulated futures contracts, foreign currency contracts, forward contracts, debt instruments, options, securities futures contracts, and other financial instruments on behalf of a customer is required to file Form 1099-B. This form reports the proceeds from these sales to the IRS.

- Barter Exchange:An organization that facilitates the exchanges of property or services through barter exchange must file Form 1099-B.

What are the exceptions of Form 1099-B?

Exceptions for Brokers:While brokers are generally required to file Form 1099-B to report sales of securities and certain other transactions, there are specific exceptions where filing is not required. These include:

-

Sales for Exempt Recipients:

You are not required to file Form 1099-B for transactions involving:

- Charitable organizations

- IRAs

- Archer MSAs and HSAs

- Federal, state, or local government entities

- Corporations (unless it involves a covered security acquired by an S corporation after 2011)

-

Sales Initiated by Dealers or Financial Institutions:

Transactions carried out by registered securities dealers and financial institutions are exempt.

-

Sales by Custodians and Trustees:

If a sale is reported on a properly filed Form 1041 (U.S. Income Tax Return for Estates and Trusts), a separate Form 1099-B is not required.

-

Sales of Shares in a Money Market Fund:

Transactions involving regulated investment companies structured as money market funds are excluded.

-

Obligor Payments on Certain Obligations, which include:

- Nontransferable obligations (e.g., savings bonds or CDs)

- Obligations where gross proceeds are reported on other Forms 1099

- Callable demand obligations issued before January 1, 2014, with no premium or discount

-

Sales of Foreign Currency:

Unless part of a forward or regulated futures contract requiring delivery.

-

Sales of Fractional Shares of Stock:

If gross proceeds are less than $20, filing is not required.

-

Retirements of Certain Registered Obligations:

Specifically, book-entry or registered form obligations issued before January 1, 2014, with no interim transfers.

- Sales for Exempt Foreign Persons

-

Sales of Commodity Credit Corporation Certificates:

These transactions are not reportable on Form 1099-B.

-

Spot or Forward Sales of Agricultural Commodities:

Certain agricultural transactions are excluded.

-

Sales of Precious Metals:

Some transactions involving precious metals may be exempt, depending on IRS rules.

-

Options and Certain Contracts:

The granting or purchasing of options, exercises of call options, and entering into contracts requiring personal property delivery are generally exempt.

-

Sales of Short-Term Obligations:

If issued on or after January 1, 2014. However, interest or original issue discount on such obligations may require reporting on Form 1099-INT.

Exceptions for Barter Exchanges: You are not required to file Form 1099-B for:

-

Exchanges through a barter exchange with fewer than 100 transactions in a year.

-

Transactions involving exempt foreign persons.

-

Exchanges where property or services' fair market value (FMV) is less than $1.

Understanding these exceptions helps brokers and barter exchanges determine their reporting obligations and ensures compliance with IRS regulations.

What information is required to file Form 1099-B?

To file Form 1099-B with the IRS, the following information is required:

-

Payer information such as name, address, TIN

-

Recipient information such as name, address, TIN, and account number

-

Transaction information, such as:

- Description of property

- Date of acquisition and sale or exchange

- Gross cash proceeds received from all dispositions (including short sales) of securities, commodities, options, securities futures contracts, or forward contracts

- Accrued market discount

- Wash sale loss disallowed

- Types of Gain or Loss

- Proceeds are from Collectible or Qualified Opportunity Funds (QOF)

- Realized or unrealized profit and loss

- Aggregate profit or loss

-

Federal income tax withheld

-

Bartering information

-

State filing information such as state name, state identification number, and state tax withheld

Click here to learn more about Step-by-step 1099-B instructions.

What is the deadline to file Form 1099-B?

You must be aware of the deadline related to Form 1099-B filing for the 2025 tax year, which includes:

Electronic Filing Deadline: March 31, 2026

The Form 1099-B deadline to file with the IRS electronically for the 2025 tax year is March 31, 2026.

Recipient Copy Deadline: February 17, 2026

In addition to filing with the IRS, a recipient copy must be provided to the recipient. The deadline to distribute copies of Form 1099-B is February 18, 2026. This ensures recipients have the necessary information to file their tax returns on time and accurately.

Paper Filing Deadline: March 2, 2026

If you are filing Form 1099-B with the IRS through paper filing, the deadline to file your 1099-B for the 2025 tax year is March 2, 2026.

TaxBandits supports the secure and accurate filing of Form 1099-B Forms with the IRS and State. We also offer solutions for the distribution of your recipient copies. E-file Form 1099-B Now

Are there penalties for late filing of Form 1099-B?

If you do not file Form 1099-B by the deadline, the IRS will impose a late filing penalty ranging from $60 to $680 per form, depending on the size of your business and the days your return is overdue. To learn more about the details of Form

1099-B penalties, click here.

How to file Form 1099-B for 2025 with TaxBandits?

With TaxBandits, e-filing Form 1099-B is simple and secure. Just follow the steps below to get started:

- Step 1: Create an account with TaxBandits.

- Step 2: Select or add the business you are filing for.

- Step 3: Enter the required Form 1099-B details.

- Step 4: Review and transmit Form 1099-B to the IRS and State.

Get started with TaxBandits today and stay compliant with the IRS! E-file as low as $0.80/Form.

Success Starts with TaxBandits

An IRS Authorized E-file provider you can trust