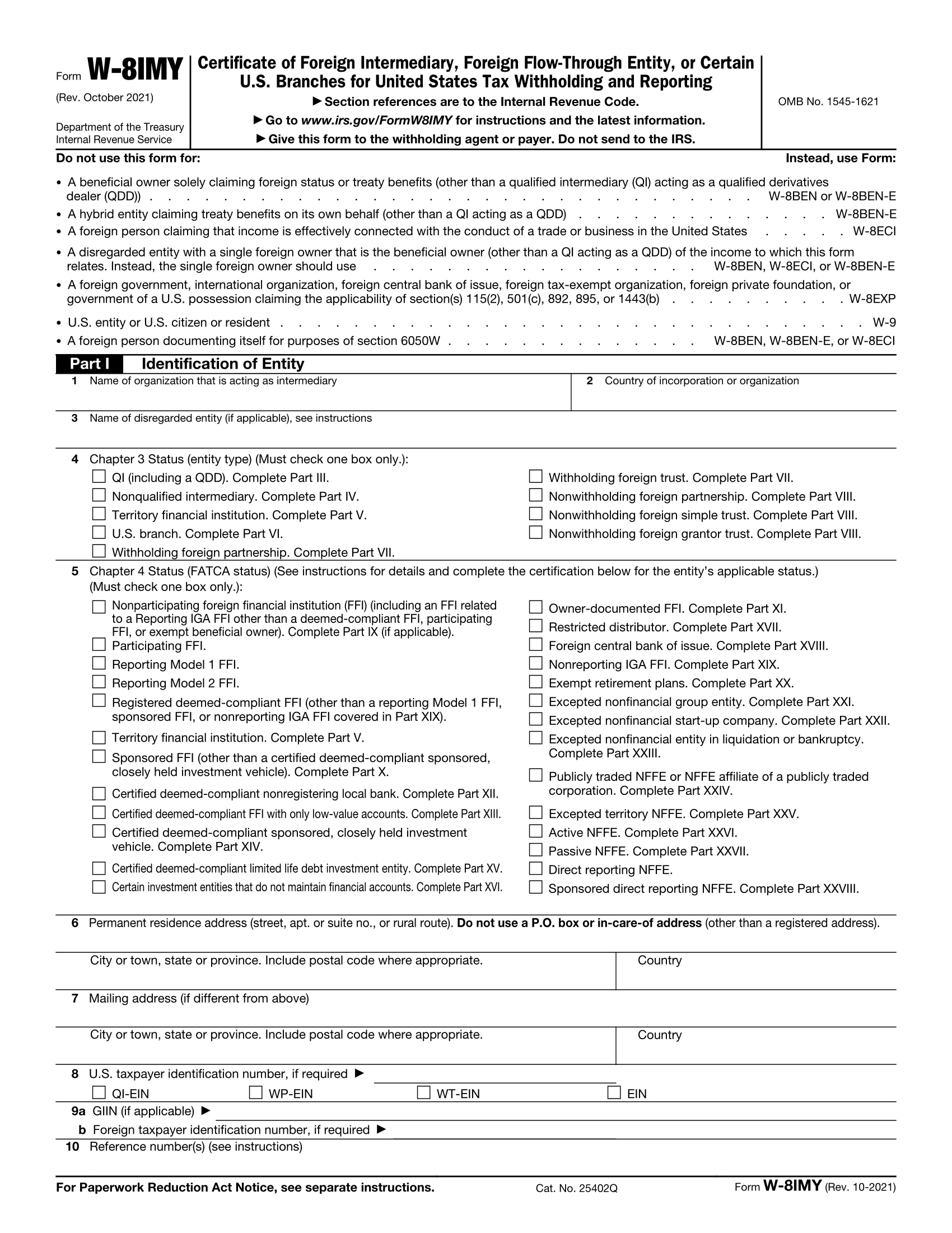

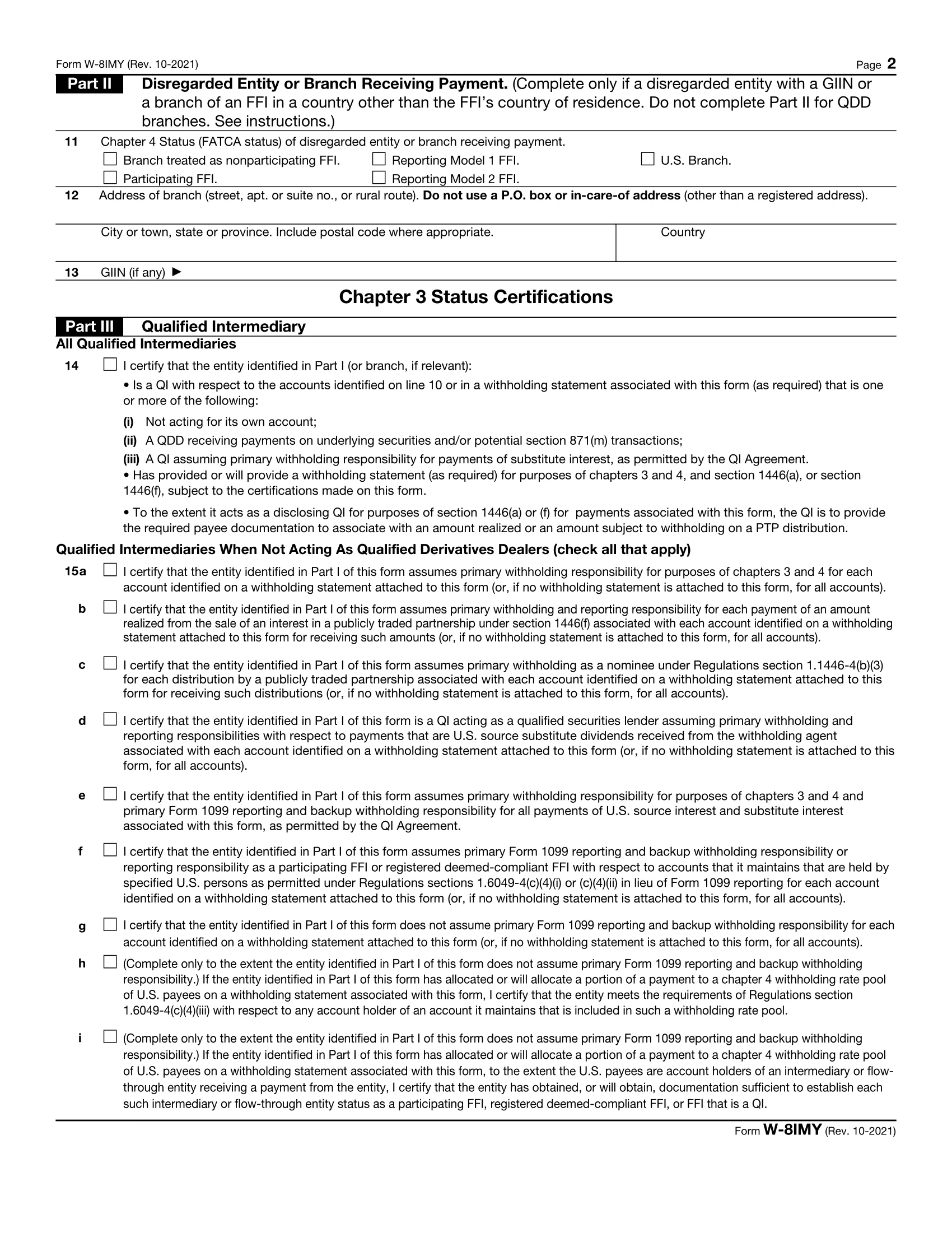

Understanding Form W-8IMY

- Form W-8IMY is an IRS document used by foreign intermediaries, flow-through entities, or certain U.S. branches to certify their status for withholding tax purposes.

- Unlike other W-8 forms, such as W-8BEN, W-8BEN-E, or W-8EXP, the W-8IMY is not used to claim a reduction or exemption from withholding tax.

