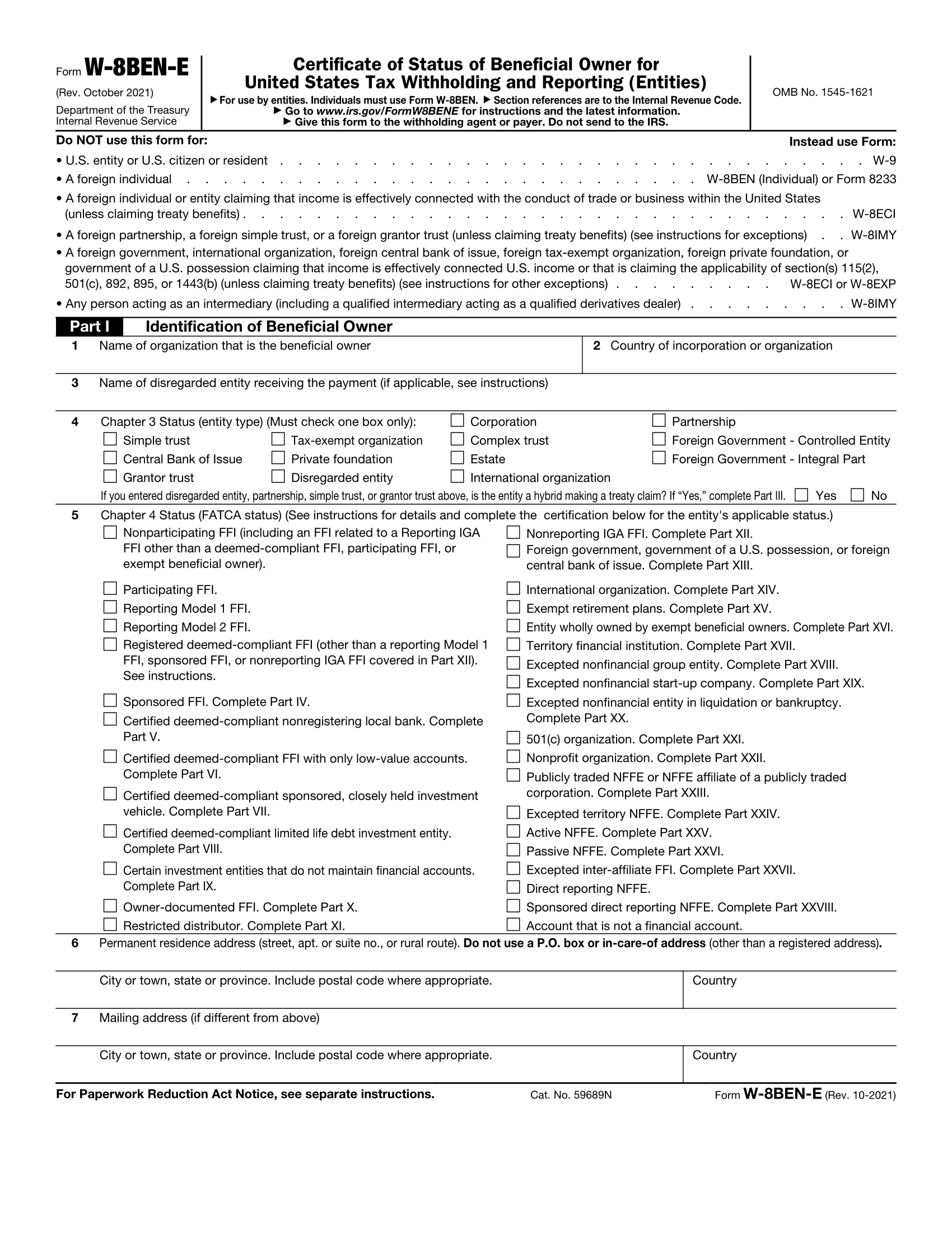

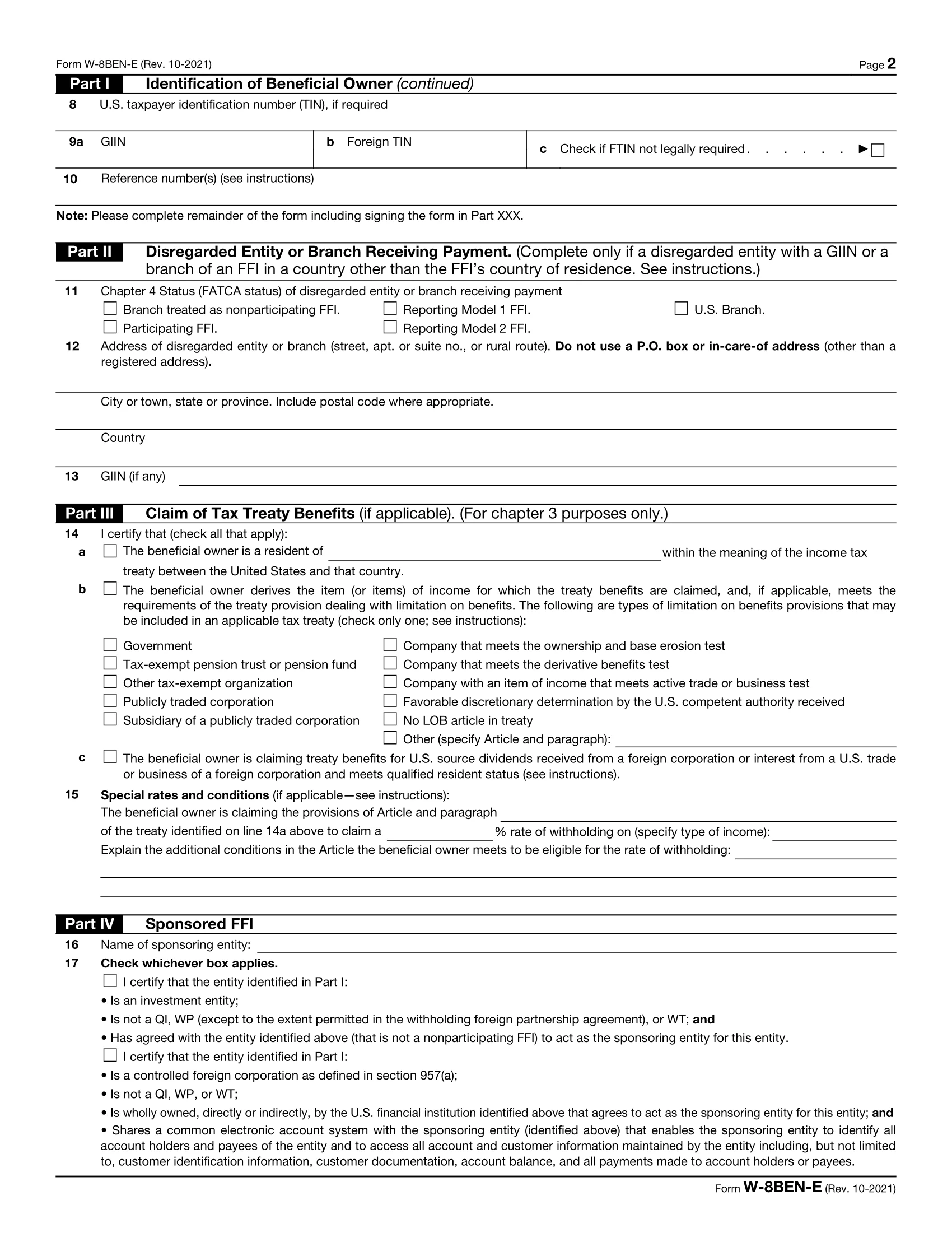

Understanding Form W-8BEN-E

-

Form W-8BEN-E is an IRS document that foreign entities must complete to confirm they are not U.S. taxpayers and to claim reduced withholding under a tax treaty.

-

Payers must request Form W-8BEN-E for certain U.S.-source payments made to foreign entities, including:

- Interest (including certain original issue discount (OID)), dividends, rents, royalties, premiums, annuities, compensation for services performed (or expected to be performed), substitute payments made in securities lending transactions, and other fixed or determinable annual or periodical (FDAP) income.

-

The information reported on Form W-8BENE is used by payers for year-end Form 1042 and Form 1042-S reporting.

-

If you make payments to foreign individuals, request Form W-8BEN instead of Form W-8BEN-E.

What Information is Required to Complete Form W-8BEN-E?

