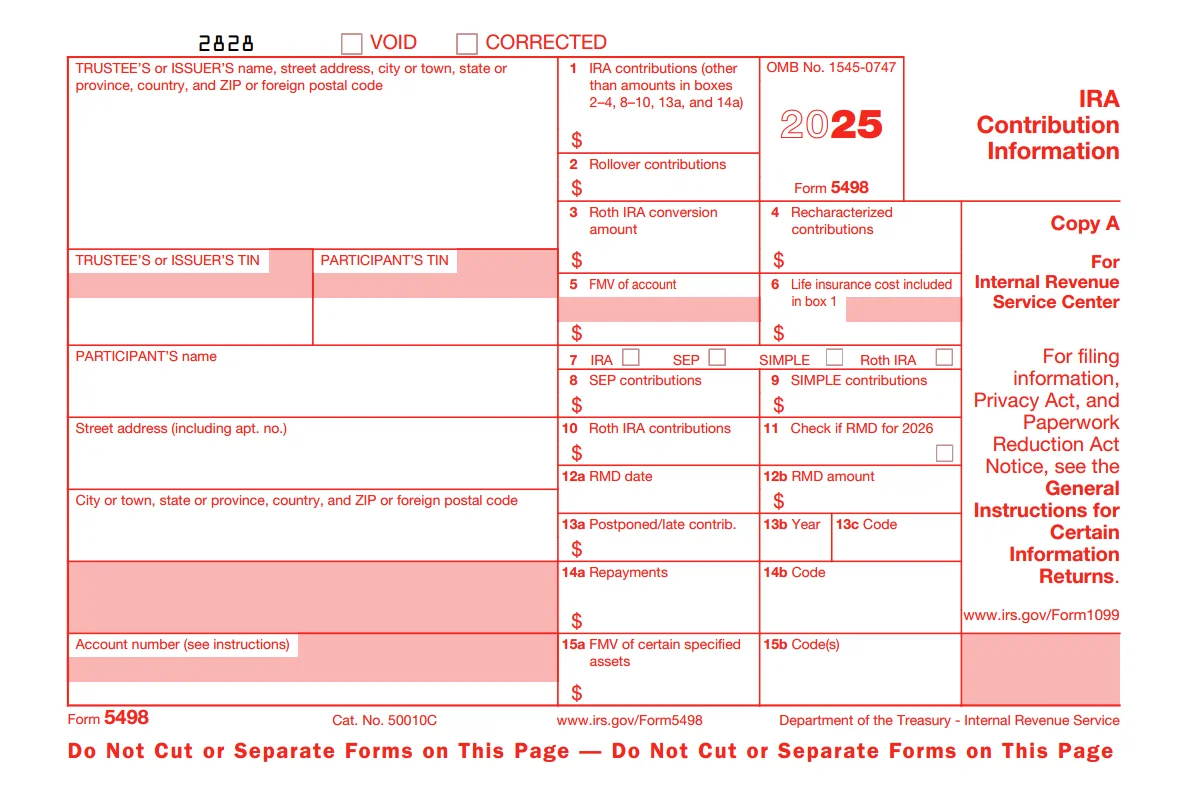

Line by Line IRS Form 5498 Instructions for 2025

To file Form 5498 accurately, banks and IRA custodians must understand how to complete and file the form with the IRS properly. Accurate reporting is essential to avoid costly errors and potential penalties.

Read this guide to learn how to complete Form 5498 correctly.

Table of contents:

What is Form 5498?

Form 5498 is used by banks and other financial institutions to report key information about Individual Retirement Accounts (IRAs) to the IRS. This includes:

- Annual contributions to traditional, Roth, SEP, and SIMPLE IRAs

- Rollovers and recharacterizations

- Fair market value (FMV) of the IRA as of December 31

- Required Minimum Distribution (RMD) details for account holders age 73 or older

The IRS uses this information to ensure accurate reporting and compliance with contribution limits and distribution rules.

How to fill out Form 5498 for 2025?

Form 5498 comprises several sections, each designated to capture specific information. Below is a detailed breakdown of each section of Form 5498.

Trustee's or Issuer's Information

This section identifies the financial institution (trustee or issuer) responsible for administering the IRA. It must include:

- Name and address of the trustee or issuer

- Trustee's Taxpayer Identification Number (TIN)

Participant Information

This section identifies the IRA owner (referred to as the participant) for whom the form is being filed. Include

the following:

- Full name of the participant

- Street address, including apartment or suite number if applicable

- City, state, ZIP code, or foreign address if outside the U.S.

-

9-digit Taxpayer Identification Number (TIN)—usually the participant’s Social Security

Number (SSN)

-

Box 1 - IRA contributions (other than amounts in boxes 2–4, 8–10, 13a, and 14a)

Enter contributions to a traditional IRA made in 2025 and through April 15, 2026, designated for 2025.