- Instead, its primary purpose is to document the entity’s status as an intermediary, which may pass through income to its beneficial owners. This allows withholding agents to apply the correct withholding tax rules when payments flow through the intermediary to the ultimate beneficial owners.

What Information is Required to Complete Form W-8IMY?

When your recipients fill out Form W-8 IMY, they must provide the following key information:

-

1. Entity Identification

- Name of the organization (intermediary or flow-through entity)

- Country of incorporation or organization

- Name of a disregarded entity (if applicable)

- Chapter 3 (e.g., Qualified Intermediary, Nonqualified Intermediary, U.S. Branch, etc.) and Chapter 4 (FATCA status, e.g., Participating FFI, Nonparticipating FFI, Active NFFE, Passive NFFE, etc.)

-

2. Address Details

- Permanent address (no P.O. box)

- Mailing address (if different)

-

3. Tax Identification

- U.S. TIN (if required)

- Foreign TIN

- GIIN (if applicable)

- Reference number(s), if needed

-

4. Authorization

- Signature and date by an authorized representative certifying that the information is accurate

What Happens if Form W-8 IMY is Not Provided?

If a foreign intermediary, flow-through entity, or U.S. branch does not provide a completed Form W-8IMY to the withholding agent:

- Backup Withholding Applies: The withholding agent is required by the IRS to apply the full statutory withholding rate on payments subject to U.S. tax (typically 30% for U.S.-source income).

- No FATCA Relief: Without the form, the withholding agent cannot apply any reduced withholding rates or exemptions under FATCA or a tax treaty.

- Payment Delays or Rejection: Payments to the entity may be delayed until the form is received and verified, or the agent may refuse to release the funds.

- Reporting Implications: The entity may be reported to the IRS as a “non-compliant” recipient, which could trigger additional scrutiny or penalties.

Challenges of Collecting Form W-8IMY Manually

Collecting W-8IMY forms manually can create significant administrative and compliance challenges for payers:

Incomplete or Incorrect Forms

Missing fields, invalid treaty claims, or unsigned forms lead to rework and delays.

Higher Compliance Risk

Errors can result in incorrect withholding and penalties during IRS audits.

Time-Consuming Follow-ups

Chasing foreign recipients for corrections increases administrative workload.

Put W-8s on autopilot, eliminate delays, and move beyond the messy chase.

Request W-8IMYs Electronically

Turn days of waiting into minutes with electronic

W-8IMY requests.

Setup Reminders

Automate follow-ups so vendors never slip through the cracks.

Secure Dashboard

Keep track of all your recipients’ W-8IMY in a centralized place.

GIIN Validations

Validating GIINs helps payers reduce errors, streamline withholding, and stay audit-ready.

Stop chasing W-8IMY forms manually. Reduce compliance stress with TaxBandits W-9 Manager.

Frequently Asked Questions

How long is a W-8IMY valid?

A W-8IMY is valid from the date signed until the end of the third calendar year after signing, or sooner if information changes.

For example, a form signed on December 15, 2025, is valid through December 31, 2028.

When to Provide Form W-8IMY to the Withholding Agent?

Form W-8IMY should be provided to the withholding agent before any U.S.-source income is paid, credited, or allocated to the intermediary or flow-through entity.

What is a Qualified Intermediary (QI)?

A Qualified Intermediary (QI) is a foreign financial institution that enters into an agreement with the IRS to act as an intermediary between withholding agents and beneficial owners. A QI can assume responsibility for withholding and reporting U.S.-source income on behalf of its clients.

What is a Qualified Derivatives Dealer (QDD)?

A Qualified Derivatives Dealer (QDD) is a special category of QI that deals in equity derivatives. QDD status is designed to address withholding on dividend equivalent payments under IRC Section 871(m).

How are QI and QDD different?

A QI manages withholding and reporting on general U.S.-source income, while a QDD specifically handles withholding related to dividend equivalents from equity-linked instruments.