When your recipients fill out Form W-8BEN-E, they must provide the following key information:

-

1. Beneficial Owner Identification

- Entity name and country of organization

- Disregarded entity receiving payment (if applicable)

- Chapter 3 and Chapter 4 (FATCA) status

- Permanent and mailing address

- U.S. TIN (if required), Foreign TIN, GIIN (if applicable)

- Reference numbers (if applicable)

-

2. Disregarded Entity or Branch Details (if applicable)

- FATCA status, address, and GIIN

-

3. Tax Treaty Benefits (if claiming)

- Treaty country of residence

- Applicable treaty article, paragraph, and withholding rate

- Any special conditions met

-

4. Other Entity-Specific Certifications (only if relevant)

- FATCA or Chapter 3 certifications based on entity type

-

5. Certification

- Authorized signature, title, date

- Statement confirming accuracy and authority to sign

What Happens if Form W-8BEN-E is Not Provided?

- Backup Withholding: The withholding agent may apply the default 30% rate to U.S.-sourced income.

- Loss of Tax Treaty Benefits: The entity may be ineligible for reduced withholding rates.

- Delayed Payments: Payments may be withheld or delayed until the form is submitted.

- FATCA Non-Compliance: Financial institutions may freeze accounts for non-compliance with FATCA requirements.

Challenges in Form W-8BEN-E Collection

W-8BEN-E collection by paper or by email increases administrative burden, slows payments, and raises compliance risks for payers.

Incomplete or Incorrect Forms

Missing fields, invalid treaty claims, or unsigned forms lead to rework and delays.

Higher Compliance Risk

Errors can result in incorrect withholding and penalties during IRS audits.

Time-Consuming Follow-ups

Chasing foreign recipients for corrections increases administrative workload.

Put W-8s on autopilot, eliminate delays, and move beyond the messy chase.

Request W-8BEN-Es Electronically

Turn days of waiting into minutes with electronic

W-8BEN-E requests

Setup Reminders

Automate follow-ups so vendors never slip through the cracks

Secure Dashboard

Keep track of all your recipients’ W-8 BEN-E in a centralized place

GIIN Validations

Validating GIINs helps payers reduce errors, streamline withholding, and stay audit-ready.

Stop chasing W-8BEN-E forms manually. Reduce compliance stress with TaxBandits W-9 Manager.

Frequently Asked Questions

How long is a W-8BEN-E valid?

A W-8BEN-E form remains valid for three years from the date it is signed. Payers should request a new form once it expires or if any information on the form changes.

For example, a form signed on December 15, 2025, is valid through December 31, 2028.

What is the difference between W-8 BEN-E and W-8 BEN?

- Form W-8BEN-E: Used by foreign entities—such as corporations, partnerships, or trusts—to certify their non-U.S. status and claim applicable tax treaty benefits when receiving U.S.-source income.

- Form W-8BEN: Used by foreign individuals to certify non-U.S. status and claim tax treaty benefits that may reduce U.S. withholding on certain payments.

Who is the beneficial owner of a W-8 BEN-E?

The beneficial owner for Form W-8BEN-E is the foreign entity that actually owns the income and is entitled to the income for U.S. tax purposes.

Examples of beneficial owners include:

- A foreign corporation earning U.S.-source interest or dividends

- A foreign partnership or trust that owns the income

- A foreign organization receiving U.S.-source payments directly

What is the purpose of Chapter 3 status?

Chapter 3 status identifies how a foreign individual or entity is classified under U.S. withholding tax rules.

It helps withholding agents determine whether U.S. tax applies, the correct withholding rate, and how payments should be reported on Forms 1042 and 1042-S.

Most foreign entities fall under Corporation or Partnership status, while other options include foreign government entities, estates, trusts, tax-exempt organizations, private foundations, international organizations, central banks of issue, and disregarded entities.

What is the purpose of Chapter 4 status?

Chapter 4 status identifies a foreign entity’s classification under FATCA (IRC Chapter 4)

It is used to determine whether FATCA withholding applies, whether the payee is compliant with FATCA reporting requirements, and whether a 30% FATCA withholding tax must be imposed on certain U.S.-source payments. Chapter 4 status helps withholding agents apply the correct withholding, document compliance, and accurately report payments on Forms 1042 and 1042-S.

What is FATCA?

FATCA (Foreign Account Tax Compliance Act) is a U.S. tax law designed to prevent tax evasion by U.S. persons holding assets outside the United States. Under FATCA, foreign entities are classified as either Foreign Financial Institutions (FFIs) or Non-Financial Foreign Entities (NFFEs). FFIs must identify and report U.S. account holders, while NFFEs must disclose whether they have substantial U.S. owners. Noncompliance may result in a 30% withholding tax on certain U.S.-source payments.