Do not report the same contribution again in a later year if it’s carried forward. It should only be included for the year it was originally contributed.

You must report the gross contribution amount, including:

- Any portion allocable to life insurance (this will also be reported in Box 6),

- Excess contributions (even if withdrawn later), and Certain employer contributions that are not part of a formal SEP arrangement but are treated as regular IRA contributions.

Contribution Limits

Report up to $7,000 per participant ($8,000 if age 50 or older), or 100% of compensation—whichever is less.

Do not include the following in Box 1

- Rollovers (Box 2)

- Roth conversions (Box 3)

- Recharacterizations (Box 4)

- SEP contributions (Box 8)

- SIMPLE IRA contributions (Box 9)

- Roth IRA contributions (Box 10)

-

Box 2 - Rollover contributions

Report any rollover contributions (or contributions treated as rollovers) to any IRA you received in 2025. These may include:

- A 60-day rollover between Roth IRAs or other types of IRAs.

-

A direct or indirect rollover (within 60 days) from a qualified plan, 403(b) plan, or

457(b) plan. - A qualified rollover from an eligible retirement plan (other than an IRA) to a Roth IRA.

- A military death gratuity or Servicemembers’ Group Life Insurance (SGLI) payment.

For property rollovers, enter the property's fair market value (FMV) on the day you receive it. This value may differ from the value on the day the property was given to the participant.

Do not use box 2 for late rollover contributions, or any of the following repayments made

after 60 days.- Qualified reservist distributions

- Qualified disaster distributions

- Qualified birth or adoption distributions

- Emergency personal expense distributions

- Terminally ill individual distributions

- Eligible distributions for domestic abuse victims

-

Box 3 - Roth IRA conversion amount

Report the total amount converted from any of the following account types to a Roth IRA during the 2025 calendar year:

- Traditional IRA

- SEP IRA

- SIMPLE IRA

This includes both direct conversions and 60-day rollovers that result in a Roth IRA.

-

Box 4 - Recharacterized contributions

Use this box to report any recharacterized contributions, including associated earnings, that were transferred from one type of IRA to another during 2025.

This typically involves a contribution made to a Roth IRA that is later recharacterized to a Traditional IRA, or

vice versa. -

Box 5 - FMV of Account

Enter the fair market value of the participant’s entire IRA account as of December 31, 2025.

-

Box 6 - Life Insurance Cost Included in Box 1

If the participant’s IRA is an endowment contract, enter the portion of the Box 1 contribution allocated to the cost of life insurance.

An endowment contract is a type of life insurance policy that combines life coverage with a savings component. It pays out a lump sum either upon the insured person's death or after a specified period, whichever comes first.

-

Box 7 - Checkbox the Appropriate Type of IRA

Check the box that correctly identifies the type of IRA for which you are filing this Form 5498:

- IRA – Check the IRA box if you’re filing Form 5498 to report traditional IRA information

- SEP – Check if reporting a SEP IRA account.

- SIMPLE – Check if reporting a SIMPLE IRA; don’t use for SIMPLE 401(k) plans.

- Roth IRA – Check if reporting a Roth IRA account.

- Roth SEP IRA – Check both “SEP” and “Roth IRA” for a Roth SEP IRA.

- Roth SIMPLE IRA – Check both “SIMPLE” and “Roth IRA” for a Roth SIMPLE IRA.

-

Box 8 - SEP contributions

Report employer contributions to a SEP IRA, including,

- Salary deferrals under SARSEP.

- Contributions made in 2025 for 2024, but exclude those made in 2026 for 2025.

You should also:

- Include SEP contributions made by self-employed individuals to their own SEP IRA

- Include contributions to a Roth SEP IRA, if applicable

Do not include employer contributions that are not made under a SEP arrangement (e.g., contributions exceeding the SEP’s allocation formula). These should be reported in Box 1 as regular IRA contributions.

-

Box 9 - SIMPLE contributions

Report all employer contributions and employee salary deferrals made to a SIMPLE IRA during 2025. This includes:

- Contributions made in 2025 for the 2024 tax year

- Contributions to Roth SIMPLE IRAs, if applicable

Do not report any contributions made in 2026 for 2025. Only amounts actually deposited in 2024 should be included. Also, do not include contributions made to a SIMPLE 401(k) plan.

-

Box 10 - Roth IRA contributions

Report the following in Box 10 of Form 5498:

-

Roth IRA Contributions for 2025

Include any Roth IRA contributions (not Roth SEP or Roth SIMPLE) made:

- During the 2025 calendar year, and

- By April 15, 2026, if designated for the 2025 tax year.

-

Qualified 529 Plan to Roth IRA Rollovers (New Rule)

You must also include qualified rollover contributions from a Section 529 Qualified Tuition Program (QTP) to a Roth IRA, if:

The rollover is designated for tax year 2025:

- It is completed using a direct trustee-to-trustee transfer

- The Roth IRA belongs to the same beneficiary as the 529 plan

- The 529 account has been open for more than 15 years

The rollover follows these IRS limits:

- Counts toward the annual Roth IRA contribution limit

- Lifetime limit: $35,000 per beneficiary

Do not include in box 10 contributions to a Roth SEP IRA or Roth SIMPLE IRA.

-

-

Box 11 - Check if RMD for 2026

Check this box if the participant is required to take an RMD for 2026. You must check the box if:

- The participant turns age 73 in 2026, even though their first RMD isn’t due until April 1 of the following year.

- The participant is already age 73 or older and is required to take an RMD in 2026.

This checkbox is used by both the IRS and the participant to track RMD obligations. Ensure it's checked accurately, as it can affect tax reporting and

distribution planning. -

Box 12a & b - RMD Date and Amount

To accurately file Form 5498, enter the RMD date in Box 12a and the RMD amount in Box 12b when reporting additional retirement account details.

-

Box 13a,b, & c - Postponed/Late Contribution, Year, and Code

Postponed contributions made in 2025 for a prior year must be reported in Box 13a.

- If contributions were made for more than one prior year, use a separate Form 5498 for each year. Also, if a participant has a postponed contribution and a late rollover, use separate Forms 5498 for each.

-

Late rollover contributions made in 2025 should also be reported in Box 13a.

- Rollovers certified by the participant

- Qualified plan loan offsets

- Rollovers related to federally declared disasters

- In box 13b, input the year the postponed contribution (reported in Box 13a) pertains to. Leave this box blank for late rollover contributions and qualified plan loan offsets.

-

In box 13c, provide the reason the participant made the postponed contribution using the

appropriate code.- If the participant served in a combat zone or similar area, enter the executive order or public law that applies.

-

If the participant was affected by a federally declared disaster, enter "FD".

If it's a repayment of a qualified disaster distribution, use Boxes 14a and 14b, not Box 13.

- If it's a rollover of a qualified plan loan offset, enter "PO".

- If the rollover is late but the participant has self-certified the reason under IRS-approved circumstances, enter "SC".

-

Box 14a & b - Repayments and their Codes

Enter the amount associated with any repayment of a qualified reservist distribution, a qualified disaster distribution, or a qualified birth or adoption distribution in box 14a and their respective repayment codes in line 14b. Here is the list of repayment codes:

- "QR" for qualified reservist distribution

- "DD" for qualified disaster distribution

- "BA" for qualified birth or adoption distribution

- "EP" for emergency personal expense distribution

- "TI" for the terminally ill individual distribution, and

- "DA" for eligible distribution to a domestic abuse victim.

-

Box 15a & b - FMV of Certain Specified Assets and their Codes

Enter the fair market value (FMV) of the investments in the Individual Retirement Account

(IRA) in 15a.The following codes can be entered in box 15b, and you can enter a maximum of 2 codes. If more than two codes are applicable, enter Code H. The table below explains the codes of the asset type.

| Code | Type of Assets |

|---|---|

|

A |

Stock or other ownership interest in a corporation that is not readily tradable on an established securities market. |

|

B |

Short- or long-term debt obligation that is not traded on an established |

|

C |

Ownership interest in a limited liability company or similar entity (unless the interest is traded on an established securities market). |

|

D |

Real estate |

|

E |

Ownership interest in a partnership, trust, or similar entity (unless the interest is traded on an established securities market). |

|

F |

An option contract or similar product that is not offered for trade on an established option exchange. |

|

G |

Another asset that does not have a readily available FMV. |

|

H |

More than two types of assets (listed in A through G) are held in this IRA. |

When is Form 5498 Due for the 2025 Tax Year?

The IRS requires Form 5498 to be filed electronically by June 01, 2026, for the 2025 tax year. The deadline for distributing participant copies of FMV and RMD information is February 02, 2026, while the deadline for other IRA details is June 01, 2026.

Learn more about the Form 5498 Deadline for the 2025 tax year.

How to File Form 5498 Electronically?

TaxBandits, an IRS-authorized e-file service provider, offers a comprehensive solution to prepare and e-file 5498 forms with the IRS. By following the simple steps outlined below, you can easily e-file Form 5498 with the IRS:

- Step 1: Create an account in TaxBandits.

- Step 2: Choose "Form 5498" and the Tax Year.

- Step 3: Enter Form 5498 Information

- Step 4: Review and Transmit to the IRS

- Step 5: Distribute recipient copies via Postal Mailing or Online Access.

Browse by Topics

Form 5498 Resources

FAQs

Blog

Help Videos